- EAER>

- Journal Archive>

- Contents>

- articleView

Contents

Citation

| No | Title |

|---|---|

| 1 | Buying on Margin and Short Selling in an Artificial Double Auction Market / 2017 / Computational Economics |

Article View

East Asian Economic Review Vol. 17, No. 3, 2013. pp. 311-332.

DOI https://dx.doi.org/10.11644/KIEP.JEAI.2013.17.3.268

Number of citation : 1View

1353

Download

97

The Effect of Initial Margin on Long-run and Short-run Volatilities in Japan

|

Sangbae Kim |

School of Business Administration, Kyungpook National University |

|---|---|

|

Taehun Jung |

School of Economics & Trade, Kyungpook National University |

Abstract

This paper examines the effect of initial margin requirements on long-run and short-run volatilities in the Japanese stock market using the Component GARCH model. Our empirical results show that when we do not divide the margin requirement into positive and negative changes, increasing margin requirement is effective for reducing long-run volatility, while not effective in short-run volatility. However, separating the positive and negative changes in margin requirements reveals the fact that the negative changes in margin requirements decrease long-run volatilities, while the higher margin requirements increase short-run volatilities in the Japanese stock market. This suggests that if the Japanese financial authorities intend to increase margin level to reduce volatility, unexpectedly, short-run volatility would be even higher.

JEL Classification: G10, G14, G18

Keywords

Margin Requirement, Long-run Volatility, Short-run Volatility, Component GARCH Model

I. Introduction

Do margin requirements play an important role in reducing stock market volatility? Many government regulators of the stock markets thought that volatility in the stock market might be controlled by some restrictions about buying on margin and short-selling. In other words, margin and short-selling can be easily used to stimulate the stock prices when the stock market is in recession, while these policies can be adopted to reduce the bubble of the stock prices when it is in boom.

Initial margin requirements were firstly imposed by the US Congress with the Securities and Exchange Act of 1934 to reduce the credit-financed speculation in the stock market, which may lead to excessive price volatility through a “pyramiding-depyramiding” process1 (Garbade, 1982). Therefore, initial margin requirements are designed and adopted to prevent excess volatility in the stock markets. However, the previous literatures show mixed results. For example, some studies (Kupiec, 1989; Hardouvelis, 1990, Hardouvelis and Theodossiu, 2002 among others) find the negative relationship between margin requirements and stock volatility, while the other studies (Schwert, 1989; Hsieh and Miller, 1990; Kim and Oppenheimer, 2002 among others) find no reliable evidence.

Basically, the pyramiding-depyramiding process takes for granted the presence of both rational and irrational investors (speculators) and expects the negative relationship between margin requirement and stock volatility. DeLong, Shleifer, Summers and Waldman (1990) theoretically show that the amount of nonfundamental volatility in the stock market increases, when noise (destabilizing) traders lever their positions. Therefore, higher margin requirements primarily restrict the participation of irrational investors in the stock market and settle excess volatilities and mispricing. Kumar et al. (1991) refer to this as the speculative effect.

Along with the speculative effect, Kumar et al. (1991) also mentioned the liquidity effect. If speculation is inherently stabilizing, then higher margin requirements restrict the activities of rational investors. That is, higher margins could potentially generate the lack of liquidity in the stock market. This lack of liquidity would cause higher volatility. This implies that when the liquidity effect prevails, there could be a positive relationship between margin requirement and stock volatility.

Depending on which effect between the speculative effect and the liquidity effect is dominant, the positive or negative relationship can be observed. In other words, if irrational (rational) investors play a role in the stock market, we can observe the negative (positive) relationship. It is natural that irrational investors play an important role in the short-run than in the long-run because sufficient time is given to collect information over the long-run. Therefore, we expect that dividing volatility into long-run and short-run components gives more insights for the effect of initial margin requirements.

The purpose of this paper is to examine the effect of initial margin requirements on long-run and short-run volatilities in the Japanese stock market. To consider the effect of initial margin requirement on long-run volatilities, the previous literatures (e.g., Hardouvelis, 1990; Hsieh and Miller, 1990; Hardouvelis and Theodossiu, 2002) construct longer horizon volatilities such as monthly and annual volatilities to examine the relationship between margin requirements and stock volatility. When using longer horizon volatilities, the relationship may be unreliable due to a handful of independent observations from generating long horizon volatilities. In the study of Hardouvelis (1990), he constructs the rolling 12-month estimator of volatility by implicitly assuming that volatility is nonstationary.2 Considering this problem, we adopt the component GARCH (CGARCH) model,3 proposed by Engle and Lee (1999). This model assumes that volatility consists of two components: one is the long-run volatility component whose shocks are highly persistent, and the other is the short-run volatility component whose shocks are less persistent.

