- EAER>

- Journal Archive>

- Contents>

- articleView

Contents

Citation

| No | Title |

|---|

Article View

East Asian Economic Review Vol. 29, No. 3, 2025. pp. 303-335.

DOI https://dx.doi.org/10.11644/KIEP.EAER.2025.29.3.451

Number of citation : 0View

48

Download

54

Dynamic Spillovers in Global Financial Markets: The Effect of Geopolitical Risk, Climate and Economic Uncertainties

|

|

University of Science and Technology Bannu |

|---|

Abstract

This study examines the dynamic impact of Global Economic Policy Uncertainty (GEPU), Climate Policy Uncertainty (CPU), and Geopolitical Risk (GPR) on sustainable markets (DJSI and green bonds), conventional equity market (S&P 500), and commodity markets (oil and gold). Utilizing monthly data from September 2014 to June 2024, the analysis employs a Time-Varying Parameter Vector Autoregression (TVP-VAR) model to capture the dynamic linkages and volatility spillover mechanisms across global financial markets and key risk factors. Unlike prior research focusing on a single uncertainty factor, this study integrates three distinct risk factors accounting for multifaceted global risk, supported by Principal Component Analysis (PCA), across multiple financial markets. To ensure the robustness of the findings, a standard VAR model is estimated, confirming the persistence of spillover dynamics. The results offer three major insights: First, the impact of uncertainty is heterogeneous across the financial markets, and is amplified especially during crises such as COVID-19 and geopolitical conflicts. Second, GEPU, GPR, and S&P 500 emerged as dominant volatility transmitters, while gold and sustainable assets exhibit hedging properties highlighting their role in portfolio diversification. Finally, periods of heightened uncertainties lead to asymmetric and time-varying transmissions, emphasizing the importance of adaptive risk management strategies. The results of the study provide understanding of how various risk factors affect financial markets, offering valuable insights to investors, policy-makers, and portfolio managers seeking resilience to the global crisis.

JEL Classification: G11, G15, F51

Keywords

Volatility Connectedness, Global Financial Markets, Climate and Economic Uncertainties, Geopolitical Risk

I. Introduction

The interplay between EPU, CPU and GPR with financial markets has attracted significant attention for its critical role in shaping global economic and financial dynamics. Caldara and Iacoviello (2018) argued that high level of geopolitical risk associate with decrease in economic activities, capital flight from developing to developed markets and consequently decline in stock returns. The outbreak of the Russia-Ukraine war in February 2022 had profound economic repercussions, particularly on financial and currency markets. The Russian Ruble experienced a sharp depreciation, plummeting from 66 to 133 per U.S. dollar. Similarly, the currencies of Central European nations faced significant declines, with the Czech koruna and Hungarian forint losing 12% and 27% of their value against the U.S. dollar, respectively, by August 2022. Furthermore, stock markets in Germany and Italy emerged as some of the worst-performing in Europe, primarily due to their heavy reliance on Russian energy and economic ties. Additionally, Poland and Hungary experienced substantial declines in both equity valuations and currency stability, given their geographical proximity to the conflict zones and heightened exposure to geopolitical risks.1

In addition to the geopolitical risk, climate policy uncertainty recently emerged as a risk factor for global financial and economic systems (Liu et al., 2025). More recently, Ji et al. (2024) suggested that the risks arising from unexpected changes in climate policy significantly influence the price volatility of underlying financial assets, ultimately exerting profound effects on the stability of the global financial system. As governments increasingly adopt stringent climate policies to address environmental degradation and carbon emissions, the uncertainty surrounding these policies has profound implications for global financial markets (Di Tomaso et al., 2024). The authors argued that climate uncertainty increasingly influences global financial markets through impacts on asset prices, investment strategies, and market stability. Understanding how global financial markets react to such uncertainty is essential for investors, policymakers, and academics aiming to navigate an increasingly volatile financial landscape.

