- EAER>

- Journal Archive>

- Contents>

- articleView

Contents

Citation

| No | Title |

|---|

Article View

East Asian Economic Review Vol. 29, No. 2, 2025. pp. 201-241.

DOI https://dx.doi.org/10.11644/KIEP.EAER.2025.29.2.448

Number of citation : 0View

51

Download

49

The Moderating Role of Shariah Compliance on the Relationship between Ethical Commitment and Corruption in Malaysian Companies

|

|

Universiti Malaysia Terengganu |

|---|---|

|

|

Universiti Malaysia Terengganu |

|

|

Universiti Teknologi Mara Cawangan Terengganu |

|

|

Kaneka Malaysia Sdn. Bhd. |

Abstract

Corporate ethics and corruption have garnered academic attention in recent decades. This study aims to gain insight into the relationship between ethical commitment and corruption and examine the moderating effect of Shariah compliance on this relationship. This study used 453 Malaysian companies from 2012 to 2021. The results indicate that a strong ethical commitment helps prevent management and employees from engaging in unethical behaviors that can lead to corruption within the company. However, the effect of ethical commitment on reducing corruption remains consistent, irrespective of a company’s Shariah-compliant status. For the separating samples based on the pre- and post-Malaysian Code of Corporate Governance (MCCG) 2017, the result shows no differences in the relationship between ethical commitment and corruption. However, Shariah compliance companies were found to reduce corruption in the post-MCCG 2017 period. This implies that improving the corporate governance structure seems to better influence corruption levels in Shariah compliance companies. This study contributes to the growing literature on corporate ethics and corruption by empirically examining the role of ethical commitment in mitigating corruption within the context of Malaysian companies. It provides novel evidence on how Shariah compliance influences this relationship, particularly in light of recent regulatory changes brought about by the Malaysian Code of Corporate Governance (MCCG) 2017.

JEL Classification: D73, G38, M14, K42

Keywords

Ethical Commitment, Shariah-Compliance, Corruption

I. Introduction

Academic interest in the field of corporate ethics and corruption has increased significantly over the past few decades. There is strong evidence that corporations can hurt society. Corporate scandals and crimes are characterized by unethical and morally distasteful behavior (Alcadipani and de Oliveira Medeiros, 2020) that can harm individuals, communities, firms, and nations. The unethical behavior has harmed the firm's reputation, decreasing investor trust and integrity. Moreover, corporate crime and scandals have resulted in considerable financial losses due to various misconducts and violations of the firm’s code of ethics and insufficient corporate governance within the corporation (Setiawan et al., 2020; Johari et al., 2022).

One of the primary controversies in this field is the interaction between ethical leadership and individual personality traits, such as Machiavellianism. Research by Manara et al. (2023) suggests that ethical leadership can significantly reduce corruption, particularly among followers with low Machiavellian tendencies. It shows that although ethical leadership is crucial, its efficacy may depend on the characteristics of the followers. In contexts characterized by individuals with darker personality traits, the efficacy of ethical leadership may be reduced, prompting questions about the universality of ethical leadership as a remedy for corruption. Moreover, the ethical climate within organizations plays a critical role in shaping employees’ behaviors. Liyanapathirana and Akroyd (2022) highlight that in contexts with high levels of corruption, the ethical decision-making of accountants is heavily influenced by the prevailing ethical climate. Addressing this issue requires a multifaceted approach that combines ethical leadership, effective training, and strong institutional frameworks to rebuild trust in public and private institutions.

In another perspective, corporate corruption occurs when employees, managers, or executives utilize their positions to their advantage. According to Aguilera and Vadera (2008), abusing authority is a major component of all types of corruption. More specifically, Vasconcelos (2023) emphasizes corporate wrongdoing as a form of organizational incivility on par with the lack of respect displayed by corporations whose leaders are selfish and unscrupulous toward society. Without a commitment to ethical values, individuals are more likely to engage in corrupt practices or unethical behavior, particularly when such actions go unchecked. Therefore, the leader’s enforcement of ethical behavior is part of the ethical commitment that shows the company’s dedication to fostering ethical behavior. The policy design by the company represents the ethical commitment that the employees should follow as a preventive measure against corruption incidents.

According to Halamka and Teplý (2017) and Baah et al. (2024), ethical organizations contribute to the growth of profits. It indicates that an ethical commitment significantly impacts the level of corruption and performance of the company. In view of sustainable development, people have a huge commitment to society regarding sustainability practices that force society to become faithful and honest in all aspects of life through the important elements of responsibility and empowerment (Ismail and Rasid, 2017, 2022). The lack of a strong ethical culture and transparent reporting mechanisms exacerbates the issue, creating a gap between the ethical standards outlined in corporate policies and the actual practices within organizations. Therefore, to combat global corruption and preserve international peace and peacekeeping efforts, companies are required to uphold ethics (Rendtorff, 2023) by ensuring that employees comply with the company’s ethical guidelines.

However, ethical commitment without additional enforcement mechanisms often proves less effective (Yulianti et al., 2023). While fostering a culture of ethics is crucial, it alone is often insufficient to deter unethical behavior in complex organizational environments. According to Jermsittiparsert et al. (2021), the combination of ethical guidelines with Shariah principle enforcement can enhance the attitudes and behaviors of individuals within a company. Shariah encourages ethical teachings that can influence individual behaviors, steering them away from opportunistic practices and enhancing loyalty to stakeholders Amayreh et al. (2024), Santoso et al. (2023) and Al-Shamali et al. (2021) proved that Islamic ethical commitment positively affects the company’s financial performance and reduces corruption. In another perspective, Shariah principles could shape the framework of Islamic finance which serves as an ethical foundation for Islamic-based transactions, guiding the structuring of financial and business dealings in accordance with Islamic teachings. However, Azam et al. (2019) argue that the current Shariah screening processes do not fully conform to underlying Islamic principles, suggesting that Shariah status may not play a crucial role in ensuring ethical behavior among managers. This raises questions about the extent to which Shariah compliance can effectively moderate the relationship between ethical commitment and corruption, particularly in contexts where the implementation of Shariah principles is inconsistent or superficial.

In Malaysia, the Malaysian Code of Corporate Governance (MCCG) was established in 2007 and revised for the fourth version in 2021. This MCCG urged businesses to improve their corporate governance practices to reach a higher standard of ethical behavior, especially for MCCG 2017, which focused on the firm’s transparency and strengthening the corporate governance structure. Ethical business practices were listed as one of the strategies for a firm to expand (Sarkar et al., 2021). According to Nguyen et al. (2020), ethical norms can change and are influenced by society, technology, and religion, influencing how people see corruption. Thus, by enforcing more effective policies and regulations for the company's stakeholders, the ethical practices of businesses could help prevent corporate corruption and crime. Apart of MCCG, Bank Negara Malaysia introduced an “Implementation Guide for Value-based Intermediation” (VBI) (Bank Negara Malaysia, 2018). which aims to strengthen the foundations of Islamic finance in social justice and to advocate for a value-based economy through enhanced integrity, inclusivity, and sustained prosperity. Although VBI adoption is not mandatory for non-financial institutions, aligning the principles into the business could enhance the company’s reputation and contribute positively to fighting corruption by practicing ethical conduct and responsible practices.

In the context of this study, Shariah-compliant companies can indeed play a crucial role in boosting ethical practices and reducing corruption, due to their adherence to specific principles and practices rooted in Islamic ethics. Shariah-compliant companies are businesses that operate in accordance with Islamic law (Shariah), particularly in how they earn revenue, invest, and conduct their operations. Shariah-compliant companies can preserve their Islamic values while promoting ethical standards, encouraging responsible conduct, and contributing to a good impact on society by aligning with VBI principles. According to Busiri (2020) and Huda and Ispriyarso (2019), Islamic Religious Education can be utilized as a technique of preventing and anticipating corruption by establishing anti-corruption standards. The establishment of MCCG and VBI in Malaysia aims to promote responsible practices that highlight the necessity of ethical behavior and integrity within companies which could contribute to combating corruption. Ethical commitment and Islamic practices may reduce the organization’s corruption level (Shah et al., 2023). Additionally, the Shariah principle provides a comprehensive ethical framework that inherently discourages corrupt practices through its emphasis on justice, transparency, and accountability. Shariah compliance mandates that financial transactions adhere to ethical standards that prohibit exploitative practices such as Riba (interest), Gharar (excessive uncertainty), and Maysir (gambling) (Aziz and Ghadas, 2021).

Therefore, there is a need to study Shariah-compliant companies due to their enforcement of the Shariah principle. Shariah-compliant companies are required to follow a formalized set of ethical guidelines rooted in Islamic teachings. There is a substantial necessity for studying Shariah-compliant companies because of their adherence to Shariah principles, which establish a structured ethical framework prioritizing fairness, justice, openness, and responsibility. These corporations utilize procedures such as Shariah advisory boards to guarantee compliance with elevated ethical standards, rendering them exemplary for examining how systematic ethical enforcement might mitigate corruption and unethical conduct. Investigating these companies provides significant insights into corporate governance, the cultivation of ethical corporate cultures, and the influence of Shariah principles on organizational activities. Such research could yield optimal procedures for both Shariah-compliant companies and wider anti-corruption initiatives across several sectors.

Malaysia’s regulatory framework for Islamic principles is robust and well-established. In addition, the growth of the halal industry in Malaysia is accelerating. Therefore, exploring corruption among Shariah and non-Shariah-compliant companies is necessary to develop tailored strategies for mitigating risk. It is critical to investigate how ethical commitments, particularly those influenced by Shariah compliance, can operate as a deterrent to corruption within firms. Addressing these knowledge gaps can support the development of more effective anti-corruption policies, enhance corporate ethical standards, and reinforce adherence to Shariah principles. Moreover, understanding the dynamics between ethical commitment and corruption has broader implications for firm behavior and economic outcomes. Corruption increases operational inefficiencies, distorts market competition, and undermines investor confidence, hindering economic growth and institutional trust.

Conversely, ethical commitment can improve governance, reduce agency costs, and promote sustainable business practices. Framing the issue through this economic lens allows for a deeper understanding of how ethical behavior contributes to both firm-level performance and wider economic stability. Therefore, this study examines the relationship between ethical commitment and corruption, with a particular focus on the moderating role of Shariah compliance. By integrating both ethical and economic perspectives, the study aims to contribute to policy development and support more effective regulatory practices that align with Islamic principles while promoting economic integrity.

This study will be structured as follows. The next section reviews related literature. Then, section III describes the data and research methodology employed in this study. The analysis and discussion of results will be described in section IV. The conclusion and recommendations based on the research findings are included in the final section.