This paper uses Japanese data for the investigation. As mentioned in Kim and Oppenheimer (2002), the Japanese experience is very useful for examining the relationship between margin requirements and volatilities due to frequent revision of margin requirements by the Tokyo Stock Exchange (TSE) and high proportion of margin transaction in all transactions in the country. Since 1970, during our sample period, there were 63 margin changes. Among a total of 63 margin policy changes, margin policy change is overlapped 10 times in monthly data.4 Therefore, there are possibility to lose some important information for investigating the relationship between margin requirements and volatility.

Overall, our results show that increasing margin requirement is effective for reducing long-run volatility, while not effective in short-run volatility. However, separating the positive and negative changes in margin requirements reveals the fact that the negative changes in margin requirements decrease long-run volatilities, while the higher margin requirements increase short-run volatilities in the Japanese stock market. This suggests that if the Japanese financial authorities intend to increase margin level to reduce volatility, unexpectedly, short-run volatility would be even higher.

The remainder of this paper is organized as follows. Section 2 describes the CGARCH model as our main empirical model. Data and empirical results are discussed in Section 3. In section 4, we discuss the results of dividing the positive and negative changes in margin requirements, while Section 5 presents concluding remarks with a summary of our results.

1)The pyramiding-depyramiding process is related to the excessive price movements. For example, the pyramiding effect can be created when the stock market is boom. Optimistic investors could borrow large amounts of money and bring stock prices up to levels unjustified by the intrinsic values of firms if there is no margin requirement restriction. In addition, if speculators were to use their increased wealth to buy more stocks on margin, this increased price could feed on itself. Suppose that brokers were to ask for additional collateral when there are some adverse news in the stock market and that some speculators lacked the requested margin funds. In this case brokers would sell their stocks driving the stock prices down further. This further declined stock price would generate more margin calls for collateral, more liquidations, and additional price declines. This is called the depyramiding effect

2)Furthermore, in the study of

3)In relation to using the GARCH model,

4)More detail discussion for our data will be provided in section 3.

II. Data and descriptive statistics

Our study uses the NIKKEI225 index and TOPIX index as proxy for the Japanese stock market.5 Our data from are composed of daily closing prices, obtained from Datastream for the period of January 5, 1970 to December 27, 1990.6 Daily returns are computed by log(

The data on initial margin requirements,

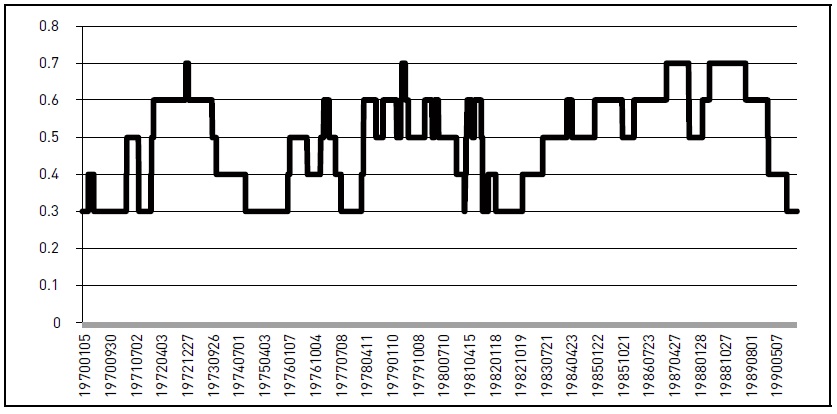

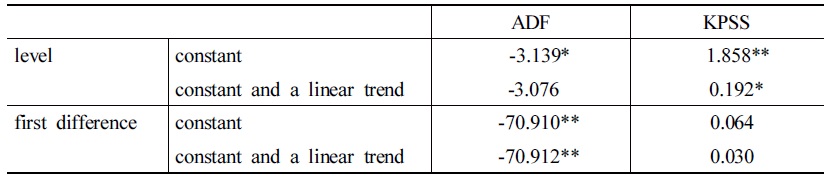

As can be seen in Figure 1, the margin requirement is a discrete variable, which is constrained to take values from 0.3 to 0.7. As mentioned in Hardouvelis and Theodossiu (2002), due to its finite variance, the level of margin requirements cannot be conceptually treated as a random walk process, i.e., a process with a unit root. However, because our sample series are a finite sample, the infrequent changes in margin requirement could produce empirically an autocorrelation function, which is very similar to one originating from a series with a unit root. Therefore, it is important to examine the stochastic process of margin requirement. We adopt the Augmented Dickey-Fuller (hereafter ADF) test and Kwiatkowski, Philips, Schmidt and Shin (1992, hereafter KPSS) test.