Effective management of risks arising from variations in CPU is essential when diversifying investments. Krueger et al. (2020) argued that investors should prioritize a risk management approach over divestment strategies when addressing climate-related risks in their portfolios, particularly for assets with high exposure to such risks. Adopting this approach, however, requires a comprehensive understanding of the interactions between various financial and commodity markets that can serve as hedging instruments against climate risk. This necessitates examining the role of climate uncertainty as a key driver of shock spillovers across markets to develop effective diversification strategies for mitigating exposure to climate-related risks.

Since the introduction of EPU index by Baker et al. (2016), there has been a growing body of research focusing on the dynamic effects of EPU on financial markets across diverse contexts and conditions. Baker et al. (2016) revealed that heightened levels of policy uncertainty, as measured by the EPU index, were associated with increased stock market volatility, alongside declines in investment and employment in sectors vulnerable to policy-related changes. Guo et al. (2018) found that elevated EPU was associated with a decline in stock market returns across both G7 and BRIC countries, highlighting its adverse impact on global financial markets. Nguyen et al. (2020) conducted a comprehensive analysis of the impact of EPU on stock markets in the U.S. and eight European Union (EU) countries.2 Their study revealed that heightened levels of uncertainty in the U.S. significantly reduce stock returns across all EU markets analysed. Similarly, increased uncertainty in specific EU markets, such as Ireland, Spain, Sweden, and the UK, was found to exert adverse effects on U.S. stock returns. This evidence aligns with broader literature highlighting the substantial influence of EPU on various financial markets, including equities (Nguyen et al., 2020; Adebayo et al., 2022), commodities (Oliyide et al., 2021; Hoque and Zaidi, 2020), and cryptocurrencies (Al-Mamun et al., 2020).

The objective of the study is to examine on the one hand the extent of dependence between sustainable, traditional and commodities markets over time. In addition, despite the increasing relevance of EPU, CPU, and GPR, there remains a lack of comprehensive analysis focusing concurrently on how these uncertainty impacts the commodities markets (oil and gold) and both the traditional and sustainable financial markets. On the other hand, this study aims to fill the gap in the existing literature by analyzing the dynamic interconnectedness between EPU, CPU, and GPR with traditional financial markets, and sustainable markets using monthly data from September 2014 to June 2024. While most existing studies have focused on traditional safe-haven assets such as oil and gold, the current study broadens the scope by including sustainable assets such as green bonds and stocks. Additionally, whereas prior research has primarily examined the effects of EPU and GPR at the country level, this study expands the analysis by incorporating CPU and a more diverse set of asset classes, including global stock prices. This will help in identifying the risk transmitters and risk receivers during the crisis’s episodes. The study period captures key global events, including major climate summits including the Paris Agreement of 2015, regulatory shifts, economic crises due to COVID-19 and the heightened geopolitical tensions including the Russia-Ukraine war and the Israel-Palestine conflict, providing a rich dataset for understanding the evolving relationship between the uncertainty and financial markets.

The findings of this study will contribute to the existing body of knowledge by offering a more nuanced understanding of how CPU, EPU and GPR influences commodities markets and both the traditional and sustainable financial assets. Previous studies mainly focused on the individual uncertainty factors in conjunction with either stock markets and/or the commodities. Secondly, this study helps identify markets that can serve as hedges against the three uncertainty factors. In addition, for building efficient portfolio, investors should analyze the behavior of sustainable and traditional financial markets as well as their interactions with the vital commodities especially oil and gold. Moreover, Di Tommaso et al. (2024) emphasize that the growing prominence of climate risk underscores the critical need for integrating climate-related considerations into the decision-making frameworks of investors, corporations, and regulatory bodies. Finally, this study examines three key uncertainty factors, whereas existing literature has primarily focused on a single uncertainty or, at most, a combination of two. Therefore, a thorough understanding of the impact of CPU, GEPU, and GPR on financial markets is essential for various stakeholders to effectively manage associated risks and identify potential opportunities. Gaining such insights is particularly valuable for investors, policymakers, and researchers, who are increasingly concerned with the financial implications of uncertainty and risk in global markets. By addressing these relationships, this research aims to enhance decision-making in portfolio management and guide policy discussions on the financial impact of GEPU, CPU and GPR.