II. Literature Review

Ethical commitment refers to a commitment to adhere to moral guidelines and standards in one's conduct, decisions, and attitude. In the context of professional obligations, ethical concerns can guide individuals to act in an honest, fair, and courteous manner toward others (Hemphill, 2023; Ryan, 2005). The study of ethics has been extensive because it is crucial to regulate human behavior. It has been linked to corporate governance for a long time since corporate governance is a way to guide and control how people make decisions in a company. Nevertheless, poor corporate governance could lead to the violation of the code of ethics and committed fraud in corporations. Organizations that went out of business due to unethical behavior cost billions of ringgits to their owners, shareholders, workers, and other stakeholders. Accordingly, it is claimed that this would not have happened if upper management and staff were aware of their coworkers’ unethical behavior (Alias et al., 2019). This could lead to corruption, which would tarnish the businesses’ reputations.

The term “corruption” refers to dishonest or unethical conduct, which frequently involves the abuse of authority or position for one’s benefit or to obtain an unfair advantage such as bribery, fraud, embezzlement, and abuse of power (Acheampong et al., 2024). Organizations with strong ethical commitment will actively fight corruption. Trust, justice, and moral behavior are fostered in societies and organizations by ethical commitment, which lays the groundwork for cultivating conditions that prevent corruption. Therefore, Shariah-compliant companies are seen to have a more ethical commitment toward their organization. Shariah compliance refers to the adherence to principles and guidelines outlined in Islamic law. Shariah boards will oversee Shariah compliance by providing assistance and ensuring that corporate practices align with Islamic standards. According to Kamaruding et al. (2022), Tawheed, kindness, and sincerity, had a good effect on the people involved in business. Thus, having an excellent ethical commitment in addition to Shariah compliance is seen to reduce corruption in business. Based on the preceding ideas and arguments, this study emphasizes the relevance of ethical commitment and Shariah compliance in constructing a fraud-resistant organization and corruption in Malaysia. Furthermore, the study contributes to the current scenario of ethical commitment, Shariah compliance in Malaysia’s companies, and the challenges that companies wanting to embrace morals endure.

1. Agency Theory

Jensen and Meckling (1976) proposed agency theory to investigate a corporation’s problems. The principal-agent problem is explained by agency theory, in which managers, as agents, engage in opportunistic behavior to maximize profits. As ownership in companies becomes increasingly diffused among shareholders, rather than operating on behalf of the owners, managers tend to pursue their own interests and achieve greater influence (La Porta et al., 2000). According to agency theory, a manager’s principal task is to maximize shareholder wealth. In maximizing wealth, it is essential to avoid incidents that contribute to corruption, which may negatively impact the company’s performance. To prevent managers from engaging in opportunistic behavior, agency theory suggests implementing effective monitoring procedures that reduce agency costs and align the interests of shareholders and managers (Benjamin et al., 2016).

Therefore, agency theory can be related to ethical commitment and corruption of the company in terms of the role of the manager to enforce employees to obey the company’s policy and guidelines as well as commit ethical behavior to reduce the corruption cases in the company. According to Dokas (2023) and Sarhan and Gerged (2023), the board’s role is vital in safeguarding the company’s credibility. For instance, the extent of corruption may represent the effectiveness of a nation’s political and legal system, which can influence board members' conduct and their ability to address corporate agency problems. Thus, policy enforcement, such as an anti-corruption policy, can ensure that all business entities adhere to ethical standards (Barkemeyer et al., 2018) and that violators face consequences for their actions. Additionally, Rosli et al. (2015) and Said et al. (2016) revealed that integrity is a key part of a sound governance system. The integrity system comprises policies, actors, and practices that can help maintain the integrity of an organization. These include mechanisms based on compliance, ideals, and informal everyday practices that help the organization achieve its goals (Molina, 2018). Therefore, agency theory suggests that enhancing corporate governance by establishing ethics-related rules is an effective means of promoting excellent ethical practices in organizations, thereby preventing future corruption (Cuomo et al., 2016).

In the context of this study, agency theory demonstrates how Shariah principles reduce conflicts by combining the interests of both principals and agents with ethical standards grounded in justice, fairness, and transparency. By implementing Shariah compliance, these companies establish a framework that holds managers accountable to shareholders and the broader community, ensuring that business decisions are made with integrity and in the best interest of all stakeholders. The enforcement of Shariah principles also reduces the risk of unethical behavior, including corruption, as it requires transparency and accountability in decision-making, which can help reduce the agency problem and foster trust between principals and agents.

2. Ethical Commitment, Shariah-Compliance and Corruption

Ethical commitment is a crucial agenda item for every organization. In examining the intricate relationship between Shariah compliance and voluntary ethical practices within firms, it is essential to consider several potential dynamics that may influence the observed outcomes (Cheong, 2020). One such dynamic is the concept of diminishing returns, which suggests that in firms already operating under strong ethical mandates via Shariah compliance, the marginal benefit of additional voluntary ethical commitments may be limited (Halim et al., 2017). This implies that the incremental value derived from implementing further ethical initiatives may decrease as the firm approaches a saturation point in its ethical performance (Qaderi et al., 2024). Firms operating under Shariah principles may already exhibit a high level of ethical conduct due to the comprehensive nature of Islamic law, which governs various aspects of business operations, including financial transactions, labor practices, and environmental stewardship (De Bruin et al., 2020). Consequently, the adoption of additional voluntary ethical practices may yield progressively smaller improvements in ethical performance, as the firm is already operating at a relatively high ethical standard (Qaderi et al., 2024).

In this study, ethical commitment refers to the knowledge of ethics that can be utilized to shift employees’ focus to ethical standards (Ferdiansah et al., 2023). According to Ngcamu and Mantzaris (2023), the lack of policy enforcement would lead to an increase in corruption cases. Thus, ethical commitment refers to the company’s commitment to having a standard and policy in place to serve as guidance for employees. A firm’s commitment to establishing an ethical culture can be gauged by examining the top management’s rules and the company’s principles (Driskill et al., 2019; Vasconcelos, 2023; Janenova and Knox, 2020). According to Cotton et al. (2017), ethical managers who convey an ethics and values message and serve as a visible role model of ethical behavior hold their followers accountable for ethical behavior. Additionally, Zahari et al. (2022) found that the practice of ethical cultures, such as supportability and sanctionability, has a positive impact on reducing corruption within an organization. By supporting and effectively communicating ethical standards, ethical leadership should play a vital role in the fight against corruption (Bashir and Hassan, 2020). With an ethical leader, people make less deliberate decisions and instinctively reject unlawful conduct like corruption (Manara et al., 2020; Hechanova and Manaois, 2020).

In Malaysia, enforcing ethical practices is strengthened by establishing the Malaysian Code of Corporate Governance (MCCG). MCCG urged businesses to operate at the highest possible ethical level by bolstering their corporate governance standards. Companies can improve their oversight by incorporating ethical practices like training and whistle-blowing policy into their governance (Merchant and White, 2017). The corporate governance code underlined the concepts of integrity, compliance, ethics concept, and anti-corruption policy. According to Mohan (2022), Malaysia’s corruption score decreased from 2019 to 2021, as reported by Transparency International. The decreased score represents high corruption in companies. Unethical practices such as corporate crime and scandals will lead to a worse impact on the company. Various misconducts and violations of the firm’s rules contributing to weak corporate governance have resulted in significant financial losses for corporations (Setiawan et al., 2020; Johari et al., 2022). Additionally, some studies found that corruption damages the quality of public institutions (Yunan, 2020; Chan et al., 2020; Bauhr and Charron, 2020) and reduces productivity and economic growth (Schomaker, 2020; Akimova et al., 2020). However, if the corporation employs an effective anti-corruption strategy in each alternative, the level of corruption will be lower than previously (Meyer-Sahling and Mikkelsen, 2022; Steenberg, 2021). Thus, having an excellent anti-corruption policy will lead to a better ethical commitment that could combat corruption in the company.

Ethical commitment is closely related to Shariah compliance. According to Masud et al. (2024) and Lai (2022), Islamic finance, through its adherence to Shariah principles, can contribute to reducing corruption within financial systems and businesses. In addition, Shariah-compliant companies frequently have strict governance structures that are overseen by Shariah boards or advisors. Modern economy has proved that Shariah compliance is one of the tools to reduce the level of corruption within an organization. Masud et al. (2024) reported that Shariah-compliant companies got fewer corruption reports than non-Shariah-compliant companies. This is because the board of directors, especially SSBs plays an important role in reducing the level of corruption in companies (Hussain Khan et al., 2022). The findings underscore the importance of enforcement and regulatory mechanisms, while also confirming the positive impact that SSBs have had in mitigating the negative effects of corruption. In addition, according to Busiri (2020), Islamic Religious Education can be utilized as a technique of preventing and anticipating corruption by instilling anti-corruption standards. Corruption could reduce the profitability and performance of companies whether it is Shariah or non-Shariah companies. There are mixed findings from previous studies in terms of the company’s performance.

Based on the study by Hussain Khan et al. (2022), Islamic banks are less corrupt than conventional banks. It shows that, as an integral component of Islamic banking and a multi-layer corporate governance structure, the Shariah Supervisory Board (SSB) is anticipated to mitigate the impact of corruption. The results emphasize the need for enforcement and regulatory procedures while confirming the good role that SSBs have played in reducing the detrimental effects of corruption. By monitoring business decisions and transactions, these entities ensure Shariah compliance, reducing the likelihood of corrupt practices. The study by Kamaruding et al. (2022) proved that Shariah compliance, emphasizing a positive purpose, provides the potential to address organizational corruption issues. Additionally, religious experts are encouraged to educate the people about the negative impacts of corruption to deter involvement (Zulyadi et al., 2022). Furthermore, Shariah compliance and corporate sustainability initiatives constitute an investment when they are acknowledged by all stakeholders and earn an excellent image (Khattak et al., 2020). Thus, companies that improve their employees’ attitudes and actions should consider Islamic work ethics, as well as Shariah compliance, which enhances the firm’s credibility. This involves conducting operations in accordance with Islamic principles that impose strict rules and moral requirements.

However, several studies exposed that Shariah-compliant companies underperformed compared to non-Shariah-compliant companies due to investors must forego certain profits to meet their Islamic principles (Nainggolan et al., 2011; Farooq and Alahkam, 2016) but the study by Martani, et al. (2009) found that Shariah-compliant companies outperformed their peers due to their close adherence to Shariah laws, which helps them achieve greater performance by attracting investors who want to participate in companies that follow Shariah principles. This is also supported by Aziz (2020) where the Islamic teachings as well as the spiritual values of Islam could prevent corruption. It demonstrates that individuals can contribute to the development of ethical conduct by adhering to Islamic teachings and promoting principles that prohibit corrupt behavior. Islamic law imposes strict penalties for offenders who commit fraud or bribery, which can lead to corruption (Zulyadi et al., 2022). In other words, Islamic law punishes corrupt people harshly to protect society.