Table 2 reports the results of unit root tests at levels and first differences with and without a trend using the ADF and KPSS tests. The reason for using the KPSS test is that the ADF test has been shown to fail to distinguish between a unit root and weakly stationary process due to its null hypothesis that the series has a unit root (Lee and Mathur, 1999). The result of the ADF test suggests that the level of margin requirement is stationary at 5% significance level, consistent with Hardouvelis and Theodossiu (2002) and Sohn and Kim (2009). However, those of the KPSS, whose null hypothesis of the KPSS test is that margin requirement is stationary, indicate that margin requirements are non-stationary at level, while stationary at first difference. Overall, the results of the unit root tests depend on which methods are adopted for the unit root test. Based on this conflicting result, we use the level and a dummy variable for the margin changes for our analysis.

Note that the purpose of an increase (decrease) in margin requirements is to reduce excess volatility in the stock market. Therefore, the effect of the negative changes in margin requirement could be offset by that of the positive changes or vice versa. For this possible reason, this paper uses the dummy variable for the margin changes.

5)The data series are obtained while the second author visited University of Michigan. In addition, we use Eviews 6.0 for our empirical examination.

6)Because the margin requirement has not changed since September 7, 1990, we expect that the latest data sample cannot possibly add much information about the relation between margin requirements and stock volatility. Therefore, this sample period has been chosen in our study.

III. Empirical model

In this section, we present the CGARCH model developed by Engle and Lee (1999) to decompose market volatility into a short-run component,

where

We define the conditional volatility specification, which permits both the long-run component of conditional variance,

In addition, by rearranging equation (2), Engle and Lee (1999) specify the dynamics of the short-run volatility components as follows:

Using equations (3) and (4), the persistence of short-run and long-run volatility can be captured by

To examine the effect of initial margin on short- and long-run volatilities, our empirical model is specified by adding the initial margin dummy into equation (1), (2) and (3) as follows:

where

In the mean equation (6), we include the dummy variable for the margin changes,

In addition, we also incorporate the margin dummy in the conditional variance equations (7) and (8). If the pyramiding-depyramiding process is likely to last a few months (Hardouvelis, 1990), the margin changes influence the volatility trend (i.e., long-run volatility). However, if the effect of the margin changes is transitory, the changes in margin requirements do not affect long-run volatility of the stock market, but only influence short-run volatility.

The studies of Hardouvelis and Theodossiu (2002) and Sohn and Kim (2009) use the EGARCH model, which specifies asymmetric effect of news on conditional volatility. Following their studies, we also incorporate the asymmetric component in our CGARCH model by introducing asymmetric effects in short-run volatility equation (7) as:

In this specification,

IV. Empirical results

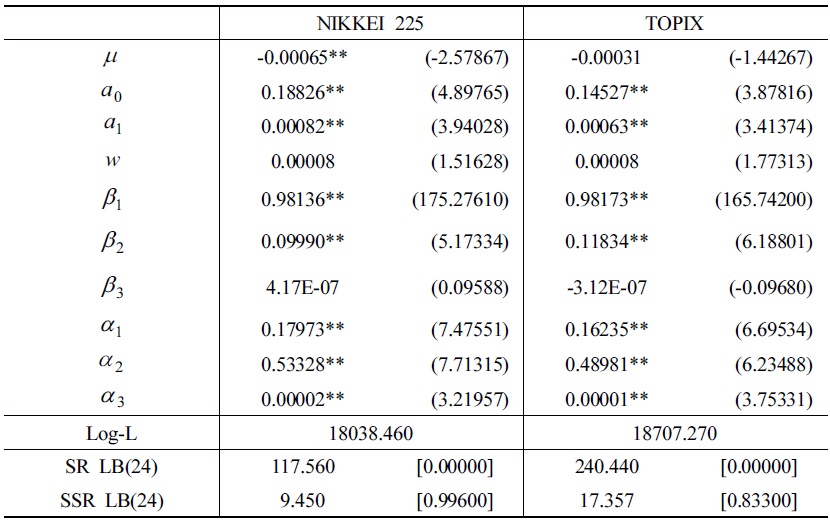

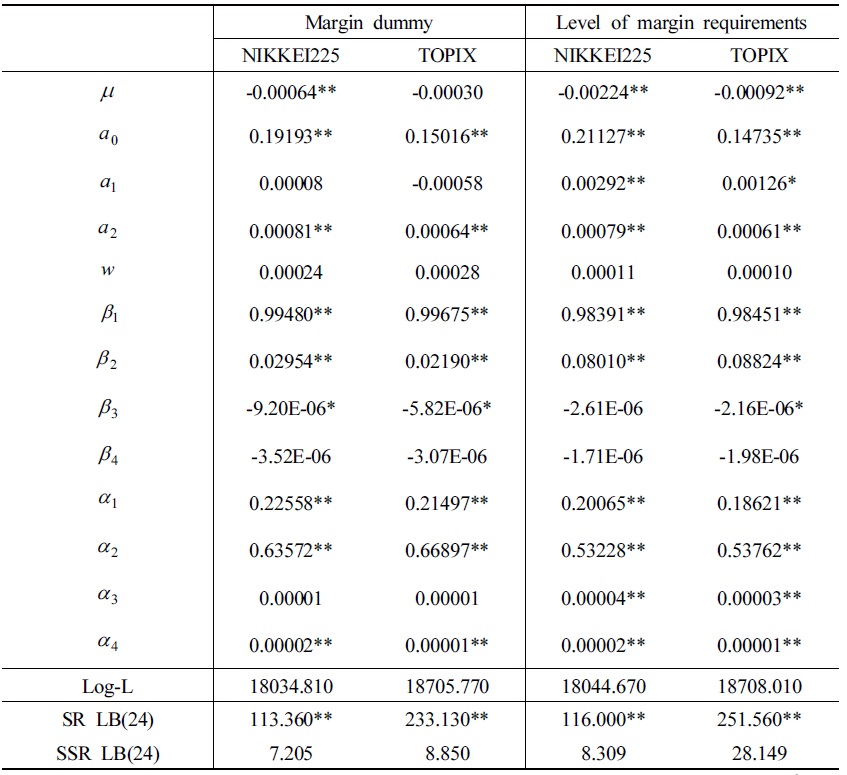

In this section, we discuss the empirical results of the CGARCH model. The estimation results of the CGARCH model, presented in equations (1) - (3), are reported in Table 3. In this table, we report the CGARCH model estimates and t-statistics. In addition, SR and SSR denote standardized residuals and squared standardized residuals, respectively. LB(24) indicates the Ljung-Box test of significance of autocorrelation of up to 24 lags. Estimation of the CGARCH model reported here is by maximum likelihood under the assumption that the distribution of shock is GED.

The estimated mean equation in Table 3 shows that the coefficient for the conditional variance (

In addition, Table 3 shows that the persistence of long-run volatility is very high (0.981 for NIKKEI225 and 0.982 for TOPIX), while the persistence of short-run volatility is relatively low (0.713 for NIKKEI225 and 0.652 for TOPIX). The parameter,

