- EAER>

- Journal Archive>

- Contents>

- articleView

Contents

Citation

| No | Title |

|---|

Article View

East Asian Economic Review Vol. 28, No. 2, 2024. pp. 221-244.

DOI https://dx.doi.org/10.11644/KIEP.EAER.2024.28.2.435

Number of citation : 0View

52

Download

35

Monetary Policy Independence during Reversal Phases of Domestic-Foreign Interest Rate Differentials

|

|

Hongik University |

|---|

Abstract

This study examines how the independence of monetary policy changes in situations where the interest rate differential between domestic and foreign rates inverts, utilizing the trilemma indices. For analysis, this paper uses the trilemma indices developed by

JEL Classification: E52, F31, F36, F41

Keywords

Monetary Policy Independence, Exchange Rate Stability, Capital Account Openness, Trilemma, Interest Rate Differentials

I. Introduction

The 2008 global financial crisis, which originated from the U.S. subprime mortgage crisis, not only had an immediate and significant impact on the U.S. economy but also delivered a substantial blow to the global economy through integrated financial markets. In response, the U.S. not only implemented traditional monetary policy measures, such as cutting the Federal Funds Rate, but also resorted to the unconventional measure of quantitative easing to address the crisis. Starting at 5.25% in August 2007, the Federal Funds Rate was reduced by 3 percentage points to 2.25% within just seven months, by March 2008, and continued to decrease steadily, reaching virtually zero levels by December 2008 (Figure 1).

Korea was not exempt from the impacts of the global financial crisis, prompting the Bank of Korea to swiftly respond by utilizing its base interest rate tool. The policy rate in Korea, which stood at 5.25% in September 2008, began to rapidly decline, dropping by 3 percentage points to 2.25% within just four months, by January 2009. Unlike the U.S., Korea’s policy rate did not reach zero levels, but it remained at a historically low level of 2% throughout 2009.

The global financial crisis triggered widespread interest rate cuts across the globe. Numerous countries enacted significant reductions in interest rates around the same time, which continued to decrease steadily thereafter, remaining at low levels for an extended period. The U.S. began to increase the Federal Funds Rate in December 2015, a full 8 years and 4 months after initiating cuts. In Korea, unlike in the U.S., there was a period from the second half of 2010 to the first half of 2011 when the policy rate increased. However, it consistently declined again after that period. It was not until November 2017 that the policy rate began to rise slightly.

The process of normalizing monetary policies in both Korea and the U.S. began in earnest in 2018, as interest rates in both countries started to rise. However, there were differences in the pace of normalization between the two. As illustrated in Figure 1, the U.S. began raising rates before Korea’s rate hikes took full effect, and did so at a faster pace. Consequently, from March 2018 to February 2020, Korea’s policy rate remained below the U.S. Federal Funds Rate for a period of 24 months. The situation where Korea’s interest rates are lower than those of the U.S. is referred to as an “interest rate differential inversion (or reversal)” in this paper.

The inversion of interest rate differentials between Korea and the U.S. is a situation that the Bank of Korea has been concerned about, as it could potentially trigger rapid exchange rate fluctuations and significant capital outflows. This concern is evident in the discussions recorded in the minutes of the 10th Monetary Policy Committee meeting held on May 28, 2018. At that time, the inversion of interest rates between Korea and the U.S., which began in March of the same year, was a topic of concern among the committee members. They also shared their monitoring of relevant indicators. Some members assessed that, as of May 2018, Korea was not in a recession but was experiencing a slowdown or a downward phase of the economic cycle. Considering the potential for capital outflows due to the interest rate differential, there was a need for an interest rate hike rather than a cut. However, the domestic economic cycle made it difficult to decide on raising rates, highlighting the complexity of the situation at that time.

In the period of interest rate inversion between Korea and the U.S. that began in September 2022, we can observe continued deliberations similar to those faced by monetary authorities in 2018, as detailed in the minutes of the 19th Monetary Policy Committee meeting of 2022, held on October 12. The Federal Open Market Committee (FOMC) in September 2022 took an unusual giant step by raising interest rates by 0.75 percentage points in response to rapidly rising inflation. This widened the gap in the interest rate differential inversion, and like in May 2018, members of Korea’s Monetary Policy Committee highlighted the need to consider the increased volatility in exchange rates and the inflow and outflow of foreign capital as financial center countries’ policy rates accelerated. Furthermore, they diagnosed that the domestic economy was cooling off rapidly in September 2022, indicating the challenges faced by monetary authorities in using the base rate as a policy tool, similar to the situation in 2018.

According to the Mundell-Fleming model’s trilemma, central banks cannot simultaneously achieve three policy objectives: monetary policy independence, capital account openness, and exchange rate stability. Instead, only two of these objectives can be achieved at any given time. This means that monetary policy independence can be secured either by adopting a flexible exchange rate system, thereby forgoing exchange rate stability, or by controlling free capital flows. However, as observed in the Korean case, the interest rate differential inversion occurs due to rapid interest rate hikes in financial centers. Although securing monetary policy independence is possible in theory, in practice, it does not necessarily enable the central bank to make monetary policy decisions based solely on domestic factors. This paper aims to analyze whether monetary policy independence can be secured in situations of interest rate differential inversion by reducing either exchange rate stability or the degree of capital account openness, as the trilemma traditionally suggests.