Therefore, it can be expected that Shariah-compliant companies that enforce Islamic ethics and law could reduce the corruption level. When ethical commitment is combined with Shariah principles, individuals and businesses can operate with honesty and morality within the context of Islamic teachings, aligning with broader ethical norms. This combination of the universal scope of ethical commitment and specific guidelines in the Islamic context could create the best duo to combat corruption. Thus, the hypothesis of this study is as follows:

H1: High ethical commitment contributes to lesser corruption.

H2: Shariah compliance strengthens (weakens) the relationship between ethical commitment and corruption score.

III. Methodology

1. Data and Sample

This paper examined 10660 Malaysian companies from 2012 to 2021. After excluding companies from the financial sector, the sample was reduced to 10,080. The year 2012 was chosen as a key milestone, as the third Malaysia Code of Corporate Governance was introduced. As our data has many missing values, only 453 firm-year observations were available for the regression model. Therefore, with such a small sample, we also applied two stages of the Heckman sample selection estimation method by following Cieślik and Goczek (2022). All data was gathered from Thomson Reuters DataStream.

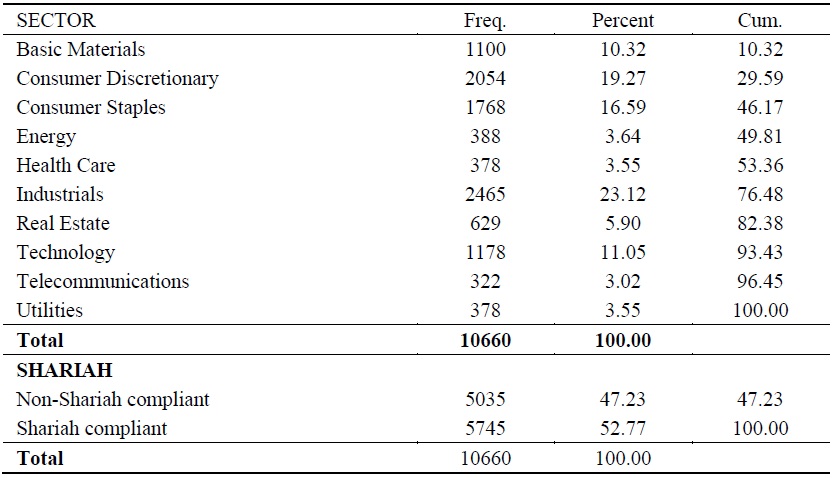

The following Table 1 presents the tabulation of the industry sector for all companies in the sample. Companies from the Industrial sector are the highest, with 23.12 percent. Meanwhile, companies in the Telecommunications sector are the lowest, with only 3.02 percent of the total sample.

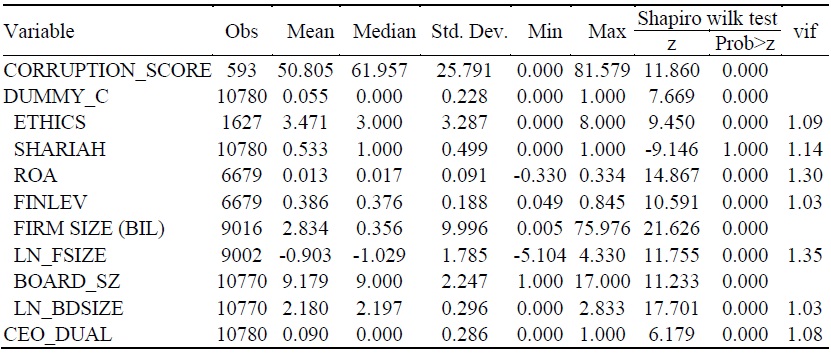

The following Table 2 presents the descriptive statistics of all variables. The mean (median) value of CORRUPTION_SCORE is 50.805 (61.957). The value reflects the current situation for the Malaysian Corruption Perception Index, with a score of 50 in 2023 (Transparency International Malaysia, 2023). The mean value for ETHICS is 3.471. The mean value of ETHICS indicated that, on average, Malaysian companies only have at least 3 of 8 indicators related to ethical commitments. Regarding controlling variables, average companies have a ROA of 0.013 percent. The mean (median) value for FINLEV is 0.386 percent (0.376 percent). The mean (median) value for LN_SIZE is -0.903 (-1.029) or RM 2.834 billion (0.356 billion). The average number of board directors (LN_BDSIZE) is 2.180 or 9.179.

2. Method

Panel data is defined as the grouping of observation of data including companies, countries and individuals over a period of time (Ascarya and Indra, 2022). Panel data analysis involved three models, which are pooled ordinary least square (OLS), fixed effect model (FE), and random effect model (RE). The equation for OLS models as follow:

Where, ‘Y’ refers to dependent variable of the model; Variable ‘X’ is the independent variable, β is beta coefficients, ‘ε’ is the error terms, and econometric units in subscripted letter, ‘i’ and ‘t’, are both representing the group’s identifier and time. Meanwhile, both fixed and random effect models allow for the heterogeneity of error terms. The assumption of random effect is that λ (time-invariant factor) has no correlation with both dependent and independent variables (Frees, 2004). Fixed effect model however assumes λi as constant (Torres-Reyna, 2007). The error terms are a group of the two independent components; ‘λ’ and ‘u’:

Therefore, the first equation becomes as follow:

The Breusch-Pagan Lagrangian multiplier (BPLM) test identifies the differences of OLS and RE model from individual specific-term (λ) which are treated differently in these two models. The test hypothesized (Ha) that there is a variance (σ2) across entities or heterogeneity (Torres-Reyna, 2007). RE model should be selected if p-value reject null hypothesis (p < .05) (Law, 2018).

Hausman (1978) suggested testing the comparison of correlations between parameters in both RE and FE models. Hausman test hypothesize (Ha) that there are correlations between errors (λi) and regressors (Torres-Reyna, 2007). Hausman test denoting the matrix of variance (

If Hausman test rejects null, (p < .05), FE model estimator should be used. For this study, the RE model was selected as a p-value of the Hausman test is larger than 5 percent as shown in Table 3.

In order to control the issues of heteroscedasticity, autocorrelations, and cross-sectional dependence, we apply Driscroll-Kraay’s robust standard error estimation method (Hoechle, 2007). This approach is a nonparametric covariance estimator that produces consistent heteroskedastic and autocorrelation standard errors that are robust which is similar to the Newey and West (1986). Adjusting the estimated standard error in this way guarantees that the estimator of the covariance matrix is consistent, independently of the cross-sectional dimension N (ie also for N → ∞). Thus, Driscoll and Kraay’s approach eliminates the shortcoming of other large T covariance matrix estimators that typically become inappropriate when the cross-sectional dimension N of the micro econometric panel becomes large.

In order to reduce sample selection bias, we proceed with Heckman sample selection estimation method. The OLS might be based on samples non-randomly selected which led to the bias. Heckman provides corrections for such error (Heckman, 1976) by using two-stage estimation method which involves in two steps, where the first step is to estimate the selection equation using a probit model.

Where Y1* is a dependent variable, X1 is a vector of independent variables, β1 is a vector of parameters, and Φ is the cumulative distribution function of the standard normal distribution. In the second step, the inverse Mills Ratio was included in the second equation as an additional variable.

Where Y2 is the outcome variable, X2 is a vector of independent variables, β2 is a vector of parameters, λ is the IMR, σ2 is the standard deviation of the error term in the outcome equation, and ε2 is the error term. This two-step process allows us to correct for sample selection bias and obtain unbiased estimates of the parameters in the outcome equation.

3. Model Development

We applied panel data analysis to examine the relationship between ethical commitment (

The definitions and calculations of

Regarding controlling variables (

IV. Results and Analysis

1. Results

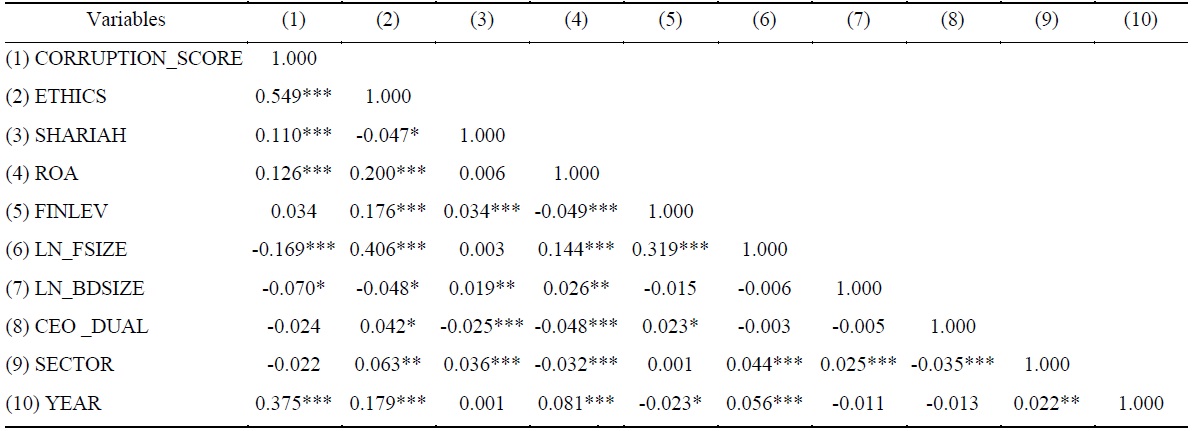

Table 4 presents the pairwise correlation for all variables. CORRUPTION_SCORE has a positive correlation with ETHICS, SHARIAH, ROA and YEAR while having a negative correlation with LN_FSIZE and LN_BDSIZE. The positive correlation between CORRUPTION_SCORE and ETHICS indicates that companies that pursue ethical conduct in operations would have better scores in the corruption index. Similarly, shariah compliance companies are also expected to have better corruption scores due to the strict Shariah rules that promote good and moral practices. ETHICS have a positive correlation with ROA, FINLEV, LNFSIZE, CEO_DUAL, SECTOR, and YEAR. SHARIAH has a positive correlation with FINLEV, LN_BDSIZE, and SECTOR.