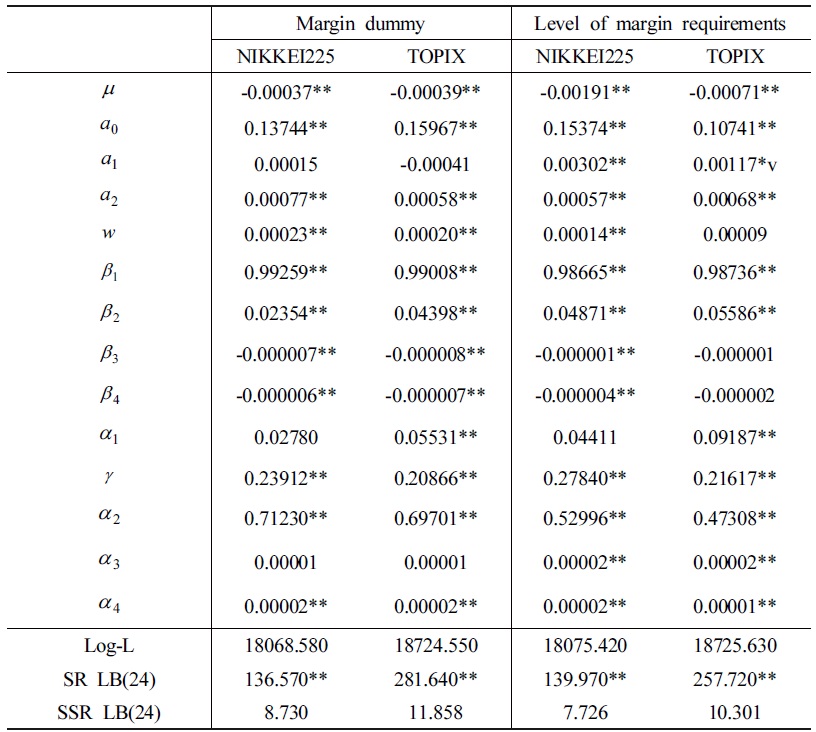

The main purpose of this paper is to examine the impact of margin requirements on long-run and short-run volatilities. To do so, we first estimate the CGARCH model, presented in equations (6) - (8). In this estimation, we use a dummy variable for the changes in margin requirements. In addition, we also estimate the CGARCH model with the level of margin requirements as a robustness check because the results of the two unit root tests (ADF and KPSS) are different.

Table 4 illustrates the estimated results of the CGARCH model with margin requirements.7 Consistent with the findings of the previous literature and Table 3, the coefficients for the conditional variance (

Moving to the conditional variance equations, the coefficients,

Overall, our result shows that the changes in margin requirement are effective for reducing long-run volatility, while not effective in short-run volatility. More specifically, the coefficients

The coefficients,

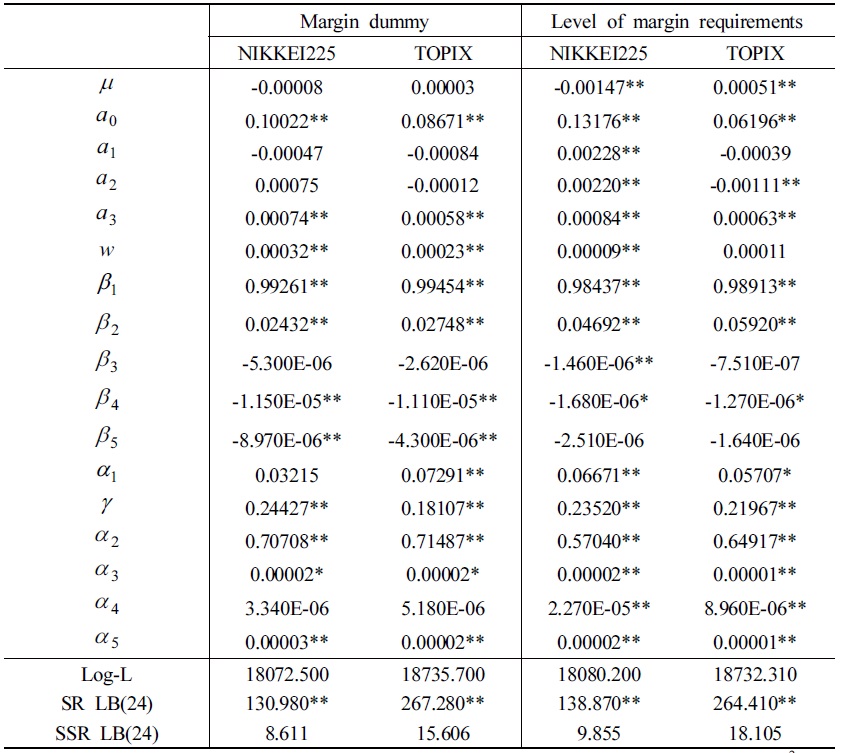

In order to consider the asymmetric effect of conditional volatility, similar to Hardouvelis and Theodossiu (2002) and Sohn and Kim (2009), we estimate the asymmetric CGARCH model, shown in equations (6), (8) and (9). The estimated results are reported in Table 5. When we incorporate the asymmetric factor of conditional short-run volatility, we find that the coefficient,

Besides, the overall result is same as those of Table 4, by showing that the coefficients,

7)We do not report t-statistics for the estimated coefficients for the sake of brevity.

8)We thank an anonymous referee for pointing this out.

V. Further analysis

Until now, we examined the effect of the changes in margin requirements on the long-run and short-run volatilities. Hardouvelis and Theodossiu (2002) mentioned that “the Federal Reserve raised margins when it saw signs of “excessive” speculative activity, such as rising stock prices and rising margin credit that appeared unusual. The Fed decreased margins when it thought that the factors which had led it earlier to increase margins ceased to exist.” Therefore, it would be expected that increasing and decreasing margin requirements influence long-run (short-run) volatility differently. For example, Kumar et al. (1991) argue that the changes in margin requirement could be positively related to the changes in short-run volatility due the liquidity effect. More specifically, if that higher margin increases short-run volatility by lack of liquidity in the stock market, lowering margin requirement generate more liquidity in the market and thus lowering short-run volatility. To this end, we extend our asymmetric CGARCH model by incorporate the positive and the negative margin dummies as follows:

where  is a positive (negative) margin dummy, which takes the value of 1 when the margin requirement is increased (decreased) at day t-1, otherwise zero9.

is a positive (negative) margin dummy, which takes the value of 1 when the margin requirement is increased (decreased) at day t-1, otherwise zero9.