This analysis utilizes the monetary policy independence index introduced by Kim et al. (2017), which constructed trilemma indices for 45 countries from 2002 to 2013. The trilemma indices consist of a capital account openness index, an exchange rate stability index, and a short-term interest rate independence index, which is a monetary policy independence index in Kim et al. (2017). This paper uses updated trilemma indices of Kim et al. (2017) up to 2018 (Kim and Kim, forthcoming) and evaluates the independence of monetary policies across 45 countries, as well as analyzes the relationships among the short-term interest rate independence index and the other two trilemma indices.

The empirical result shows that, similar to the findings of Kim et al. (2017), the trilemma still holds well even when extending the analysis period. Specifically, the short-term interest rate independence index shows a statistically significant negative correlation with both the capital account openness index and the exchange rate stability index. Interestingly, during periods when domestic and foreign interest rate differentials reverse, the trilemma does not hold. Specifically, the statistically significant negative correlation between the short-term interest rate independence index and the exchange rate stability index disappears. This is because, in some countries during these reversal periods, a positive correlation between the exchange rate stability index and the short-term interest rate independence index is observed.

Particularly notable is that this effect becomes pronounced when the reversed interest rate differential exceeds a certain threshold. This indicates that economies maintaining stable exchange rates, despite lower domestic interest rates compared to foreign rates, are effectively managing their monetary policies to appropriately respond to economic conditions. This effectiveness is captured in the short-term interest rate independence index.

Even during periods of reversed interest rate differentials, the statistically significant trade-off between the monetary policy independence index and the capital account openness index was estimated. That is, even during periods of interest rate differential reversal, a decrease in the capital account openness index is closely associated with an increase in the monetary policy independence index. This suggests that the dilemma of Rey (2013), which posits that monetary policy in open financial markets is influenced by monetary policy in financial centers regardless of the exchange rate regime, may be more applicable than the trilemma during these periods.

This study contributes to the existing literature by introducing an intuitive and highly utilizable index for evaluating the independence of monetary policy. While previous studies (Aizenman et al., 2008, 2010, 2011, 2013, 2016, 2017; Aizenman and Ito, 2014) have examined the independence of monetary policy using trilemma indices, focusing on periods of reversed interest rate differentials distinguishes this research from existing works. Additionally, there is another contribution to existing research by analyzing recent periods of rapid changes in interest rates differentials among countries using the updated trilemma indices.

The remainder of this paper is organized as follows: Section II explains the trilemma indices and discusses the data used to construct the indices. Section III evaluates the independence of monetary policy using the constructed indices, and Section IV performs empirical analysis on the factors influencing the short-term interest rate independence index during periods of interest rate differential reversal. Finally, Section V concludes the analysis.

II. Trilemma Indices

1. Indices

We utilize the Short-term Interest Rate Independence Index (SRI) from Kim et al. (2017) as our measure of monetary policy independence. This index reflects the extent to which short-term interest rates in each country move in tandem or independently of those in the base country. SRI is calculated using the following equation (Equation 1).

The subscript  denotes the short-term interest rate of country

denotes the short-term interest rate of country  represents the short-term interest rate of the base country for country

represents the short-term interest rate of the base country for country  1

1

The remaining two indices constituting the trilemma indices, namely the capital account openness index (KA) and the exchange rate stability index (ERS), were constructed in the same manner as Kim et al. (2017). KA is constructed based on the capital control measure introduced by Fernández et al. (2016). ERS is formulated using the exchange rate regime classifications by Shambaugh (2004), Klein and Shambaugh (2008, 2010), and Obstfeld et al. (2010), illustrating the exchange rate stability of a country. A higher KA and ERS indicate greater financial market openness and higher exchange rate stability, respectively.

2. Data

Kim et al. (2017) constructed indices for SRI, KA, and ERS for 45 countries from 2002 to 2013 due to data availability constraints.2 Since then, the data used for index construction has been updated. In this study, following the approach of Kim et al. (2017), we use updated indices up to 2018 (Kim and Kim, forthcoming).3

The base country data for calculating the SRI and the classification of peg and soft peg used in calculating the ERS were derived from the same sources as those used in Kim et al. (2017), namely Shambaugh (2004), Klein and Shambaugh (2008, 2010), and Obstfeld et al. (2010).4 Additionally, SRI were obtained from OECD database.5 KA was computed using capital control measures from Fernández et al. (2016), consistent with Kim et al. (2017).

Table 1 presents a list of sample countries included in the analysis. It includes the country code (provided for identification purposes in the figures), a dummy variable indicating whether the country is advanced economy (henceforth AE or AEs), and whether it uses the Euro. It also shows the analysis period and the proportion of years during the sample period in which the interest rate differential was inverted for each country. While the method of constructing individual trilemma indices is the same as Kim et al. (2017), there are differences in some data sources. As a result, there may be slight differences in the composition of sample countries, but the number of sample countries remains the same at 45, and it is an unbalanced panel data.6 There is no special criterion for selecting sample countries; all countries with available data are included in the analysis.