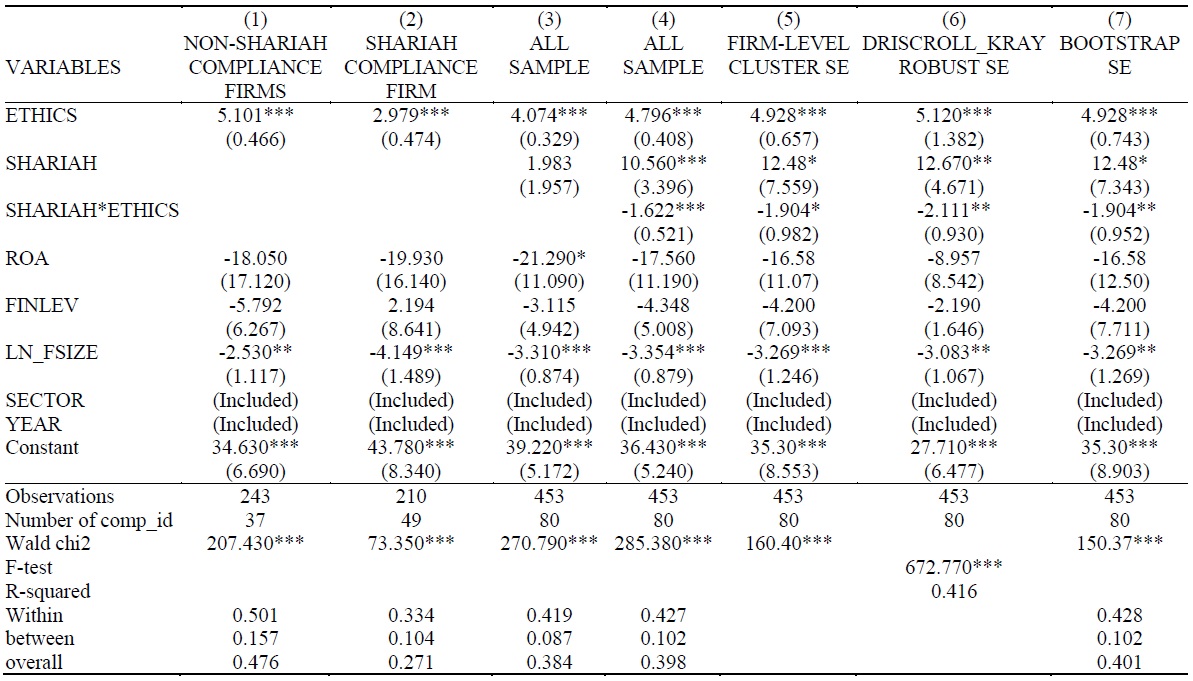

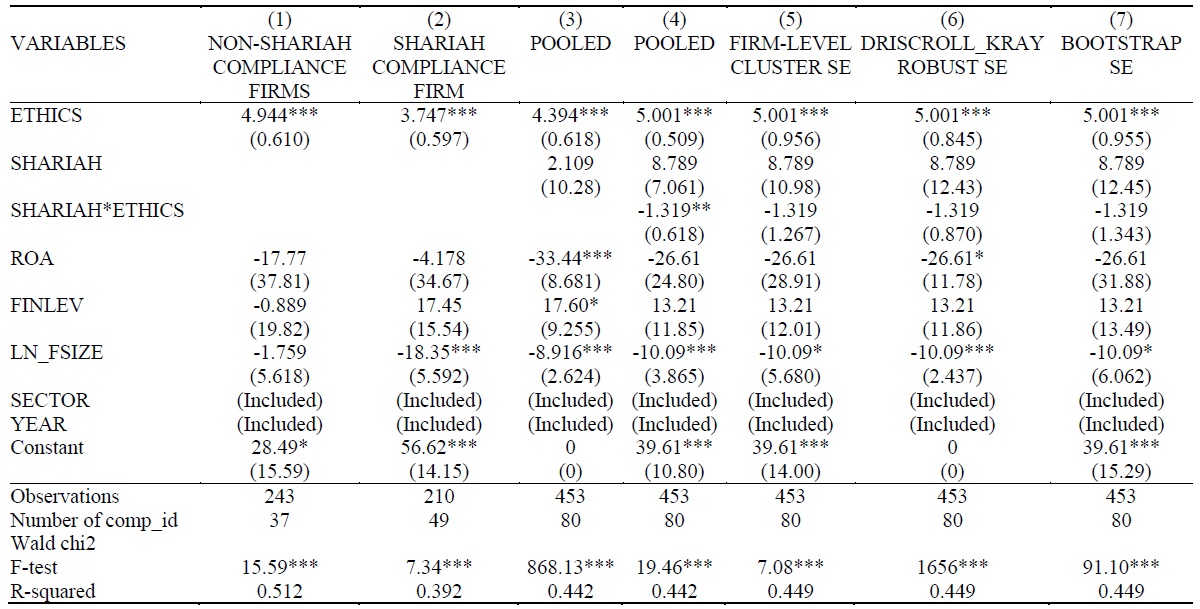

Table 5 presents a random effect estimation between ETHICS, SHARIAH, and CORRUPTION_SCORE. The first column (1) shows the estimations result for non-shariah compliant companies, where ETHICS have a positive association with CORRUPTION_SCORE at 1 percent significant level (p<.01). Similarly, in the second column (2), ETHICS have a positive association with CORRUPTION_SCORE at a 1 percent significant level (p<.01). In the all sample, both column (3) and (4) shows ETHICS have positive association with CORRUPTION_SCORE at 1 percent significant level (p <.01). Meanwhile, SHARIAH have no association with CORRUPTION_SCORE in column (3) and positive association with CORRUPTION_SCORE in column (4). Nevertheless, column (4) shows that SHARIAH weakened the association between ETHICS and CORRUPTION_SCORE at a 1 percent significant level (p<.01).

To control the unobserved heteroscedasticity and autocorrelation, we applied another estimation model by clustering firm-level standard errors (column 5) and Driscroll-Kraay standard errors estimation (column 6). The result was similar to column (4) as ETHICS has a positive association with CORRUPTION_SCORE, SHARIAH has a positive association with CORRUPTION_SCORE and the interaction between SHARIAH and ETHICS, (SHARIAH*ETHICS) weakened the association. Due to small sample size, we replicate the random effect estimations by using bootstrap standard errors method, which can improve the estimations accuracy. We follow Song et al. (2024) by applying bootstrapping standard errors method with 1000 replications. The result presented in column (6) Table 5 shows consistency and more improve coefficient for ETHICS compared to pooled result (column 4).

In addition, we also present the fixed effect model to capture the unobserved time-variant effect for SHARIAH compliance variable in table 6. The fixed effect model shows consistent results regarding ETHICS on CORRUPTION_SCORE. However, SHARIAH compliance has no effects on CORRUPTION_SCORE. The interaction term (SHARIAH*ETHICS) also has no effect on CORRUPTION_SCORE especially in robust standard error models (column 5 and 6).

2. Additional Analysis

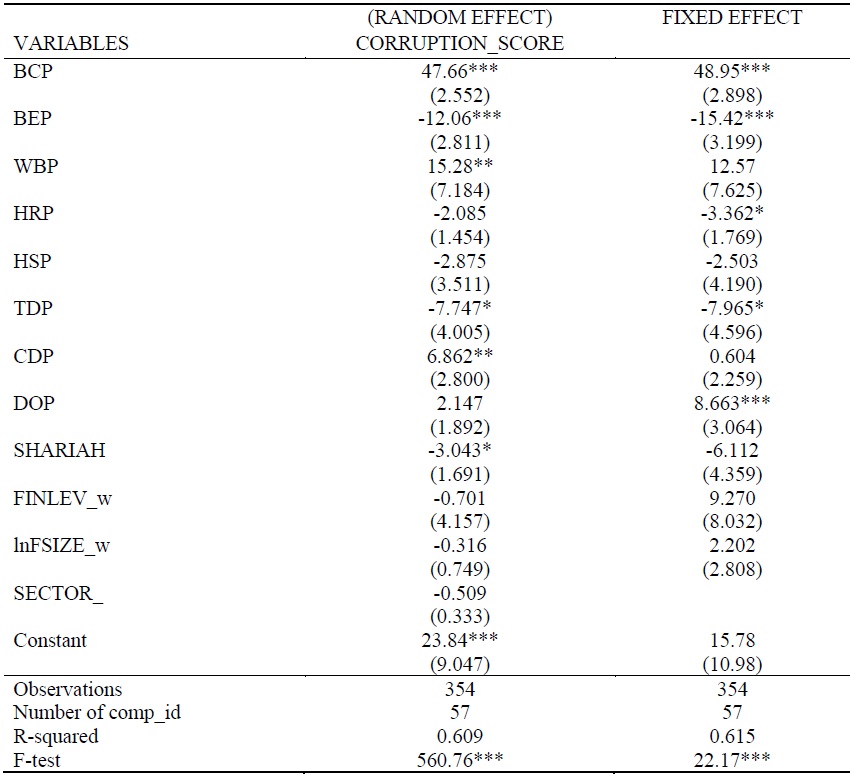

We further extend the analysis by including dummy variables for each ethical commitment variables. The reason to do such estimations is to capture which ethical practices’ indicators that are associated with corruption in companies. The results (Table 7) show that Policy on Bribery and Corruption (BCP), Whistleblower Protection (WBP) and Policy on Career Development (CDP) have positive association with CORRUPTION_SCORE, which implied that companies with such policy implemented, have better corruption scores (less involvement in corruption related controversies). However, Policy on Business Ethics (BEP), and Training and Development Policy (TDP) have negative association with CORRUPTION_SCORE, which indicates that by having such policies, unable to combat corruption behaviors and possible lead to the involvement in corruptions controversies. Meanwhile for the rest indicators, Policy on Human Rights (HRP), Policy on Employee Health and Safety (HSP) and Policy on diversity and opportunity (DOP) have no association with CORRUPTION_SCORE.

These results indicate that having policy regarding bribery and corruption is effective to prevent any involvement in corruption related controversies. This also reflects the commitment from top management to lower-level employees to avoid any corruption related activities. Regarding the result of having whistleblowing policy and policy for career and development, that able to lower corruption score, can be explained based on the recommendations of MCCG. Therefore, a possible reason for such results is that companies show commitment to adhere to the recommendations of MCCG to prevent corrupt practice in operations.

In term of SHARIAH compliance however lower CORRUPTION SCORE. This shows that the presence of SHARIAH compliance might be unable to avoid companies from involvement in corruption related controversies therefore lead to lowering corruption score. Another possible reason is shariah compliance companies obligated to provide product and services that comply with shariah principle therefore it is possible that less-ethical companies were included in shariah compliance listed firms (Malik et al., 2025).