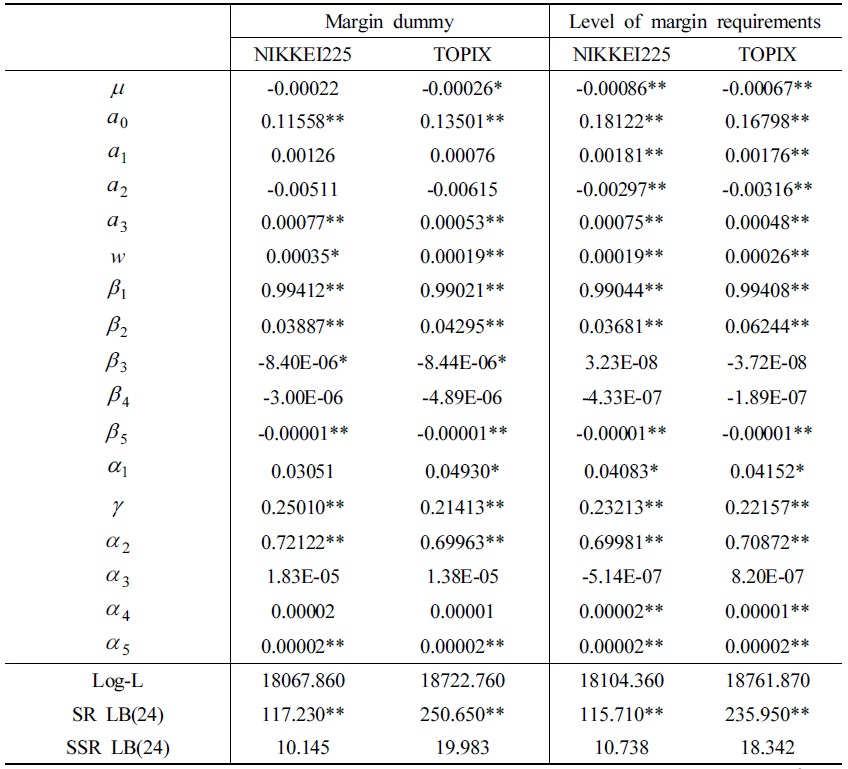

The estimated results are reported in Table 6. The effects of the positive and negative changes in margin requirements on stock returns are captured by the coefficients,

The purpose of including the asymmetric term in the conditional volatility equation is to consider the possible effect of the asymmetric effect in volatility. The results show that the coefficient,

The effects of the positive and negative changes in margin requirement on the conditional long-run volatility are captured by the coefficients,

In addition, the coefficients,

Overall, our results show that the negative changes in margin requirement decrease long-run volatilities, while the higher margin requirements increase short-run volatilities in the Japanese stock market. This implies that, similar to Sohn and Kim (2009), if Japanese financial authority intends to increase margin level to reduce volatility, unexpectedly, short-run volatility would be even higher.

Recent studies (Hardouvelis and Theodossiu, 2002; Sohn and Kim, 2009) examine the asymmetric effect of margin requirements in the bull and bear markets. It is also of interest to examine how margin requirements influence long-run and short-run volatilities in the bull and bear markets.11 To do so, we extend the asymmetric CGARCH model as:

where

Table 7 illustrates the estimated results of equations (13) - (15). The effects of the changes in margin requirement in the bull and bear markets on the conditional long-run volatility are captured by the coefficients,

Furthermore, the coefficients,

Overall, our finding is similar to those of Sohn and Kim (2009) who find that during bear periods, margin requirement policy is not effective for reducing volatility in the Japanese stock market.

9)We also examine the effect of the level of margin requirement as in  is the level of margin requirement when margin requirement is increased (decreased) at day t-1 and remains until next changes in margin requirement.

is the level of margin requirement when margin requirement is increased (decreased) at day t-1 and remains until next changes in margin requirement.

10)We do not examine whether or not raising margin requirement reduces the participation of irrational investors or rational investors as in the previous studies because it is beyond our scope. We leave this in the future study.

11)We also thank an anonymous referee for pointing this out.