The structure of the study is organized as follows: Section II offers a comprehensive review of the relevant literature. Section III details the dataset and methodology employed in the analysis. Section IV presents the empirical findings derived from the study. Lastly, Section V provides the concluding remarks, summarizing key insights and implications.

1)For more details about the impacts of Russia-Ukraine war, please see

2)The European countries included France, Germany, Greece, Ireland, Italy, Spain, Sweden, and the UK.

II. Literature Review

The literature review section has been divided into two sub-sections; first, sub-section II.1, represents the theoretical framework of the study. Sub-section II.2 provides a detailed review of the empirical literature.

1. Theoretical Framework

Theoretically this study is related to the portfolio theory proposed by Markowitz in 1952. The theory mainly advocates the diversification of various assets into a portfolio rather than investing in individual securities. This proposition is based on diversification of assets having weak correlations. During turmoil episodes, inter-connections among the markets increases having limited benefits from diversifications. Investors therefore look for un-related assets to gain from diversification. In the recent times, due to financialization of commodities, innovation in fintech, and the emergence of cryptocurrencies, investors reallocate their investments into a diverse set of alternative assets to minimize risk. Efficient Market Hypothesis (EMH) suggests that markets quickly reflect available information. According to Lo (2004) and Malkiel (2003), during heightened uncertainties, the market may exhibit delayed responses. The Real Options Theory (Bernanke, 1983) suggested that investors will postpone investments to some future time during higher uncertainties due to higher risk-aversion. The decrease in investment in turn results in lower output and consequently macroeconomic fluctuations (Bloom, 2009).

According to the prospect theory (Kehneman and Tverskey, 1979), investors exhibit asymmetric responses to good news and bad news. During periods of high uncertainty, investor’s risk aversion might intensify. Consequently, they attach more value to bad news as compared to good news. This is supported by the Uncertainty and Risk Aversion Theory (Bloom, 2009; Paster and Veronesi, 2012) postulated that higher uncertainty leads to increased risk premium demanded by investors consequently resulting in lower assets valuations. Bossman et al. (2023) argued that heightened economic policy uncertainty adversely affect the precision in estimates of risk and return resulting in augmenting the risk aversion of investors.

2. Empirical Literature Review

This study examines three significant strands of empirical literature addressing the uncertainties arising from GEPU, CPU, and GPR and their impact on financial markets. Recent research has primarily analyzed these uncertainty factors either in isolation or by considering at most two in combination, thereby overlooking the comprehensive interplay among these critical risk factors. The growing importance of these uncertainties within the global economic system has elevated this topic to a crucial area of academic inquiry. A brief overview of the three strands focusing on each of these uncertainty factors is provided below.

The foundational work of Caldara and Iacoviello (2022) catalyzed a significant body of literature examining the implications of GPR, which is linked to events such as wars, political crises, and terrorist activities that disrupt national and international relations. Caldara and Iacoviello (2022) posited that elevated level of GPR lead to a contraction in real economic activity, heightened financial market volatility, and wider corporate credit spreads. Moreover, their study highlighted that the disruptions caused by GPR extend beyond the economy, permeating financial markets and amplifying overall uncertainty.

Geopolitical risk exerts an asymmetric impact on the global economy by influencing trade dynamics, shaping fiscal and monetary policies, and affecting financial markets (Asomaning and Shah, 2023; IMF, 2023; Sohag et al., 2023). Pastor and Veronesi (2012) and Uche et al. (2022) argued that GPR significantly affects investment decisions and directly impacts the global economy. Wang et al. (2022) emphasized the concept of geopolitical risk spillover, which transmit political and security uncertainties across countries and regions. This phenomenon carries significant implications for global economic stability and the performance of financial markets.

The impacts of geopolitical events on financial markets are well-documented. Events such as civil unrest, armed conflicts, and terrorist attacks generate significant uncertainty, resulting in increased volatility in stock and financial markets (Elsayed and Yarovaya, 2019; Guidolin and La Ferrara, 2010; Kollias et al., 2013). Geopolitical shocks are also closely associated with changes in crude oil prices, as demonstrated by Liu et al. (2019), who found that geopolitical events significantly influence oil price volatility.