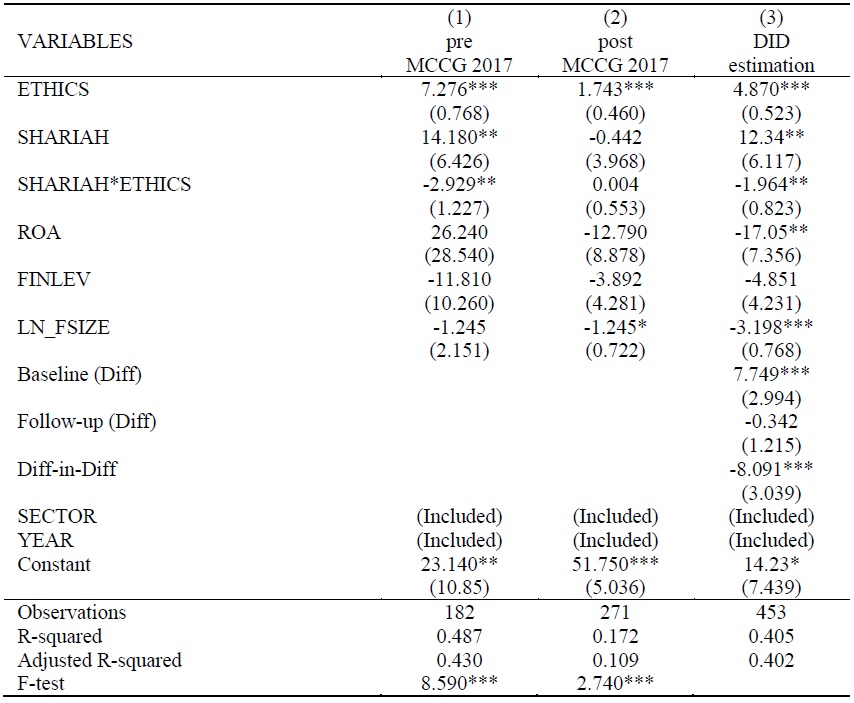

We further the analyses by separating the pre-MCCG 2017 (2012-2016) and post-MCCG 2017 (2017-2021) samples in Table 8. We chose the pre-MCCG 2017 period as companies fully complied with the previous MCCG 2012 (Zainul Abidin et al., 2022). In addition, post-MCCG 2017 expects companies to be more integrity and transparent in business dealings and promote good ethical business practices from top management to bottom.

The first column (pre-MCCG 2017) shows that ETHICS has a positive association with CORRUPTION_SCORE at a 1 percent significant level (p < .01). This shows companies already adhered to ethical commitment before the introduction of MCCG 2017. Moreover, this result shows that companies are highly committed to practicing ethical business as recommended by MCCG 2012 (Zainul Abidin et al., 2017) therefore, companies become cleaner from corruption and help increase their corruption score. Similarly, the second column (post MCCG 2017) also shows a positive association between ETHICS and CORRUPTION_SCORE. This also explains that MCCG 2017 recommends that companies establish a code of conduct and ethics and expects them to maintain their integrity and create ethical behavior among management, employees, and stakeholders (Securities Commission, 2017).

Regarding Shariah-compliant companies, during pre-MCCG 2017, the result shows that SHARIAH has a positive association toward CORRUPTION_SCORE at 5 percent level (p < .05). On the contrary, during post-MCCG 2017, SHARIAH have no association with CORRUPTION_SCORE. The result of post-MCCG 2017 shows the regulations and recommendations of MCCG for practicing ethical business outperforming Sharia-compliant standards. This is because all listed companies including Shariah or non-shariah compliant were recommended to comply with the MCCG recommendations to practice ethical business. Moreover, as MCCG2017 emphasizes strengthening governance structure and establishing a code of conduct and ethics, such recommendations might help Shariah-compliant companies improve their governance and practices and therefore help improve their corruption score. Nevertheless, the interaction term SHARIAH*ETHICS weakens the association between ETHICS and CORRUPTION_SCORE during pre-MCCG 2017 and has no association with CORRUPTION_SCORE during post-MCCG 2017. One reason shariah compliance might weaken the link between ethics and corruption is that shariah companies follow the Islamic Capital Market guidelines set by the Securities Commission. However, these guidelines mainly focus on ensuring transactions comply within shariah law rather than explicitly addressing anti-corruption measures such have code of ethics to combat corruption as recommended by MCCG 2017.

In addition, we employed difference-in-difference estimations to examine the differences between pre MCCG 2017 and post MCCG 2017. we firstly identify large companies with market capital more than RM2 billion as defined by MCCG (2017), large companies are recommended to have majority independent directors on board, at least 30 percent women on board and board tenure should not more than 9 years. Later we composite this three governance variables as treatment for companies that possibly adhere to MCCG recommendations. The results presented in column (3) Table 8 shows the consistency of association for ETHICS on CORRUPTION_SCORE, positive association between SHARIAH and CORRUPTION_SCORE, and negative association for interaction of SHARIAH*ETHICS on CORRUPTION_SCORE. The result for baseline (Diff) shows positive significantly indicate that during pre MCCG 2017, companies with strong governance characteristics have positive association with corruption (less involvement in corruption related controversies). As follow-up (Diff) result shows negative significant, it is implied that there is slight decrease of CORRUPTION_ _SCORE, which also implied companies might be involved in controversies but not statistically strong evidence. Nevertheless, the Diff-in-Diff result shows negative significant which implied that companies subject to MCCG experienced a decrease of CORRUPTION_SCORE which implying the latest MCCG had unintended effects on companies’ corruption related controversies. Such results also can be several implications of the latest MCCG on companies as they face stronger governance and regulatory pressure which lead to more transparency in reporting and reported issues that causing the corruption scores to decline.

3. Robustness Test

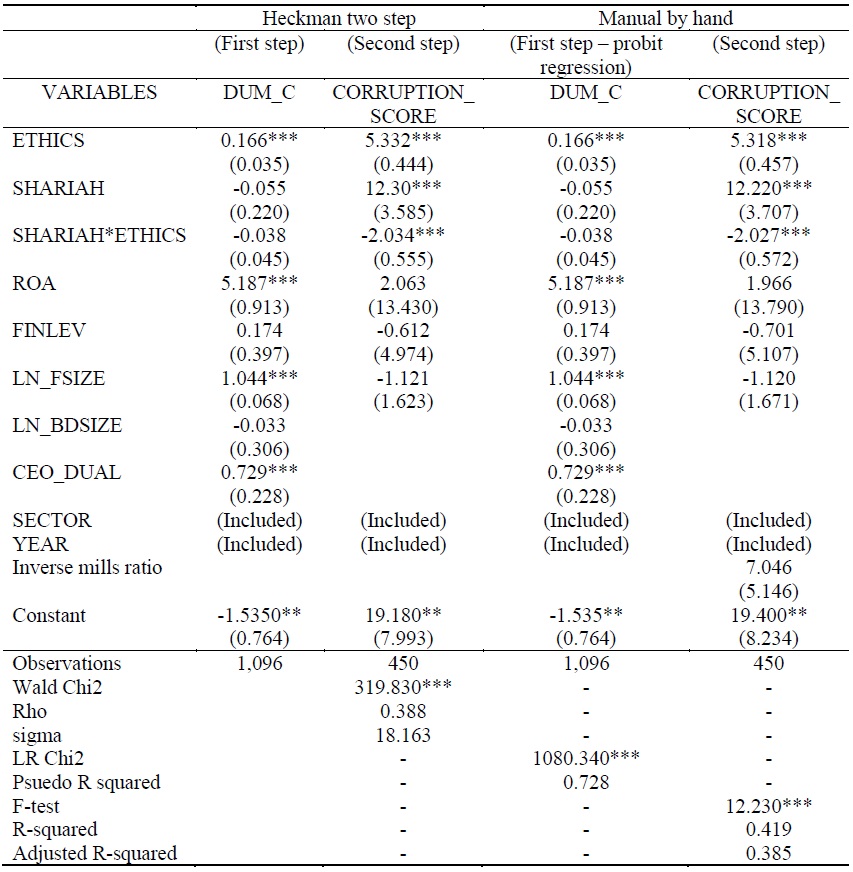

The main result from Table 8 may be biased due to small sample bias and endogeneity problems, where companies with lower levels of corruption are likely to be more committed to ethics. Thus, companies with highly committed ethical practices will likely be self-selected in the sample. We apply the Heckman selection model to obtain unbiased estimates in the presence of missing data (Heckman, 1976). We selected board size (LN_BDSIZE) and CEO duality (CEO_DUAL) as the instrument variables, following Al-Shaer (2023). The number of directors on the board is significant to a firm’s decision-making. Thus, it is able to influence a firm’s ethical practices (Boutchkova et al., 2022). Meanwhile, CEO duality plays a role in a firm’s transparency regarding corruption information (Jaggi et al., 2021).

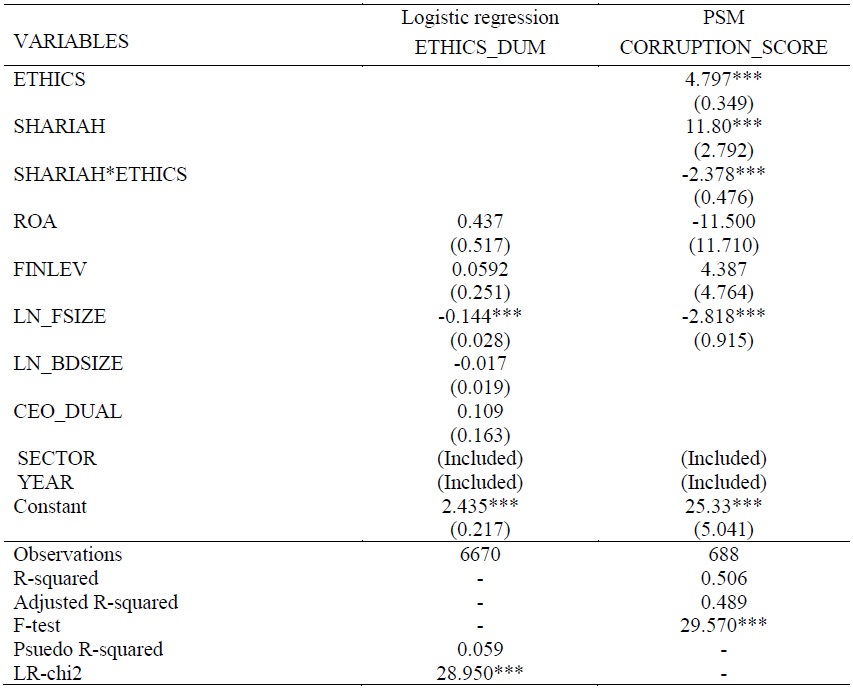

The following Table 9 presents the two-stage Heckman sample selection regression approaches. In the first stage, we create dummy variables of corruption (DUM_C) and regress them alongside control variables, including board size and CEO duality. DUM_C was calculated from the mean value of CORRUPTION_SCORE, which was assigned to 1 if the mean was above (3.47) and 0 if the mean was below. The residuals of the first step were included in the second step regression. The result of the selected sample was presented in column 2, which is similar to the main model. The inverse-mills ratio shows insignificant values (p < 0.05) which implies selection bias not a serious issue (Duong et al., 2022). We also compared the results with the manual-by-hand method and showed consistency in the findings.

Following Table 10, we follow Mohamad Ariff et al., (2023) by applying the Propensity Score Matching (PSM) approach. PSM techniques are considered as it used a matched score of a model with interfering variables and treated the model by matching the closest propensity score (Rosenbaum and Rubin 1983), we applied PSM estimation regression result where in the first stage (column 1), we ran the logistic regression of ETHICS on controlling variables, including LN_BDSIZE and CEO_DUAL as interfering variables. The treated weightage of the logistics model was included in the OLS model in the second stage (column 2) and provided similar findings to the main findings in Table 5.