12)We define a bull or a bear market as follows: a period during which there are at least 3 consecutive monthly stock returns with same algebraic sign, after constructing monthly stock returns using stock indices at the end of each month.

13)We calculate the correlation coefficients between NIKKEI225 and the level of margin requirement and between TOPIX and the level of margin requirement. The estimated correlations are 0.460 and 0.479, respectively.

VI. Concluding remarks

The purpose of this paper is to examine the effect of initial margin requirements on long-run and short-run volatilities in the Japanese stock market using the Component GARCH model, whose advantage is to decompose market volatility into the short-run component and the long-run component. We choose the Japanese stock market for examining the effect of initial margin requirements for two reasons: frequent revision of margin requirements and high proportion of margin transactions in total transactions in Japan.

This study is important for investors and policy makers to have more insights for the effect of initial margin requirements. According to the pyramiding-depyramiding process, which takes for granted the presence of rational and irrational investors in the stock market, the effect of initial margin requirements depends on which investors' participations are more restricted by the changes in margin requirements. To this end, we adopt the various Component GARCH models.

When we use the margin dummy and the level of margin requirement without dividing them into the positive and negative changes or into the bull and bear markets, we find that increasing margin requirement is effective for reducing long-run volatility, while not effective in short-run volatility, which is inconsistent with the result of Hardouvelis and Peristiani (1992) who find that margins effectively moderate volatility in the short-run using the daily returns.

By dividing the changes in margin requirement into the positive and negative changes, we find that the negative changes in margin requirements decrease long-run volatilities, while the higher margin requirements increases short-run volatilities in the Japanese stock market, similar to Sohn and Kim (2009). This suggests that if the Japanese financial authority increases margin to reduce volatility, it could face higher short-run volatility.

In addition, we divide the sample period into the bull and bear periods to examine the possible asymmetric effect of margin requirement in long-run and short-run volatilities, similar to Hardouvelis and Theodossiu (2002) and Sohn and Kim (2009). The overall result shows that during bear periods, margin requirement policy is not effective for reducing volatility in the Japanese stock market, similar to those of Sohn and Kim (2009).

14)Note that in the margin dummy, we do not consider the degree of margin changes. Therefore, the difference between the changes in margin requirement and the level of margin requirement could be affected by the scale effect of margin requirement.

Tables & Figures

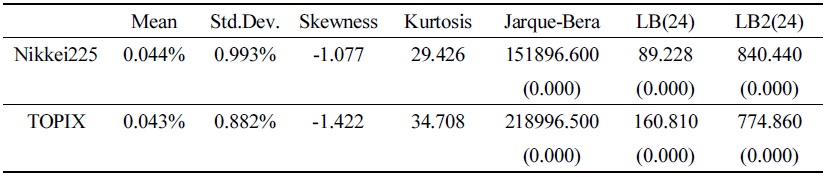

Table 1.

Descriptive Statistics

Note: This table reports the basic statistics for daily returns of NIKKEI225 and TOPIX. In this table, ‘Kurtosis’ indicates the excess kurtosis. In addition, LB(24) and LB2(24) are Ljung-Box statistics for up to 24 lags for returns and squared returns, respectively. Significance levels are in parentheses.

Figure 1.

Initial Margin Requirement in the Japanese Stock Market

Table 2.

Results of the Unit Root Tests for Margin Requirement

Note: * and ** indicate significance at 5% and 1% level. The null hypothesis for the ADF test is that margin requirement has a unit root, while that of the KPSS test is that margin requirement is stationary.

Table 3.

CGARCH Estimation Results without Margin Requirements

Note: * and ** indicate significance at 5% and 1% levels, respectively. t-statistics are presented in parentheses, while significance levels are presented in brackets. SR LB(24) and SSR LB2(24) are Ljung-Box statistics for up to 24 lags for standard residuals and squared standard residuals, respectively.

Table 4.

CGARCH Estimation Results with Margin Requirements

Note: * and ** indicate significance at 5% and 1% levels, respectively. SR LB(24) and SSR LB2(24) are Ljung-Box statistics for up to 24 lags for standard residuals and squared standard residuals, respectively.

Table 5.

Asymmetric CGARCH Estimation Results with Margin Requirements

Note: * and ** indicate significance at 5% and 1% levels, respectively. SR LB(24) and SSR LB2(24) are Ljung-Box statistics for up to 24 lags for standard residuals and squared standard residuals, respectively.

Table 6.

Asymmetric CGARCH Estimation Results with Positive and Negative Margin Requirements.