In the case of Eurozone countries (Euro = 1), the short-term interest rates are generally the same, leading to no periods of reversed interest rate differentials. However, countries like Cyprus and Latvia, which joined the Eurozone later, experienced periods of interest rate differential inversion due to not using the Euro during certain periods within the analysis period. Germany, while part of the Eurozone, has the U.S. as its base country, unlike most other Eurozone countries where Germany serves as the base country. As a result, Germany experiences approximately 41% of the sample period with interest rate differentials inverted. Among the analyzed countries, including most Eurozone countries, 25 out of 45 countries, accounting for approximately 56%, never experienced a period of reversed interest rate differentials throughout the entire sample period. The remaining approximately 44% of countries experienced such reversals during the analysis period. Notably, Singapore and Switzerland consistently maintained lower levels compared to their base countries on an annual average basis during these periods.7

Figure 2 illustrates the proportion of countries experiencing a reversal in interest rate differentials annually from 2002 to 2018. Around one-third of the countries experienced a reversal in interest rate differentials in 2007, marking the year with the highest number of countries simultaneously experiencing such a reversal during the analysis period. Subsequently, from 2008 to 2010, this proportion decreased to around 12%, and by 2014, it decreased further to the low 4% range, indicating the lowest proportion of countries with a reversal in interest rate differentials during the analysis period.

In Figure 3, we compare the distribution of interest rate differentials between the years with the highest (2007) and lowest (2014) proportions of countries experiencing inversion. A noticeable difference is observed in the width of the area where interest rate differentials are negative, with 2007 exhibiting a wider range compared to 2014. In terms of numerical values, both the average and median in 2007 are 0.75 and 0, respectively, whereas in 2014, they are 2.08 and 1.05, showing differences of more than 1%p (percent point) for both statistics.

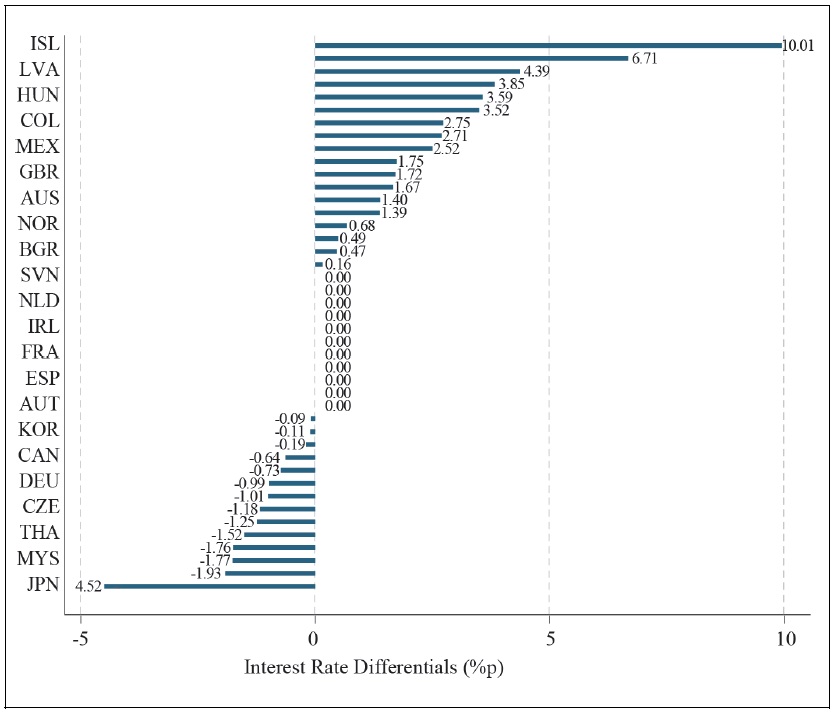

Figure 4 illustrates the interest rate differentials for each country in 2007 using a bar graph. As observed in Figure 1, out of 42 countries, 14 countries, experienced an inversion in interest rate differentials. It is evident from the graph that there is significant variation in the degree of interest rate differential inversion among countries. Japan exhibits the largest interest rate differential inversion, approximately 4.5%p. Following Japan are Switzerland, Malaysia, China, Thailand, and Singapore, indicating that some emerging Asian economies experienced substantial interest rate differential inversions in 2007.

1)The 36-month period was set to be consistent with

2)Moreover, in

3)The reason for extending only up to 2018 is that the data required for calculating the ERS is available only up to 2018. See Kim and Kim (forthcoming).

4)For further details on the ERS, please refer to

5)Short-term interest rates are derived from three-month money market rates whenever possible. Common standardized terms include “money market rate” and “treasury bill rate.” In some OECD countries where short-term interest rates are not available, the IMF International Financial Statistics (IFS)’s money market rate or deposit rate was utilized.

6)In comparison to

7)The base countries for Singapore and Switzerland were set as Malaysia and Germany, respectively

III. Evaluation of Monetary Policy Independence Using Indices

In Section II, we constructed the SRI to reflect monetary policy independence. In Section III, we aim to examine how monetary policy independence, reflected by the constructed SRI, has changed in terms of indicators representing periods with and without inverted interest rate differentials, and analyze its relationship with the other two trilemma indices.