4. Endogeneity Concerns

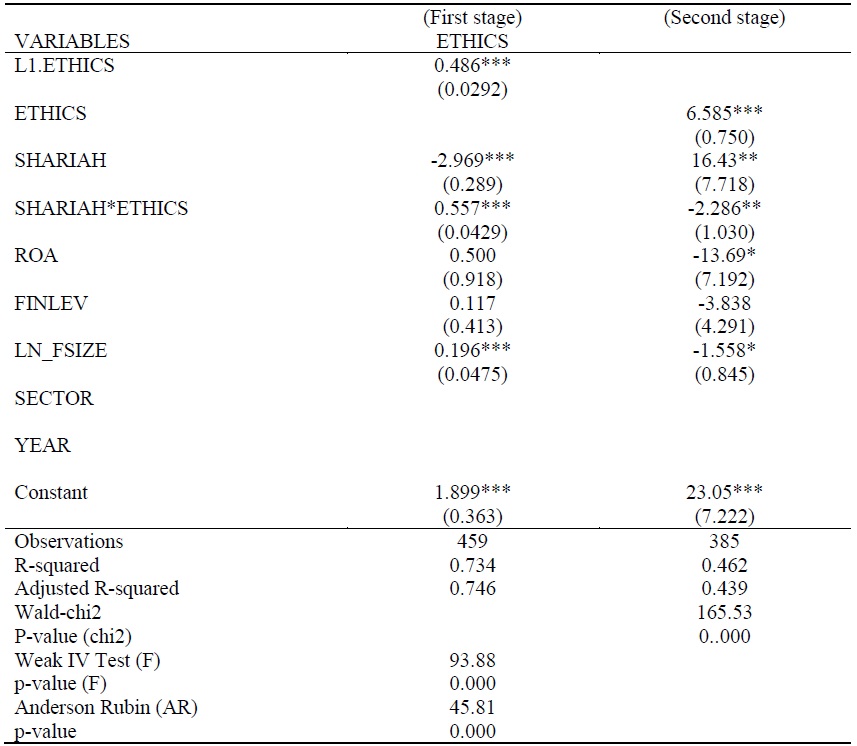

To account for potential endogeneity concerns, we introduce an instrumental variable (IV) approach (Table 11). However, using IV approach for 2SLS have limitations to find a valid instrument (Ullah et al., 2021) and become challenges for many researchers. Therefore, we chose lag 1 year for independent variable as our instruments (L1.ETHICS). Using lagged independent variables can help mitigate endogeneity because they reflect past values that are unlikely to be influenced by current outcomes, thereby reducing issues such as reverse causality and omitted variable bias (Arif et al., 2021). The rationale for selecting a one-year lag for ethics is that ethical commitment from the prior year could impact current corruption levels while being less susceptible to immediate external disturbances, making it a potentially strong instrument. We employ a Two-Stage Least Squares (2SLS) estimation to validate the instrument’s relevance and assess its impact on our primary findings. Robustness checks confirm that the IV satisfies the necessary exclusion restrictions and improves the reliability of our causal interpretations, as the F-value was 93.88, and our Anderson-Rubin test (AR) suggests the chosen instruments are valid for the model (Andrews et al., 2019). The findings show that there is evidence that strong ethical commitment led to better corruption scores, which means lesser engagement in any corruption business dealings by firms. The coefficient for ETHICS is also higher from previous analysis which indicates firms’ ethical commitment becomes stronger.

5. Analysis

The result regarding ETHICS and CORRUPTION_SCORE affirms hypothesis 1, where companies with high ethical commitment contribute to lesser corruption. Aligned with agency theory, ethical practices help mitigate agency problems in companies’ management (Giannarakis et al., 2020). Ethical policy can be one of the tools for monitoring and preventing corruption (Merchant and White, 2017). A strong ethical code and policy will help prevent management and employees from being involved in unethical behaviors. Companies that are highly committed to ethical practices not only receive a good perception from stakeholders, but they also help to improve the firm’s reputation, therefore, helping to increase values in the marketplace. Monitoring tools in terms of policy enforcement imply that companies that are committed to ethical conduct by establishing policies show legitimacy for their practices. For example, imposing an ethics policy will ably restrain management and employees from being involved in corruption (Merchant and White, 2017). If there are policy breaches, companies or authorities have the right to take any disciplinary action against employees or managers involved in unethical practices (Schwartz, 2013).

This finding regarding SHARIAH implied that companies practicing Shariah compliance in their business do contribute lesser corruption, which is aligned with the study by Shah et al. (2023). The reason behind such findings implied that Shariah companies operate based on the Quran and Sunnah that emphasize specific Islamic ethical conduct (Miglietta and Forte, 2011). However, regarding the second hypothesis, the interaction between SHARIAH and ETHICS (SHARIAH*ETHICS), shows that companies with ethical practices and Shariah compliance reduce corruption scores compared to companies without Shariah companies’ contrary to Shah et al. (2023), therefore rejecting H2. These findings imply that the Shariah compliance factor encounters corruption challenges only in limited contexts or regions. With the newly rising halal companies that embedded Shariah guidelines, inadequate comprehension or improper implementation of Shariah principles may result in circumstances where people can manipulate the system, which can lead to unethical behavior. Therefore, their practices might not be strong enough to lower the level of corruption. Additionally, there is limited control over halal industry in Malaysia, as reported by Ariffin et al. (2021). Thus, it shows that Shariah compliance companies with poor enforcement of ethical conduct could also contribute to high corruption.

Over the period of pre- and post-MCCG 2017, the result shows that there are no differences in the relationship between ethics and corruption. However, Shariah compliance companies were found to improve corruption scores during the post-MCCG 2017 period. This suggests that enhancing the corporate governance structure may reduce corruption in Shariah-compliant companies. Nevertheless, regarding the interaction with ethical commitment, Shariah-compliance companies still experienced higher levels of corruption than non-Shariah-compliance companies during the post-MCCG 2017 period.

Shariah-compliant companies may have different ethical business practices than non-Shariah-compliant companies. As Shariah compliance companies must adhere to Shariah compliance principles and criteria regarding business transactions, halal production, and services, these criteria cannot be included in the corruption score index. Another possible explanation regarding shariah compliance that weakened the association between ETHICS and CORRUPTION is that shariah compliance companies are adhered to follow the Islamic Capital Market guidelines by Securities Commissions. The guideline however does not explicitly state about anti-corruption measures, and it focuses on the obligations for companies to follow shariah law in transactions of their product and services (Securities Commission Malaysia, 2024). Moreover, the guideline provides a methodology for evaluating a company’s adherence to Shariah principles solely through its financial statements using Shariah screening methodologies (Malik et al., 2025). However, the absence of a specific criterion such as responsible investments, in Shariah-compliant industries creates a risk where unethical companies may still be included in portfolios labeled as Shariah-compliant (Malik et al., 2025). Without this additional screening measure, businesses that do not fully adhere to ethical or Shariah principles could become part of these portfolios, potentially undermining their credibility and defeating the purpose of ethical investing.

V. Conclusion and Recommendation

The objective of this study is to examine the relationship between ethical commitment and corruption as well as investigate the role of Shariah compliance as a moderator between ethical commitment and corruption. The findings suggest that companies must embrace their ethical practices to combat misconduct and show their commitment to upholding the highest standard of practices in the marketplace in compliance with MCCG 2017. This study concludes that Malaysian companies are progressive in adopting supplementary programs to promote ethical practices. The agency theory posits that when companies commit to ethical practices by imposing ethical policy (i.e., a code of ethics), it will shape the culture against corruption, thus improving their image and reputation. In addition, Malaysian companies should take this opportunity to be more ethical in business dealings as the market does take note and rewards ethical companies.

However, Shariah compliance does not moderate the relationship between ethics and corruption. It shows that Shariah-compliant companies also encounter corruption challenges such as inadequate comprehension or improper implementation of Shariah principles due to recently established and lack of experience in managing the companies. The expertise in the Islamic area is essential in enforcing the Shariah principles throughout the company (Hudayati, 2023). Based on the study by Muryanto (2023), there is a lack of supervision and low Shariah compliance among companies in Indonesia, Malaysia, and the United Kingdom. The study suggests fulfilling the need for SSBs and supportive regulations and policies to enhance Shariah compliance among companies. The new establishment also leads to limited government control over Shariah-compliant companies (in the context of non-financial companies) (Ariffin et al., 2021). Additionally, it can be difficult to maintain a constant commitment to Shariah principles due to diverse interpretations in different scholars and geographical areas, which makes it difficult to standardize compliance. Thus, it can be concluded that poor enforcement leads to a high corruption level among companies.

Shariah compliance companies were listed in Islamic Capital Market that have different set of guidelines and mainly focuses on shariah compliant transactions in providing product and services and must not conflicting the Muslims and religion of Islam. Shariah screening methodologies which solely focuses on income statement however have limitations by not including screening method such as ethical conduct (i.e responsibility practices, sustainability or anti-corruption measures) (Malik et al., 2025). This could led companies listed as shariah-compliant but engaging in unethical practices may be perceived as corrupt, as their actions contradict the ethical standards expected of them. This could result in lower corruption scores, reflecting a lack of integrity despite their adherence to shariah compliance in financial transactions.

There are several limitations in this study. First, this study excluded financial institutions from the sample because the operation of financial institutions is under specific regulations and reporting requirements that differ from other sectors. Data limitations and complexities, ethical considerations, and research, focus on broader trends also lead the researcher to exclude financial institutions in this study. Strict regulation on Shariah compliance in financial institutions would influence the result of this study since Shariah compliance for non-financial companies is still in a nascent stage. The second limitation is that our study does not include corporate governance factors in the model because this study specifically does not focus on governance but on the ethical commitment of the companies. The ethical commitment comes from enforcing governance; thus, including the corporate governance factors will redundancy the result of this study. Another limitation of this study is the exclusion of stock market prices and financial performance indicators, such as profits, as independent variables in the analysis. These factors could potentially act as proxies for corruption or ethical behavior, given their strong connection to corporate performance and public transparency. However, their inherent volatility and susceptibility to external influences—such as economic trends, market sentiment, and geopolitical developments—led to their omission from the study. While this decision allowed for a more targeted investigation of the relationships among ETHICS, SHARIAH, and CORRUPTION_SCORE, it also narrows the scope of the findings. Future studies could consider incorporating these variables to offer a more comprehensive perspective on the interplay between ethical governance, financial outcomes, and corruption metrics.

This study recommends conducting a cross-country comparative study, especially for Islamic countries with a dual system of companies, Shariah and conventional, to assess the scenario and ability of conventional companies to compete with Shariah-compliant companies. Thus, future research could offer more interesting results on this topic. Additionally, future research could analyze how leadership styles, ethical communication, and decision-making impact corruption prevention and Shariah compliance in addition to corporate governance factors as a main role. It could specifically analyze the impact of corporate governance systems, such as board composition, oversight mechanisms, and regulatory compliance, on creating ethical commitment and preventing corruption in Sharia-compliant companies.