Elsayed and Helmi (2021) examined the impact of GPR on MENA and GCC countries, revealing that during significant political events such as the Arab Spring uprisings (2010-2011), the Yemen Civil War, the 2008 global financial crisis, and political tensions between Qatar and other GCC nations, the GPR index acted as a net transmitter of spillovers to Bahrain, Kuwait, and Saudi Arabia. Recent studies further emphasize that geopolitical events have caused substantial disruptions in financial markets (Liu et al., 2023; Mignon and Saadaoui, 2024). Feng et al. (2023) analyzed the impact of GPR on capital flows across 45 major economies. The study found that heightened geopolitical risks negatively influenced capital flows in the countries under investigation. These results underscore the sensitivity of capital markets to geopolitical conditions and highlight their critical role in maintaining global financial stability.

In the context of emerging markets, Asomaning et al. (2024) analysed the impact of geopolitical risk on Ghana's macroeconomic variables using the TVP-VAR model. Their findings demonstrate that GPR significantly influences key macroeconomic indicators, including foreign exchange reserves (FXI), real exchange rates (REER), consumer price indices (CPI), and debt levels. This underscores the critical role of geopolitical risk in transmitting shocks to national economies and shaping macroeconomic dynamics.

The second strand of the literature examined the impact of economic policy uncertainty on financial markets. Nguyen et al. (2020) emphasized that financial markets exhibit significant sensitivity to both domestic and global uncertainties, as these factors can influence critical macroeconomic indicators, including output, employment, productivity, interest rate spreads, and capital flows. Their study investigated the spillover effects of trans-Atlantic macroeconomic uncertainties on stock market returns in the U.S. and eight European countries from 2000 to 2019, employing the DCC-GARCH model.3 The results showed that rising US economic uncertainty negatively impacts all EU stock markets, while uncertainties in Spain, Ireland, Sweden, and the UK significantly affect the U.S. stock returns. Additionally, U.S. EPU has a dynamic influence on European markets, with stronger negative impacts observed during bear markets. In bull markets, only increases in U.S. EPU significantly affect EU stock returns. Conversely, EPUs in Germany, Spain, and the UK impact U.S. stock returns primarily during bear markets.

Government policy uncertainty plays a critical role in shaping economic and financial decision-making. Gulen and Ion (2016) highlighted that heightened government policy uncertainty can alter or delay investment, consumption, and saving decisions of economic agents. Their study provided evidence that firms tend to reduce or postpone investment during periods of higher policy uncertainty. Similarly, Pastor and Veronesi (2012, 2013) emphasized that policy uncertainty increases expected risk premia, volatilities, and correlations in stock markets. They argued that policy uncertainty undermines financial stability by directly shifting risks in financial markets and reducing the value of government-provided protections. These findings are consistent with the observations of Al-Mamun et al. (2020), who suggested that EPU significantly affects stock market returns and volatility.

Several studies have explored the impact of uncertainty on financial markets. Belke et al. (2018) showed that Brexit-induced policy uncertainty will continue to cause instability in key financial markets and has the potential to damage the real economy in both the UK and other European countries. Shaikh (2020) found that increased policy uncertainty adversely affects the stock market, commodity prices, and overall economic stability. However, the growing significance of climate-related policies has shifted the focus toward understanding how CPU influences both traditional and sustainable financial assets, including green bonds and environmentally conscious stock indices.

Finally, a growing body of research has focused on the uncertainty arising from climate change, leading to the emergence of CPU as a critical area of study. The concept of risk associated with climate change has gained significant attention from researchers seeking to understand the influence of CPU on global financial markets. This emerging field has prompted investigations into the role of CPU as a risk factor in asset valuation and investment decisions. CPU captures the unpredictability of government actions related to environmental regulations and climate policies, which can introduce volatility, particularly in financial markets linked to environmental and sustainable investments. Interest in the impact of CPU has intensified in recent years, particularly following the introduction of the CPU Index by Gavriilidis (2021). Moreover, the rising occurrence of climatic anomalies and natural disasters, including tsunamis, hurricanes, droughts, and floods—frequently linked to global warming—has intensified market volatility and impeded global economic growth (Cheng et al., 2023; Shahrour et al., 2023).