Note: * and ** indicate significance at 5% and 1% levels, respectively. SR LB(24) and SSR LB2(24) are Ljung-Box statistics for up to 24 lags for standard residuals and squared standard residuals, respectively.

Table 7.

CGARCH Estimation Results with the Bull and Bear Market Dummies.

Note: * and ** indicate significance at 5% and 1% levels, respectively. SR LB(24) and SSR LB2(24) are Ljung-Box statistics for up to 24 lags for standard residuals and squared standard residuals, respectively.

References

-

Black, A. and D. G. McMillan. 2004. “Long run trends and volatility spillovers in daily exchange rates.”

Applied Financial Economics , vol. 14, issue 12, pp. 895-907.

- Christoffersen, P., Jacobs, K. and Y. Wang. 2004. “Option valuation with long-run and short-run volatility components,” CIRANO Working Papers 2004s-56. Mantreal: CIRANO

-

DeLong, J. B., Shleifer, A., Summers, L. H. and R. J. Waldmann. 1990. “Noise trader risk in financial markets,”

Journal of Political Economy , vol. 98, no. 4, pp. 703-738.

-

Engle, R., and G. Lee. 1999. “A permanent and transitory component model of stock return volatility,” in R. Engle and H. White (ed.),

Cointegration, causality, and forecasting: A festschrift in honor of Clive W. J. Granger , Oxford: Oxford University Press, pp. 475-497. - Garbade, K. D. 1982. “Federal reserve margin requirements: A regulatory initiative to inhibit speculative bubbles,” in Paul Wachtel (ed.), Crises in economic and financial structure, Lextington, MA: Lexington books.

-

Hardouvelis, G. A. 1990. “Margin requirements, volatility, and transitory component of stock prices,”

American Economic Review , vol. 80, no. 4, pp. 736-762. -

Hardouvelis, G. A. and P. Theodossiou. 2002. “The asymmetric relation between initial margin requirements and stock market volatility across bull and bear markets,”

Review of Financial Studies , vol. 15, no. 5, pp. 1525-1559.

-

Hardouvelis, G. A., and S. Peristiani. 1992. “Margin requirements, speculative trading, and stock price fluctuations: The case of Japan,”

Quarterly Journal of Economics , vol. 107, no. 4, pp. 1333-1370.

-

Harvey, C. R. 1989. “Time-varying conditional covariances in tests of asset pricing models,”

Journal of Financial Economics , vol. 24, issue 2, pp. 289-317.

-

Hsieh, D. A. and M. H. Miller. 1990. “Margin regulation and stock market volatility,”

Journal of Finance , vol. 45, no. 1, pp. 3-29.

-

Kim, K. A. and H. R. Oppenheimer. 2002. “Initial margin requirements, volatility, and the individual investor: Insight from Japan,”

Financial Review , vol. 37, issue 1, pp. 1-16.

-

Kumar, R., Ferris, S. and D. Chance. 1991. “The differential impact of federal reserve margin requirements on stock return volatility,”

Financial Review , vol. 26, issue 3, pp. 343-366.

-

Kupiec, P. H. 1989. “Initial margin requirements and stock returns volatility: Another look,”

Journal of Financial Services Research , vol. 3, issue 2-3, pp. 287-301.

-

Kwiatkowski, D. P., Phillips, C. B., Schmidt, P. and Y. Shin. 1992. “Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root?,”

Journal of Econometrics , vol. 54, issue 1-3, pp. 159-178.

-

Lee, C. I. and I. Mather. 1999. “Efficiency tests in the Spanish futures markets,”

Journal of Futures Markets , vol. 19, issue 1, pp. 59-77. -

Schwert, G. W. 1989a. “Margin requirements and stock volatility,”

Journal of Financial Services Research , vol. 3, issue 2-3, pp. 153-164.

- Schwert, G. W. 1989b. “Business cycles, financial crises and stock volatility,” NBER working paper, No. 2957, National Bureau of Economic Research.

- Sohn, P.-D. and S.-S. Kim. 2009. “On relationship between initial margin requirements and volatility: New evidence from Japan Stock Market,” Joint conference of five finance association, May 2009. Cheonan, Korea.

-

Turner, C. M., Startz, R. and C. R. Nelson. 1989. “A Markov model of keteroskedasticity, risk and learning in the stock market,”

Journal of Financial Economics , vol. 25, issue 1, pp. 3-22.

-

Watanabe, T. and K. Harada. 2006. “Effects of the Bank of Japan’s intervention on yen/dollar exchange rate volatility,”

Journal of Japanese International Economics , vol. 20, issue 1, pp. 99-111.