An important avenue for future research is to more directly examine the role of Shariah compliance in shaping corporate ethical behavior and governance outcomes. While this study focuses on broader measures of voluntary ethical commitment, the unique institutional setting of Malaysia—where Shariah-compliant firms operate under specific ethical and financial principles—offers a valuable opportunity to explore the distinct effects of Shariah governance. Future studies could investigate whether changes in Shariah compliance rules, certification processes, or governance guidelines (e.g., those issued by Bank Negara Malaysia or the Securities Commission) create exogenous variation that can be used to identify causal effects. Leveraging such institutional mechanisms could provide deeper insights into how formal religious-ethical frameworks interact with corporate governance reforms, potentially offering a more granular understanding of ethical commitment in dual financial systems.

Furthermore, policymakers should enhance regulatory frameworks by developing and enforcing policies that explicitly require ethical commitments and Shariah compliance in the workplace. In addition, policymakers should implement reporting standards for Shariah-compliant companies, specifically for non-financial companies, to gain better transparency among companies. Then strengthening whistleblower policy is one of the initiatives that cannot be abandoned in order to create a platform for reporting unethical behavior or corruption. For practitioners, especially business leaders, emphasizing a leadership style that promotes a culture of integrity could encourage ethical commitment throughout the company. The enforcement from the business leader could create oversight for all stakeholders to comply with Shariah principles and ethical guidelines and contribute to better ethical conduct that could reduce the existence of corrupt companies.

Tables & Figures

Table 1.

Tabulation of Industrial Sector and Shariah-Compliant Firms

Table 2.

Descriptive Statistics

Table 3.

Model Specification Test

Table 4.

Pairwise Correlations

*** p<0.01, ** p<0.05, * p<0.1

Table 5.

Main Result

Notes: * , ** and ** represent significance at p<0.1, p<0.05 and p<0.01, respectively, t-values are reported in the parentheses.

Table 6.

Fixed Effect Model

Notes: * , ** and ** represent significance at p<0.1, p<0.05 and p<0.01, respectively, t-values are reported in the parentheses.

Table 7.

Extended Analysis by Including Dummy Variables of Ethical Commitment Indicators

Notes: * , ** and ** represent significance at p<0.1, p<0.05 and p<0.01, respectively, t-values are reported in the parentheses.

Table 8.

Pre- and post-MCCG 2017

Notes: * , ** and ** represent significance at p<0.1, p<0.05 and p<0.01, respectively, t-values are reported in the parentheses.

Table 9.

Heckman Sample Selection and By Hand Sample Selection Estimation

Standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

Table 10.

Propensity Score Matching

Notes: * , ** and ** represent significance at p<0.1, p<0.05 and p<0.01, respectively, t-values are reported in the parentheses.

Table 11.

Two Stage Least Square Estimation

Notes: * , ** and ** represent significance at p<0.1, p<0.05 and p<0.01, respectively, t-values are reported in the parentheses.

References

-

Acheampong, A. O., Boateng, E., and C. B. Annor. 2024. “Do corruption, income inequality and redistribution hasten transition towards (non) renewable energy economy?”

Structural Change and Economic Dynamics , vol. 68, pp. 329-354.

-

Aguilera, R. V. and A. K. Vadera. 2008. “The Dark Side of Authority: Antecedents, Mechanisms, and Outcomes of Organizational Corruption.”

Journal of Business Ethics , vol. 77, no. 4, pp. 431-449.

-

Akimova, L., Litvinova, I., Ilchenko, H., Pomaza-Ponomarenko, A., and O. Yemets. 2020. “The negative impact of corruption on the economic security of states.”

International Journal of Management , vol. 11, no. 5, pp. 1058-1071. -

Alcadipani, R. and C. R. de Oliveira Medeiros. 2020. “When Corporations Cause Harm: A Critical View of Corporate Social Irresponsibility and Corporate Crimes.”

Journal of Business Ethics , vol. 167, pp. 285-297.

-

Alias, N. F., Nawawi, A., and A. S. A. P. Salin. 2019. “Internal auditor’s compliance to code of ethics: Empirical findings from Malaysian Government-linked companies.”

Journal of Financial Crime , vol. 26, no. 1, pp. 179-194.

-

Al-Shaer, H., Albitar, K., and J. Liu. 2023. “CEO power and CSR-linked compensation for corporate environmental responsibility: UK evidence.”

Review of Quantitative Finance and Accounting , vol. 60, no. 3, pp. 1025-1063.

-

Al-Shamali, A., Irani, Z., Haffar, M., Al-Shamali, S., and F. Al-Shamali. 2021. “The influence of Islamic Work Ethic on employees’ responses to change in Kuwaiti Islamic banks.”

International Business Review , vol. 30, no. 5, 101817.

-

Amayreh, I., Ananzeh, H., and A. Bugshan. 2024. “The impact of board of directors and islamic shariah on company internal control: evidence from Jordan.”

International Journal of Economics and Financial Issues , vol. 14, no. 1, pp. 39-51.

-

Andrews, I., Stock, J. H., and L. Sun. 2019. “Weak instruments in instrumental variables regression: Theory and practice.”

Annual Review of Economics , vol. 11, no. 1, pp. 727-753.

-

Arif, M., Sajjad, A., Farooq, S., Abrar, M., and A. S. Joyo. 2021. “The impact of audit committee attributes on the quality and quantity of environmental, social and governance (ESG) disclosures.”

Corporate Governance: The International Journal of Business in Society , vol. 21, no. 3, pp. 497-514.

-

Ariffin, M. M., Riza, N. M., Hamid, M. F. A., Awae, F., and B. M. Nasir. 2021. “Halal food crime in Malaysia: An analysis on illegal meat cartel issues.”

Journal of Contemporary Issues in Business and Government , vol. 27, no. 2. DOI:10.47750/cibg.2021.27.02.152

-

Ascarya, A. and I. Indra. 2022. Standard Methodology for Research in Islamic Economics and Finance (Chapter 17). In Billah, M. M. (Ed).

Teaching and Research Methods in Islamic Economics and Finance . Abingdon-on-Thames, England, UK: Routledge. -

Azam, M., Akram, J., Ali, S. A., and K. Mohy-ud-Din. 2019. “The moderating role of shariah compliance on the relationship between firm profitability and CSR activities.”

International Journal of Ethics and Systems , vol. 35, no. 4, pp. 709-724.

-

Aziz, A. A. 2020. Revive the Value of Islamic Spirituality for an Anti-Corruption Mentality.

International Journal of Psychosocial Rehabilitation , vol. 24, no. 3, pp. 2413-2423.

-

Aziz, H. A. and Z. A. A. Ghadas. 2021.

Corporate governance framework for shariah compliant corporation . Proceedings of the International Joint Conference on Arts and Humanities 2021 (IJCAH 2021). -

Baah, C., Agyabeng-Mensah, Y., Afum, E., and J. A. Lascano Armas. 2024. Exploring corporate environmental ethics and green creativity as antecedents of green competitive advantage, sustainable production and financial performance: empirical evidence from manufacturing firms.

Benchmarking: An International Journal , vol. 31, no. 3, pp. 990-1008.

-

Bank Negara Malaysia. 2018. “Value-based Intermediation: Strengthening the Roles and Impact of Islamic Finance.”

the Strategy Paper , 034-2. -

Barkemeyer, R., Preuss, L., and M. Ohana. 2018. “Developing country firms and the challenge of corruption: Do company commitments mirror the quality of national-level institutions?”

Journal of Business Research , vol. 90, pp. 26-39.

-

Bashir, M. and S. Hassan. 2020. “The need for ethical leadership in combating corruption.”

International Review of Administrative Sciences , vol. 86, no.4, pp. 673-690.

-

Bauhr, M. and N. Charron. 2020. “The EU as a savior and a saint? Corruption and public support for redistribution.”

Journal of European Public Policy , vol. 27, no. 4, pp. 509-527.

-

Benjamin, D. J., Choi, J. J., and G. Fisher. 2016. “Religious identity and economic behavior.”

Review of Economics and Statistics , vol. 98, no. 4, pp. 617-637.

-

Boutchkova, M., Cueto, D., and A. Gonzalez. 2022. “Test power properties of within-firm estimators of ownership and board-related explanatory variables with low time variation.”

Review of Quantitative Finance and Accounting , vol. 59, no. 3, pp. 1215-1269.

-

Busiri. 2020. “Implementation of Anti-Corruption Values in Islamic Education Perspective.”

International Journal of Psychosocial Rehabilitation , vol. 24, no. 4, pp. 5253-5259. DOI:https://doi.org/10.61841/hqc7h384

-

Cieślik, A. and Ł. Goczek. 2022. “Who suffers and how much from corruption? Evidence from firm-level data.”

Eurasian Business Review , vol. 12, no 3, pp. 451-473.

-

Chan, K., Dang, V., and T. Li. 2020. “Corruption and income inequality in China.”

Emerging Markets Finance and Trade , vol. 56, no.14, pp. 3351-3366.

-

Cheong, C. W. H. 2020. “Risk, resilience, and Shariah-compliance.”

Research in International Business and Finance , vol. 55, 101313.https://doi.org/10.1016/j.ribaf.2020.101313

-

Chiang, T. C., Li, J., and L. Tan. 2010. “Empirical investigation of herding behavior in Chinese stock markets: Evidence from quantile regression analysis.”

Global Finance Journal , vol. 21, no. 1, pp. 111-124.

-

Cotton, R. D., Stevenson, W. B., and J. M. Bartunek. 2017. “A way forward: Cascading ethical and change leadership, values enactment, and group-level effects on commitment in corruption recovery.”

The Journal of Applied Behavioral Science , vol. 53, no. 1, pp. 89-116.

-

Cuomo, F., Mallin, C., and A. Zattoni. 2016. Corporate governance codes: A review and research agenda.

Corporate governance: an international review , vol. 24, no. 3, pp. 222-241.

- De Bruin, L., Roberts-Lombard, M., and C. De Meyer-Heydenrych. 2020. Internal marketing, service quality and perceived customer satisfaction An Islamic banking perspective.

-

Dokas, I. 2023. “Earnings Management and Status of Corporate Governance under Different Levels of Corruption—An Empirical Analysis in European Countries.”

Journal of Risk and Financial Management , vol. 16, no. 10, pp. 1-23.

-

Driskill, G., Chatham-Carpenter, A., and K. Mcintyre. 2019. “The power of a mission: Transformations of a department culture through social constructionist principles.”

Innovative Higher Education , vol. 44, pp. 69-83.

-

Duong, H. K., Fasan, M., and G. Gotti. 2022. “Living up to your codes? Corporate codes of ethics and the cost of equity capital.”

Management Decision , vol. 60, no. 13, pp. 1-24.