A growing body of academic research has explored the impact of CPU on various financial markets. As highlighted by the Financial Stability Board (FSB, 2020), climate change presents significant challenges to the global financial system, primarily categorized as physical risks and transition risks. Physical risks emerge from the escalating intensity and frequency of climate-related extreme weather events, alongside gradual shifts in climate patterns, which can lead to substantial economic losses by depreciating the value of financial assets and amplifying liabilities. Transition risks, conversely, arise from the global movement toward a low-carbon economy. Although this transition is critical for mitigating climate change, the policy reforms and structural adjustments it necessitates can disrupt asset valuations, creating uncertainties in financial markets and increasing liabilities. Collectively, these risks pose significant challenges to the stability and resilience of the financial system.

Lasisi et al. (2024) highlighted that stock market volatility in both the U.S. and the UK is particularly sensitive to elevated levels of CPU. In the context of energy markets, research has identified differential impacts of CPU on green versus brown energy stocks. Bouri et al. (2022) demonstrated that uncertainty surrounding climate-related legislation and policies serves as a more reliable predictor of the performance of green energy stocks compared to brown energy stocks. Furthermore, their findings suggest that CPU exerts a stronger positive influence on the performance of green energy equities relative to their brown counterparts.

Similarly, Tian et al. (2022) examined green bond markets in Europe, China, and the U.S., revealing significant heterogeneity in pricing dynamics across these regions. Their findings highlighted that the Chinese green bond market experiences asymmetrical short-term influences due to CPU, whereas the European green bond market exhibits a more pronounced long-term asymmetric impact compared to the U.S.

Liang et al. (2022) utilized a news-based CPU measure to analyse volatility within the renewable energy index, concluding that CPU negatively affects long-term volatility in renewable energy markets. Shang et al. (2022) similarly noted that rising CPU significantly dampens long-term demand for renewable energy, emphasizing the detrimental impact of policy uncertainty on the sector. He and Zhang (2022) further observed that oil industry stock returns are adversely influenced by increased CPU.

Siddique et al. (2023) expanded on these findings, demonstrating that CPU positively affects the returns of most renewable energy assets across various quantiles and frequencies. As global warming intensifies, there is growing consumer awareness about reducing reliance on fossil fuels, which drives increased investment in renewable energy resources by individuals, corporations, and governments. These changes in CPU have been shown to influence the demand for clean and renewable energy, thereby impacting the performance of renewable energy companies and their stock prices.

Finally, Ren et al. (2023b) revealed that extreme climate events or significant changes in climate policies significantly strengthen the causal relationship between CPU and the performance of traditional energy and green markets. These findings underscore the critical role of CPU in shaping financial market dynamics and the broader energy sector.

Building on the insights gained from the preceding literature review, it is evident that prior studies have predominantly examined uncertainty factors in isolation, neglecting their combined influence on financial markets. Grounded in key theoretical risk factors, this study highlights the critical need for a comprehensive analysis of multiple uncertainty dimensions to fully capture their combined effects on diverse financial markets. To address this critical gap, the present study seeks to investigate the interplay of CPU, GEPU, and GPR in shaping the volatility and connectedness of various financial markets, including commodities (oil and gold), traditional stock markets (S&P 500), and sustainable markets (green bonds and DJSI). Specifically, this study pursues three objectives: first, to examine the dynamic linkages and spillover effects between these uncertainty indices and the financial markets under consideration; second, this study employed a more recent data (September 2014 to June 2024) and utilized the TVP-VAR model, which is particularly suited for capturing nonlinear and time-varying interactions; and third, to provide novel insights that can guide investors and policymakers in navigating the interconnectedness of financial markets amidst rising economic, climate, and geopolitical uncertainties.