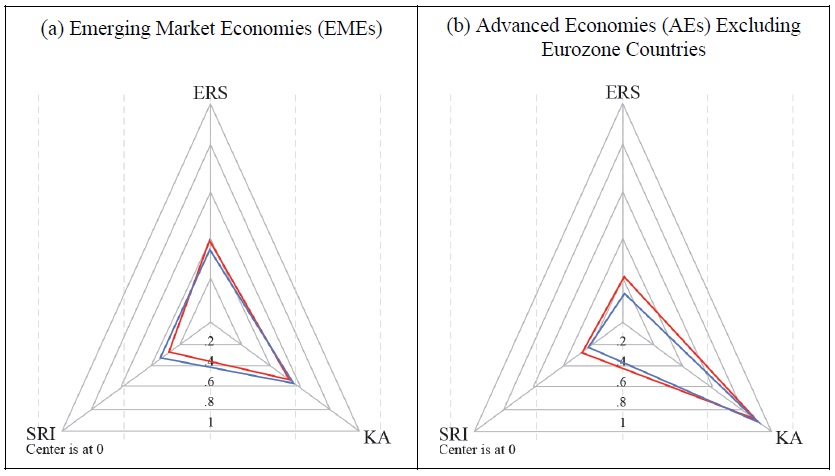

Figures 5 (a) and (b) below depict radar charts of the trilemma indices for emerging market economies (EMEs) and AEs, respectively. The blue solid line represents the trilemma indices (average value) for years with positive interest rate differentials, while the red solid line represents the trilemma indices for years with inverted interest rate differentials. Overall, compared to AEs (excluding the Eurozone), EMEs exhibit higher exchange rate stability, while AEs tend to have higher KA than EMEs. There are no significant differences in the SRI between the two country groups on average; however, differences are primarily observed at the individual country level.

In Figure 5, it can be observed that during periods of interest rate differential inversion, both EMEs and AEs experience an increase in the ERS. Given that the KA decreases for both groups of countries, it suggests that if the trilemma holds, achieving exchange rate stability comes at the cost of reduced KA. Regarding the SRI, notable differences exist between EMEs and AEs. While the SRI decreases for EMEs during periods of interest rate differential inversion, it shows a slight increase for AEs. This reflects the difficulty EMEs face in securing monetary policy independence, particularly during periods of interest rate differential inversion.

Table 2 examines whether there is a correlation between trilemma indices when divided into periods of interest rate differential inversion and periods without such inversion. The subscript ACI refers to the trilemma indices by Aizenman et al. (2010). The Monetary Independence index corresponding to the SRI in this paper is denoted as MI.8

During periods without interest rate differential inversion, there is a relatively clear negative correlation between SRI and KA, as well as between SRI and ERS (-0.6103 and -0.6886, respectively). Negative correlations are also observed in SRI-KAACI and SRI-ERSACI. Moreover, when considering MIACI instead of SRI, similarly high negative correlations among the indices can be observed. However, during periods of interest rate differential inversion, this negative correlation tends to diminish or even turn into a weak positive correlation. It varies depending on the index. This suggests that during periods of interest rate differential inversion, the trilemma may not hold.

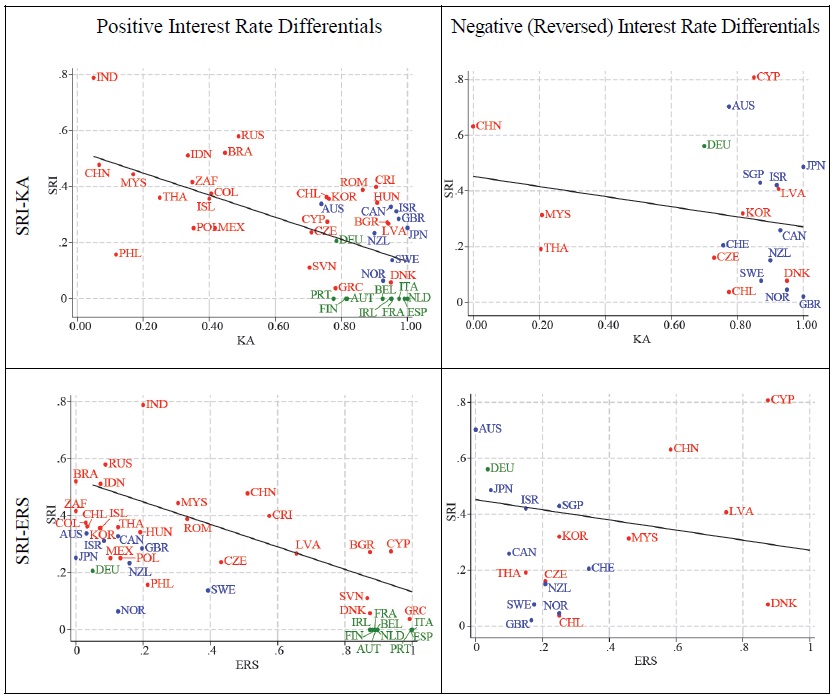

Figure 6 presents scatter plots to examine the relationship between SRI and the other two trilemma indices on a country-by-country basis. The sample period is divided into periods with and without interest rate differential inversion, and the average indices for each period are calculated to create the scatter plots. The correlations between SRI and KA, SRI and ERS observed on the graph differ noticeably between periods of positive interest rate differential and periods of interest rate differential inversion. During periods of positive interest rate differential, there appears to be a relatively clear negative correlation, suggesting a higher likelihood of the trilemma holding. However, during periods of interest rate differential inversion, these correlations seem to decrease significantly. Further empirical analysis is necessary for rigorous validation, which will be conducted in Section IV.

In summary, based on the combination of figures and tables in Section III, a slight decrease in the independence of monetary policy in EMEs during periods of inverted interest rate differentials has been observed. However, this decline in monetary policy independence appears to be difficult to explain solely through the trilemma framework. We will examine whether the trilemma holds during periods of inverted interest rate differentials and explore what factors influence monetary policy independence during these periods in the upcoming Section IV using empirical analysis with indices.