-

Farooq, O. and A. Alahkam. 2016. “Performance of Shariah-compliant firms and non-Shariah-compliant firms in the MENA region: which is better?”

Journal of Islamic Accounting and Business Research , vol. 7, no. 4, pp. 268-281.

-

Ferdiansah, M. I., Chong, V. K., Wang, I. Z., and D. R. Woodliff. 2023. “The effect of ethical commitment reminder and reciprocity in the workplace on misreporting.”

Journal of Business Ethics , vol. 186, no. 2, pp. 325-345.

-

Frees, E. W. 2004.

Longitudinal and panel data: analysis and applications in the social sciences . Cambridge University Press. -

Giannarakis, G., Andronikidis, A., and N. Sariannidis. 2020. “Determinants of environmental disclosure: investigating new and conventional corporate governance characteristics.”

Annals of Operations Research , vol. 294, pp. 87-105.

-

Halamka, R. and P. Teplý. 2017. “The Effect of Ethics on Banks’ Financial Performance.”

Prague Economic Papers , vol. 26, no. 3, pp. 330-344.

-

Halim, A. A., Sukor, M. E. A., and O. I. Bacha. 2017. “Testing the Capital Structure Behavior of Malaysian Firms: Shariah vs. Non-Shariah Compliant.”

International Journal of Economics and Management Engineering , vol. 11, no. 9.https://waset.org/abstracts/78483 -

Hechanova, M. R. M., and J. O. Manaois. 2020. “Blowing the whistle on workplace corruption: the role of ethical leadership.”

International Journal of Law and Management , vol. 62, no. 3, pp. 277-294.

-

Hausman, J. A. 1978. Specification Tests in Econometrics.

Econometrica , vol. 46, no. 6, pp. 1251-1271.

-

Heckman, J. J. 1976. “The common structure of statistical models of truncation, sample selection and limited dependent variables and a simple estimator for such models.” In Annals of economic and social measurement, vol. 5, no. 4, pp. 475-492. NBER.

http://www.nber.org/chapters/c10491 -

Hemphill, T. A. 2023. “A Case for Effective Business Association Membership Codes of Ethics and Conduct.”

Business and Professional Ethics Journal , vol. 42, no. 1, pp. 55-78.

-

Huda, M. C. and B. Ispriyarso. 2019. “Contribution of Islamic law in the discretionary scheme that has implications for corruption.”

Ijtihad: Jurnal Wacana Hukum Islam Dan Kemanusiaan , vol. 19, no. 2, pp. 147-167.

-

Hudayati, A. 2023. “Exploring the nexus of disclosure of Sharia compliance and governance in Islamic banking: a comprehensive analysis of the sharia supervisory board/Arifah and Ataina Hudayati.”

Management & Accounting Review (MAR) , vol. 22, no.3, 408-428. -

Hussain Khan, M., Fraz, A., Hassan, A., and S. Zohaib Hassan Kazmi. 2022. “Impact of corruption on bank soundness: the moderating impact of Shari’ah supervision.”

Journal of Financial Crime , vol. 29, no.3, pp. 962-983.

-

Hoechle, D. 2007. “Robust standard errors for panel regressions with cross-sectional dependence.”

Stata Journal , vol. 7, no. 3, pp. 281-312.

-

Ismail, N. H. and M. E. S. M. Rasid. 2017. “The relevance of Islamic pillars of sustainable development in promoting shared prosperity.”

E-Academia Journal , vol. 6, no. 2, pp. 264-278. -

Ismail, N. H. and M. E. S. M. Rasid. 2022. “Promoting An Inclusive Economy: The Relevance of Sustainable Development and Islamicity Prosperity Index.”

Journal of Islamic Monetary Economics and Finance , vol. 8, no. 4, pp. 637-660.

-

Jaggi, B., Allini, A., Ginesti, G., and R. Macchioni. 2021. “Determinants of corporate corruption disclosures: evidence based on EU listed firms.”

Meditari Accountancy Research , vol. 29, no. 1, pp. 21-38.

-

Janenova, S. and C. Knox. 2020. “Combatting corruption in Kazakhstan: A role for ethics commissioners?”

Public Administration and Development , vol. 40, no. 3, pp. 186-195.

-

Jensen, M. C. and W. H. Meckling. 1976. “Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure.”

Journal of Financial Economics , vol. 3, pp. 305-360.

-

Jermsittiparsert, K., Chankoson, T., Malik, I., and W. Thaicharoen. 2021. “Linking Islamic Work Ethics with Employee Performance: Perceived Organizational Support and Psychological Ownership as a Potential Mediators in Financial Institutions.”

Journal of Legal, Ethical and Regulatory Issues , vol. 24, no. 15. -

Johari, R. J., Rosnidah, I., Talib, N. A., and I. M. Helmi. 2022. “Role of code of ethics in building a fraud-resilient organization: The case of the developing economy.”

Journal of Governance & Regulation , vol. 11, no. 2, pp. 32-40.

-

Kamaruding, M., Mokthar, M. Z., and S. H. A. Rahman. 2022. “Revising intention as a solution for the corruption issues among actors of construction project management: Analysis from an Islamic perspective.”

AIP Conference Proceedings , vol. 2532, no.1. AIP Publishing.https://doi.org/10.1063/5.0109962 -

Khattak, M. A., Ali, M., and A. K. Burki. 2020. “Sustainability-disclosures and financial performance: Shariah compliant vs Non-Shariah-compliant Indonesian firms.”

Journal of Islamic Monetary Economics and Finance , vol. 6, no. 4, pp. 789-810.

-

La Porta, R., Lopez‐de‐Silanes, F., Shleifer, A., and R. W. Vishny. 2000. “Agency problems and dividend policies around the world.”

The journal of finance , vol. 55, no. 1, pp. 1-33.

-

Lai, J. 2022. Financialised ethics, economic security and the promise of Islamic finance. Asian Journal of Comparative Politics, vol. 7, no. 1, pp. 45-57.

-

Liyanapathirana, N. and C. Akroyd. 2022. Religiosity and accountants’ ethical decision-making in a religious country with a high level of corruption. Pacific Accounting Review, vol. 35, no. 2, pp. 181-198.

-

Law, S. H. 2018.

Applied Panel Data Analysis Short Panels . UPM Press. -

LSEG Data & Analytics. 2024.

Environmental, Social and Governance scores from LSEG , LSEGhttps://www.lseg.com/content/dam/data-analytics/en_us/documents/methodology/lseg-esg-scores-methodology.pdf -

Malik, R., Dar, H., and A. Muneeza. 2025. “Reforms required for Shariah screening of equities using the case study of Dow Jones Islamic market index (DJIMI)”.

International Journal of Law and Management , vol. 67, no. 3, pp. 325-340.

-

Manara, M. U., van Gils, S., Nübold, A., and F. R. Zijlstra. 2020. “Corruption, fast or slow? Ethical leadership interacts with Machiavellianism to influence intuitive thinking and corruption.”

Frontiers in Psychology , vol. 11, no. 578419.https://doi.org/10.3389/fpsyg.2020.578419 -

Manara, M. U., van Gils, S., Nübold, A., and F. R. Zijlstra. 2023. “Exploring the path to corruption–an informed grounded theory study on the decision-making process underlying corruption.”

Plos One , vol. 18, no. 9, e0291819.

-

Martani, D., Khairurizka, R., and R. J. C. B. R. Khairurizka. 2009. “The effect of financial ratios, firm size, and cash flow from operating activities in the interim report to the stock return.”

Chinese business review , vol. 8, no. 6, pp. 44-55. -

Masud, M. A. K., Hossain, M. S., Rahman, M., Chowdhury, M. A. F., and M. M. Rahman. 2024. “Corruption disclosure practices of Islamic and conventional financial firms in Bangladesh: the moderating role of Big4.”

Journal of Islamic Accounting and Business Research , vol. 15, no. 1, pp. 32-55.https://doi.org/10.1108/JIABR-07-2021-0195

-

Merchant, K. A. and L. F. White. 2017. “Linking the ethics and management control literatures.”

Advances in Management Accounting , vol. 28, pp. 1-29. -

Meyer-Sahling, J. H. and K. S. Mikkelsen. 2022. “Codes of ethics, disciplinary codes, and the effectiveness of anti-corruption frameworks: Evidence from a survey of civil servants in Poland.”

Review of Public Personnel Administration , vol. 42, no. 1, pp. 142-164.

-

Miglietta, F. and G. Forte. 2011. “A comparison of socially responsible and Islamic equity investments.”

Journal of Money, Investment and Banking , ISSN 1450-288.http://dx.doi.org/10.2139/ssrn.1819002 -

Mohamad Ariff, A., Abd Majid, N., Kamarudin, K. A., Zainul Abidin, A. F., and S. N. Muhmad. 2023. “Corporate ESG performance, Shariah-compliant status and cash holdings.”

Journal of Islamic Accounting and Business Research . (In press) -

Mohan, M. 2022. “Corruption perceptions index 2021.” Transparency International Malaysia.

https://transparency.org.my/pages/what-we- do/indexes/corruption-perceptions-index-2021 . -

Molina, A. D. 2018. “A systems approach to managing organizational integrity risks: Lessons from the 2014 veterans affairs waitlist scandal.”

The American Review of Public Administration , vol. 48, no. 8, pp. 872-885.

-

Muhmad, S. N., Mohamad Ariff, A., Abd Majid, N., and R. Muhamad. 2023. “Corporate sustainability commitment and cash holding: evidence from Islamic banks in Malaysia.”

Journal of Islamic Accounting and Business Research , vol. 14, no. 5, pp. 782-811.

-

Muryanto, Y. T. 2023. The urgency of sharia compliance regulations for Islamic Fintechs: a comparative study of Indonesia, Malaysia and the United Kingdom.

Journal of Financial Crime , vol. 30, no. 5, pp. 1264-1278.

- Nainggolan, Y., How, J. C., and P. Verhoeven. 2011. “Do Fund Managers Keep Their Promises?: The Case of Shari’ah Equity Funds.” In 2012 Financial Markets & Corporate Governance Conference. December, 2011.

-

Newey, W. K. and K. D. West. 1986. “A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix.”

Econometrica , vol. 55, no. 3, pp. 703-708.

-

Ngcamu, B. S. and E. Mantzaris. 2023. “Policy enforcement, corruption and stakeholder interference in South African universities.”

Journal of Transport and Supply Chain Management , vol. 17, pp. 1-10.

-

Nguyen, L. A., Vesty, G., Kend, M., Nguyen, Q., and B. O’Connell. 2020. “Intertwined institutionalization: Pressures on Vietnam’s accounting profession during transition to IFRS.”

Pacific Accounting Review , vol. 32, no. 4, pp. 475-493.

-

Qaderi, S. A., Ghaleb, B. A. A., Qasem, A., and W. N. Wan‐Hussin. 2024. “Unveiling the link between female directors’ attributes, ownership concentration, and integrated reporting strategy in Malaysia.”