3)The countries included France, Germany, Greece, Ireland, Italy, Spain, Sweden, and the UK.

III. Data and Methodology

This study investigates the impact of CPU, GEPU and GPR on volatility spillovers effects on the commodities market (gold and oil) traditional stock market (S&P 500) and sustainable markets (Green bond and DJSI) over time.4 The study employs monthly data spanning from September 2014 to June 2024 to analyze the impact of CPU, GEPU, and GPR on the markets under consideration. The selection of the multiple uncertainties is based on the uniform data availability, their distinct impact on the financial markets and their wide use in the recent studies (Ayadi and Mbarek, 2025; Hu and Borjigin, 2024; Bossman et al., 2023). Specifically, Hu and Borjigin (2024) argued that there is a significant correlation among the three uncertainty risk factors, presenting a systemic risk to global financial markets, and that their combined effect on financial markets is highly significant. The time period investigated is comparable to a number of recent studies focusing on the connectedness between the uncertainty factors and financial markets (Bossman et al., 2023; Khan, 2024). The sample period is particularly pertinent for examining these relationships due to several critical factors. First, the growing prominence of climate policy initiatives, especially following the 2015 Paris Agreement, which introduced new uncertainties and regulatory shifts with significant implications for financial markets.5 Second, the COVID-19 pandemic introduced unprecedented disruptions to global economic and financial system impacting the global economic and financial stability. Finally, the Russia-Ukraine war and subsequently the Israel-Palestine conflict further exacerbated geopolitical risks and led to volatility in global financial markets. Monthly closing price data are used for the U.S. (S&P 500), West Texas Intermediate (WTI) Crude oil prices (oil), gold prices (gold), Dow Jones Sustainability Index (DJSI), S&P Green Bonds Index (Gbonds), along with the three uncertainty indices of CPU, GEPU and GPR.6 The rationale for selecting these financial markets is as follows: the S&P 500 is widely regarded as a benchmark for the global equities market. Oil and gold are key commodities that exhibit both direct and indirect transmission effects on financial markets. Moreover, their roles as safe-haven and hedge assets have been extensively studied, particularly during periods of market turbulence. Green bonds and sustainable equity markets are included due to their distinct characteristics compared to traditional markets and their potential connection to climate-related initiatives, introducing a novel channel explored in recent literature.

In 2014, the issuance of green bonds totalled approximately $37 billion. This figure experienced significant growth, reaching a peak of approximately $633 billion in 2021. However, a slight decline was observed in subsequent years, with green bond issuances amounting to $487 billion in 2022 and $620 billion in 2023.7 The size of the green bond market is estimated to be valued at $525.72 billion in 2024 and is projected to grow to $1,033.43 billion by 2031, representing a compound annual growth rate (CAGR) of 10.1 percent over the forecast period from 2024 to 2031.8

This study utilized established indices to analyse uncertainty factors. The CPU Index, developed by Gavriilidis (2021), was constructed by searching for terms related to regulatory and policy uncertainties in eight prominent U.S. newspapers from April 1987 onward.9 The GPR Index, created by Caldara and Iacoviello (2018, 2022), measures geopolitical risks by analysing articles from leading global newspapers such as

The variables were selected on the basis of their global importance. S&P 500 index is commonly used as a representative of the world stock markets and the global economy (Gao et al., 2023; Khan, 2024). According to Al-Mamum et al. (2020) the GEPU index outperformed the U.S.-EPU in predicting the risk premia for bitcoins. Green bonds and DJSI are selected due to their prominent role in the sustainable markets. Green bonds emerged as an alternative environmentally friendly investment especially after signing of the Paris Agreement and has attracted investor’s attention. The commodity markets, specifically crude oil and gold, are included in the analysis due to their significant influence on the global financial system. These commodities are particularly valued for their roles as safe-haven assets and effective hedging instruments, especially during periods of economic or geopolitical crises. (Shahzad et al., 2020; Gao et al., 2023). The selection of the sample period was based on the time period covering the time of various crisis periods including the COVID-19, the Russian invasion in Ukraine and the Israel-Palestine conflict.11