8)The correlation coefficient between MI and SRI is 0.8739

IV. Empirical Analysis

1. Model

The empirical model using trilemma indices for 45 countries from 2002 to 2018 is represented by the following Equations (2-1) and (2-2).

The model reflects the monetary policy independence, with SRI as the dependent variable and the remaining trilemma indices, KA and ERS, as explanatory variables. If the trilemma holds, both

To account for the potential impact of the degree of inverted interest rate differentials on SRI, we will conduct additional empirical analysis by including the variable  instead of Ι

instead of Ι and the short-term interest rate of country

and the short-term interest rate of country  multiplied by the dummy variable Ι

multiplied by the dummy variable Ι

Equation (2-1) and Equation (2-2) serve as the benchmark model specifications for the empirical analysis. However, we will start from a simple model and gradually add variables to employ various empirical models for hypothesis testing. Additionally, we will verify the robustness of the results by excluding some country groups.

Table 3 presents the descriptive statistics of the trilemma indices, categorized into periods with and without reversals in the interest rate differential. Among the 45 countries in the sample, 20 countries experienced interest rate differential reversals during the analysis period. Conversely, Singapore and Switzerland consistently exhibited lower short-term interest rates than their base countries throughout the analysis period, thus, for the periods when interest rate differentials did not reverse, the statistics are presented as the annual average of countries excluding these two. Since the indices themselves are normalized between 0 and 1, noticeable outliers are not observed.

2. Results

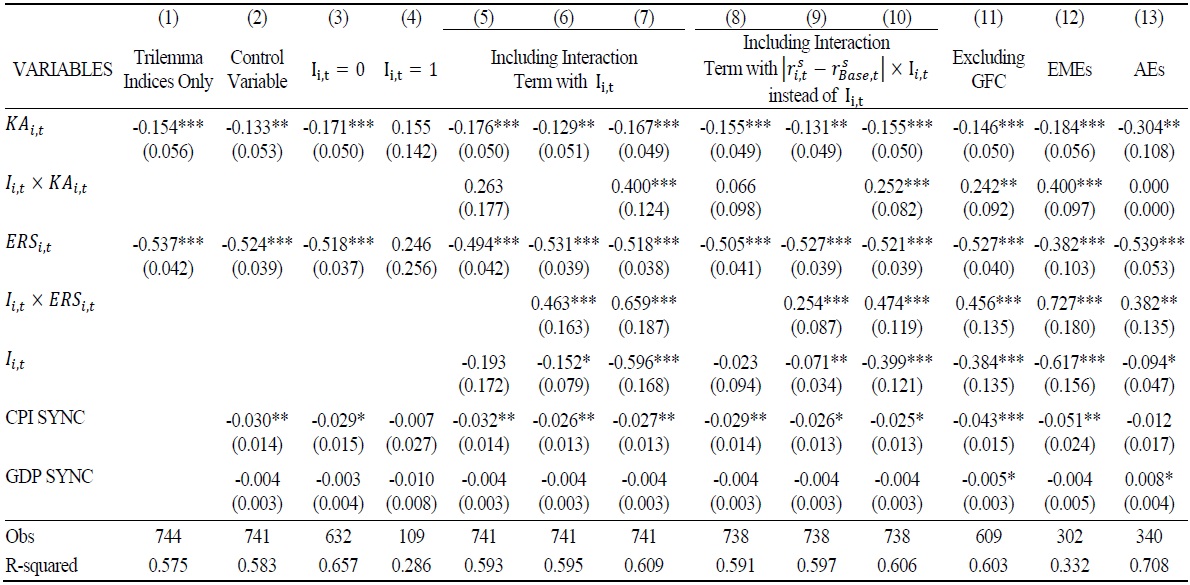

The empirical analysis results are presented in Table 4. In (1), the results are based on including only trilemma indices as explanatory variables, excluding separate dummy variables indicating the reversal of interest rate differentials and control variables (including intercept and time fixed effects). It is observed that the coefficients for KA and ERS are negative and statistically significant, indicating trade-off correlations between each index and SRI, thereby confirming the existence of trilemma. These negative correlations are also evident in the model including control variables, as shown in (2).

(3) and (4) present the results of empirical analysis conducted using the dataset used in (2), divided into periods where the interest rate differential is inverted and those where it is not. During periods when the interest rate differential is not inverted, KA and ERS maintain a negative correlation with SRI. However, during periods of inverted interest rate differentials, this trend seems to dissipate.

(5) ~ (7) represent the empirical results of the econometric model presented in Equation (2-1). Firstly, in (5), the interaction term, Ιi,t ×

Therefore, it is necessary to pay attention to the results in (8) ~ (10) to verify whether the empirical findings from (5) ~ (7) remain robust when considering the empirical analysis that includes  instead of Ιi,t in Equation (2-2). Similarly to the previous results, only the term

instead of Ιi,t in Equation (2-2). Similarly to the previous results, only the term  is statistically significant and estimated to be positive. Thus, we can conclude that not only the presence but also the extent of inverted interest rate differentials are closely related to SRI.

is statistically significant and estimated to be positive. Thus, we can conclude that not only the presence but also the extent of inverted interest rate differentials are closely related to SRI.

(11) ~ (13) test whether the empirical findings so far remain robust even after excluding certain observations. Essentially, (11) ~ (13) include  instead of Ιi,t in Equation (2-2). First, in (11), the empirical analysis is performed excluding the period of the global financial crisis (GFC, 2008 ~ 2010), and the results exhibit robustness. Then, in (12), the analysis excludes 25 countries (all Eurozone countries excluding Cyprus and Latvia) that did not experience inverted interest rate differentials throughout the analysis period, and two countries (Singapore and Switzerland) that consistently exhibited lower short-term interest rates than their base countries throughout the analysis period. Since most of the excluded countries are Eurozone members, the remaining countries are mostly classified as EMEs. Consequently, they are referred to as EMEs. Although the statistical significance of the coefficient for ERS disappears in (12), the term

instead of Ιi,t in Equation (2-2). First, in (11), the empirical analysis is performed excluding the period of the global financial crisis (GFC, 2008 ~ 2010), and the results exhibit robustness. Then, in (12), the analysis excludes 25 countries (all Eurozone countries excluding Cyprus and Latvia) that did not experience inverted interest rate differentials throughout the analysis period, and two countries (Singapore and Switzerland) that consistently exhibited lower short-term interest rates than their base countries throughout the analysis period. Since most of the excluded countries are Eurozone members, the remaining countries are mostly classified as EMEs. Consequently, they are referred to as EMEs. Although the statistical significance of the coefficient for ERS disappears in (12), the term  is estimated to be positive and statistically significant. For comparison with (12), (13) presents the results of empirical analysis focusing only on AEs, excluding countries classified as EMEs. In this analysis, the statistical significance of KA disappears, but robust results are obtained again from the term

is estimated to be positive and statistically significant. For comparison with (12), (13) presents the results of empirical analysis focusing only on AEs, excluding countries classified as EMEs. In this analysis, the statistical significance of KA disappears, but robust results are obtained again from the term  consistent with the previous findings.

consistent with the previous findings.

Table 5 conducts robustness tests using the trilemma indices from Aizenman et al. (2010). Overall, the results are consistent with those in Table 4, with one notable difference: some of the analyses including interaction terms between KA and  show statistically significant and positive. Apart from this discrepancy, the findings align with those in Table 4, indicating that the main empirical results are highly robust.

show statistically significant and positive. Apart from this discrepancy, the findings align with those in Table 4, indicating that the main empirical results are highly robust.

To interpret the positive estimation of the interaction term between ERS and  a threshold analysis is conducted using the estimated results. To determine the marginal effect of a one-unit change in ERS on SRI in Equation (2-2), we differentiate both sides with respect to ERS. Then, by utilizing the estimated coefficients from Table 4 (10), we can proceed:

a threshold analysis is conducted using the estimated results. To determine the marginal effect of a one-unit change in ERS on SRI in Equation (2-2), we differentiate both sides with respect to ERS. Then, by utilizing the estimated coefficients from Table 4 (10), we can proceed:

According to Equation (3), in situations where the interest rate differential is reversed (Ιi,t = 1), an increase in ERS is associated with an increase in SRI if the reversed interest rate differential  exceeds 0.72%p. However, if the reversed interest rate differential does not exceed 0.72%p, the trade-off relationship between ERS and SRI still persists. Calculating this threshold using the estimated coefficients from Table 4 (9) ~ (13), the range is approximately estimated to be between 0.72%p and 1.32%p, excluding Table 4 (12) as it is not significant. Alternatively, when calculated using Table 5 (9) ~ (13), the threshold is estimated to be between 0.52%p and 2.12%p. In other words, in situations where the reversal of the interest rate differential exceeds this range, an increase in one unit of ERS may actually increase SRI.10

exceeds 0.72%p. However, if the reversed interest rate differential does not exceed 0.72%p, the trade-off relationship between ERS and SRI still persists. Calculating this threshold using the estimated coefficients from Table 4 (9) ~ (13), the range is approximately estimated to be between 0.72%p and 1.32%p, excluding Table 4 (12) as it is not significant. Alternatively, when calculated using Table 5 (9) ~ (13), the threshold is estimated to be between 0.52%p and 2.12%p. In other words, in situations where the reversal of the interest rate differential exceeds this range, an increase in one unit of ERS may actually increase SRI.10

The empirical analysis results presented above demonstrate correlations rather than causal relationships between trilemma indices. Therefore, caution is needed in interpreting policy implications. In situations where the interest rate differential is reversed (especially when the reversed interest rate differential exceeds a certain threshold), a positive correlation between exchange rate stability and monetary policy independence may indicate that despite low domestic interest rates, stable exchange rates suggest that the central bank is effectively managing monetary policy to respond appropriately to economic conditions. This could be interpreted as reflected in SRIi,t. Conversely, in economies where the exchange rate is not stable during periods of reversed interest rate differentials, a simultaneous decrease in exchange rate stability and monetary policy independence may occur. This could suggest that the index reflects the difficulty faced by the central bank in operating monetary policy solely based on domestic factors when the exchange rate is unstable.

Another interesting interpretation related to the empirical analysis results revolves around the coefficient of KA ( the coefficient of these interaction terms (

the coefficient of these interaction terms (

9)CPI and GDP synchronization indices capture the simultaneous fluctuations in CPI inflation and GDP growth forecast revisions for each country and its base country. These indices are developed in accordance with the methodologies of

10)The reason for the threshold being greater than zero appears to be due to the transaction costs involved in cross-border arbitrage. However, the primary research questions of the current study are to investigate whether the trilemma is applicable during periods of inverted interest rate differentials, hence the investigation of the threshold goes beyond the scope of this study. Research on this aspect will be reserved for future work.