To examine the dynamic volatility interconnections among the markets, this study employs the TVP-VAR model, an extension of the Diebold and Yilmaz (2012, 2014) framework as proposed by Antonakakis et al. (2020). Specifically, the analysis explores the interconnectedness between traditional markets (S&P 500), sustainable markets (DJSI and Green Bonds), and commodities (crude oil and gold) in conjunction with uncertainty factors such as CPU, GEPU, and GPR. The TVP-VAR model addresses the limitations of traditional VAR models by mitigating issues of overly smoothed parameters and retaining valuable observations, ensuring a robust and comprehensive analysis. Furthermore, this framework facilitates a dynamic evaluation of spillover effects as they evolve over time. The model, selected with a lag of one based on the Bayesian Information Criterion (BIC), is mathematically expressed as follows:

In Equation (1) and Equation (2)

The TVP-VAR model, incorporating a stationary order of

The dynamic nature of Equation (3) allows it to be expressed in a moving average representation as follows:

In this framework,

The use of time-varying coefficients in the Vector Moving Average (VMA) model facilitates the computation of Generalized Forecast Error Variance Decompositions (GFEVD), as proposed by Koop et al. (1996) and Pesaran and Shin (1998). This approach ensures robustness in the results, irrespective of variable ordering. Accordingly, the H-step-ahead forecast error variance decomposition is determined using the following equation:

In context of Equation (5), Σ denotes the covariance matrix of the error term

The diagonal element

Equation (5) is expressed in its normalized form as follows:

The GFEVD, introduced by (Diebold and Yilmaz, 2012), measures the proportion of the error variance of variable

The Total Connectedness Index (TCI), derived from the GFEVD, quantifies the overall level of interconnectedness among variables in the system. It is calculated using the following equation:

As a result, the primary emphasis is on how variable

Here  reflects the time-varying response of all other variables

reflects the time-varying response of all other variables

Additionally, the total directional connectedness

In this context,  denotes the time-varying response of variable

denotes the time-varying response of variable

The net spillovers from a variable

A positive NC value means that variable

The TVP-VAR framework offers a robust methodology for analyzing the propagation of shocks across interconnected variables, effectively capturing the dynamics of uncertainty spillovers. This study uses monthly data and utilizes the TVP-VAR model to investigate the dynamic interrelationships between CPU, GEPU, and GPR across multiple market categories, including commodities (crude oil and gold), sustainable markets (DJSI and green bonds), and traditional markets (S&P 500). The framework is particularly well-suited for examining the transmission of risk from one market to others on a global scale.

4)Worldwide, the Dow Jones Sustainability Indices (DJSI) is the first global family of indices to track the financial performance of leading sustainability companies.

5)The Paris Agreement was proposed during the 21st Conference of the Parties (COP21) to the United Nations Framework Convention on Climate Change (UNFCCC), held in Paris, France, from November 30 to December 12, 2015. It was formally adopted on December 12, 2015, and came into effect on November 4, 2016.

6)Monthly data for CPU, GPR and GEPU were collected from the Economic Policy Uncertainty database (

7)

8)

9)The eight newspapers include Boston Globe, Chicago Tribune, Los Angeles Times, Miami Herald, New York Times, Tampa Bay Times, USA Today and the Wall Street Journal.

10)The countries included Australia, Brazil, Canada, Chile, China, Colombia, France, Germany, Greece, India, Ireland, Italy, Japan, Mexico, the Netherlands, Russia, South Korea, Spain, Sweden, the UK, and the U.S.

11)The COVID-19 pandemic was officially recognized by the World Health Organization (WHO) on March 11, 2020. The Russia-Ukraine conflict commenced on February 24, 2022, following Russia’s military invasion of Ukraine. The Israel-Palestine conflict escalated significantly on October 7, 2023.