V. Conclusions

In this study, we analyzed whether it is possible to secure monetary policy independence by reducing exchange rate stability or financial market openness during periods of reversed interest rate differentials, as traditionally predicted by the trilemma. To conduct the analysis, we utilized the monetary policy independence index introduced by Kim et al. (2017). The analysis period spans from 2002 to 2018, and unbalanced panel data consisting of 45 countries was used.

The empirical analysis using the index revealed that, similar to the findings of Kim et al. (2017), the trilemma still holds true even when extending the analysis period. However, during periods of reversed interest rate differentials, the trilemma no longer holds. In particular, no statistically significant negative correlation was found between the monetary policy independence index and exchange rate stability index. This is because a positive correlation between exchange rate stability and short-term interest rate independence indices is observed in some countries during these periods.

Especially noteworthy is that such effects become more pronounced when the widened interest rate differential exceeds a specific threshold (0.72%p ~ 1.32%p), as indicated by our estimation results. This suggests that in economies where interest rates are relatively low despite reversed interest rate differentials, stable exchange rates imply effective central bank management of monetary policy in response to economic conditions, reflecting in the monetary policy independence index.

Furthermore, during periods of reversed interest rate differentials, the statistically significant negative correlation between financial market openness and monetary policy independence indices remains consistent, similar to periods when the interest rate differential is not inverted. This indicates that even during periods of reversed interest rate differentials, the decrease in capital account openness is closely associated with an increase in monetary policy independence. Therefore, it can be argued that the dilemma of Rey (2013) holds greater validity during these periods compared to the traditional trilemma.

Tables & Figures

Figure 1.

Policy Rates of Korea and the U.S. (2004-2023)

Notes: Solid line represents Korea, while dotted line denotes the U.S. The shaded area indicates interest rate differentials (= Korea policy rate ‒ US policy rate).

Source: Bank for International Settlements (BIS).

Table 1.

Country List

Note: Cyprus, Latvia, and Slovenia started using the Euro in 2008, 2014, and 2007, respectively. All Eurozone countries (“Euro”) except these three used the Euro throughout the entire sample period. “AE” denotes developed countries according to the MSCI (Morgan Stanley Capital International) criteria, and the reversed interest rate differential ratio represents the proportion of years during the sample period in which the interest rate differential was inverted for each country. Base countries are taken from

Figure 2.

Proportion of Countries Experiencing Reversal in Interest Rate Differentials

Note: Interest Rate Differential (%p) = Domestic Short-term Interest Rate ‒ Base Country’s Short-term Interest Rate. Solid lines represent the proportion (%) of countries with negative interest rate differentials each year.

Figure 3.

Distributions of Interest Rate Differentials (2007 vs 2014)

Note: Interest Rate Differential (%p) = Domestic Short-term Interest Rate ‒ Base Country’s Short-term Interest Rate.

Figure 4.

Interest Rate Differential in 2007

Note: Interest Rate Differential (%p) = Domestic Short-term Interest Rate ‒ Base Country’s Short-term Interest Rate.

Figure 5.

Trilemma Indices: Positive vs. Negative Interest Rate Differentials

Notes: Interest Rate Differential (%p) = Domestic Short-term Interest Rate ‒ Base Country’s Short-term Interest Rate. The blue solid line represents periods with positive interest rate differentials (i.e., domestic short-term interest rate exceeding the base country’s short-term interest rate), while the red solid line represents periods with negative interest rate differentials. ERS = Exchange Rate Stability Index, KA = Capital Account Openness Index, SRI = Short-term Interest Rate Independence Index.

Table 2.

Correlations among the Trilemma Indices

Note: Interest Rate Differential (%p) = Domestic Short-term Interest Rate ‒ Base Country’s Short-term Interest Rate. KA = Capital Account Openness Index, ERS = Exchange Rate Stability Index, SRI = Short-term Interest Rate Independence Index, KAACI, ERSACI, and MIACI are the capital account openness, exchange rate stability, and monetary policy independence indexes, respectively.

Source:

Figure 6.

Scatter Plots: Positive vs. Negative Interest Rate Differentials

Notes: Interest Rate Differential (%p) = Domestic Short-term Interest Rate ‒ Base Country’s Short-term Interest Rate. KA = Capital Account Openness Index, ERS = Exchange Rate Stability Index, SRI = Short-term Interest Rate Independence Index. Red denotes emerging markets economies, blue represents advanced economies excluding the Eurozone, and green signifies advanced economies within the Eurozone.

Table 3.

Summary Statistics for the Trilemma Indices: Positive vs. Negative Interest Rate Differentials

Notes: Interest Rate Differential (%p) = Domestic Short-term Interest Rate ‒ Base Country’s Short-term Interest Rate. KA = Capital Account Openness Index, ERS = Exchange Rate Stability Index, SRI = Short-term Interest Rate Independence Index, SD = Standard Deviation, p5 = 5th percentile, p25 = 25th percentile, p50 = 50th percentile, p75 = 75th percentile, p95 = 95th percentile.

Table 4.

Main Result

Notes: Clustered standard errors are reported in the parentheses; *, **, and *** indicate significance at the 10%, 5%, and 1% levels, respectively. SRI = Short-term Interest Rate Independence Index, KA = Capital Account Openness Index, ERS = Exchange Rate Stability Index, CPI SYNC = CPI inflation synchronization measure, GDP SYNC = GDP growth synchronization measure. GFC = Global Financial Crisis, EMEs = Emerging Market Economies, AEs = Advanced Economies. The intercept term and time fixed effects were included.

Table 5.

Robustness Check

Notes: Clustered standard errors are reported in the parentheses; *, **, and *** indicate significance at the 10%, 5%, and 1% levels, respectively. SRI = Short-term Interest Rate Independence Index, KA = Capital Account Openness Index, ERS = Exchange Rate Stability Index, CPI SYNC = CPI inflation synchronization measure, GDP SYNC = GDP growth synchronization measure. GFC = Global Financial Crisis, EMEs = Emerging Market Economies, AEs = Advanced Economies. The intercept term and time fixed effects were included.

References

- Aizenman, J., Chinn, M. D. and H. Ito. 2008. “Assessing the Emerging Global Financial Architecture: Measuring The Trilemma’s Configuration Over Time.” NBER Working Papers, no. 14533. National Bureau of Economic Research.

-

Aizenman, J., Chinn, M. D. and H. Ito. 2010. “The emerging global financial architecture: Tracing and evaluating new patterns of the trilemma configuration.”

Journal of International Money and Finance , vol. 29, no. 4, pp. 615-641.

-

Aizenman, J., Chinn, M. D. and H. Ito. 2011. “Surfing the waves of globalization: Asia and financial globalization in the context of the trilemma.”

Journal of the Japanese and International Economies , vol. 25, no.3, pp. 290-320.

-

Aizenman, J., Chinn, M. D. and H. Ito. 2013. “The ‘Impossible Trinity’ Hypothesis in an Era of Global Imbalances: Measurement and Testing.”

Review of International Economics , vol. 21, no. 3, pp. 447-458.

-

Aizenman, J., Chinn, M. D. and H. Ito. 2016. “Monetary policy spillovers and the trilemma in the new normal: Periphery country sensitivity to core country conditions.”

Journal of International Money and Finance , vol. 68, pp. 298-330.

- Aizenman, J., Chinn, M. D. and H. Ito. 2017. “Financial Spillovers and Macroprudential Policies.” NBER Working Papers, no. 24105. National Bureau of Economic Research.

-

Aizenman, J. and H. Ito. 2014. “Living with the trilemma constraint: Relative trilemma policy divergence, crises, and output losses for developing countries.”

Journal of International Money and Finance , vol. 49, no. A, pp. 28-51.

-

Bank of Korea. 2018. “Minutes of the Monetary Policy Committee Meeting (May 2018).”

https://www.bok.or.kr/eng/bbs/E0001620/view.do?nttId=10045799&menuNo=400021&pageIndex=5 -

Bank of Korea. 2022. “Minutes of the Monetary Policy Committee Meeting (October 2022).”

https://www.bok.or.kr/eng/bbs/E0001620/view.do?nttId=10073849&menuNo=400021&pageIndex=2 -

Fernández, A., Klein, M. W., Rebucci, A., Schindler, M. and M. Uribe. 2016. “Capital Control Measures: A New Dataset.”

IMF Economic Review , vol. 64, no. 3, pp. 548-574.

-

Kalemli-Ozcan, S., Papaioannou, E. and F. Perri. 2013. “Global Banks and Crisis Transmission.”

Journal of International Economics , vol. 89, no. 2, pp. 495-510.

-

Kim, K. and J. H. Pyun. 2018. “Exchange rate regimes and the international transmission of business cycles: Capital account openness matters.”

Journal of International Money and Finance , vol. 87, pp. 44-61.

- Kim, K., Kim, S., Yang, D. Y. and E. Kang. 2017. “The Effect of Financial Market Integration on Monetary Policy and Long-term Interest Rate in Korea and Its Policy Implications.” KIEP Policy Analyses, no. 17-11. Korea Institute for International Economic Policy. (in Korean)

-

Kim, K. and S. Kim. forthcoming. “Trilemma versus Dilemma: Monetary Autonomy and Long-term Interest Rate Independence.”

Review of International Economics . -

Klein, M. W. and J. C. Shambaugh. 2008. “The Dynamics of Exchange Rate Regimes: Fixes, Floats, and Flips.”

Journal of International Economics , vol. 75, no. 1, pp. 70-92.

- Klein, M. W. and J. C. Shambaugh. 2010. Exchange Rate Regimes in the Modern Era. MIT Press.

-

Obstfeld, M., Shambaugh, J. C. and A. M. Taylor. 2010. “Financial Stability, the Trilemma, and International Reserves.”

American Economic Journal: Macroeconomics , vol. 2, no. 2, pp. 57-94.

-

Rey, H. 2013. “Dilemma not trilemma: the global financial cycle and monetary policy independence.” Paper presented at the Jackson Hole Economic Policy Symposium. Wyoming. August 21, 2013. Federal Reserve Bank of Kansas City.

https://www.kansascityfed.org/Jackson%20Hole/documents/4575/2013Rey.pdf -

Shambaugh, J. C. 2004. “The Effect of Fixed Exchange Rates on Monetary Policy.”

Quarterly Journal of Economics , vol. 119, no. 1, pp. 301-352.