IV. Empirical Results and Discussions

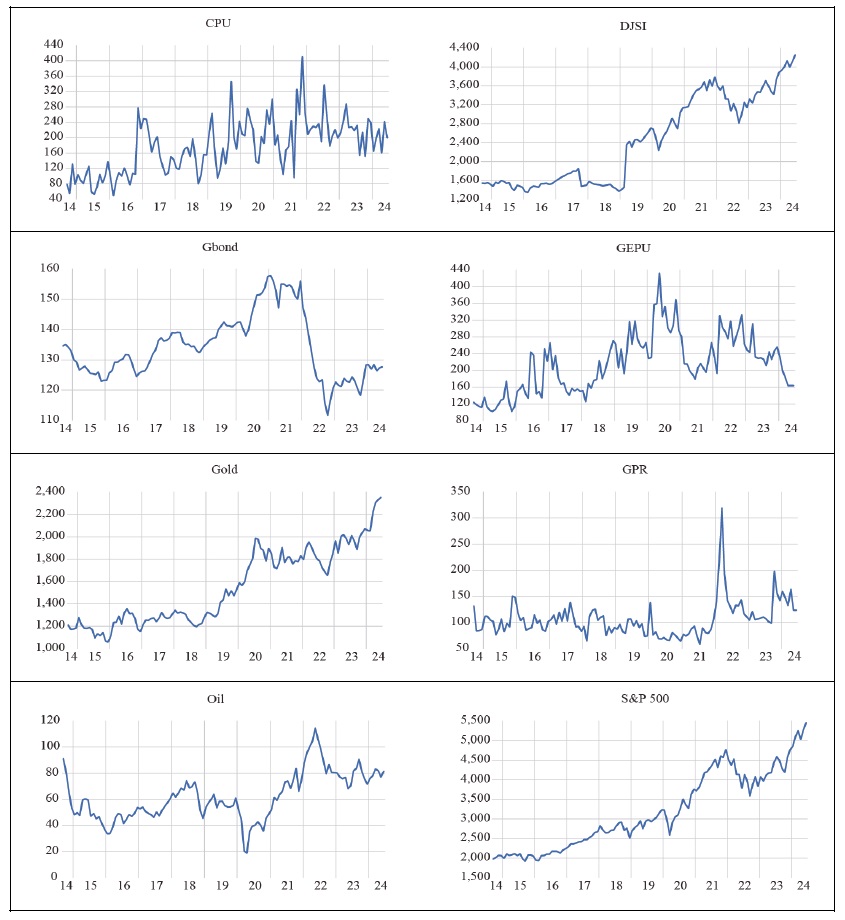

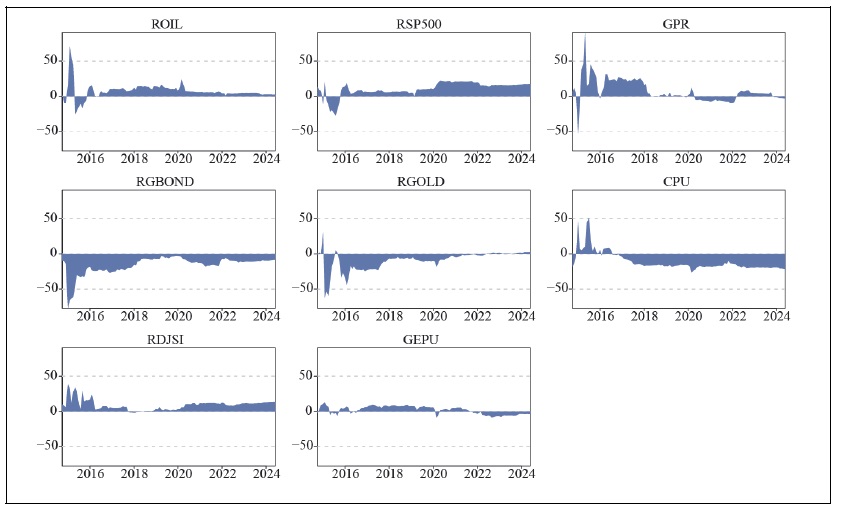

Figure 1 represents the monthly plots of all variables from September 2014 to June 2024 to visualize the time varying fluctuations in the eight variables under investigation. The visual inspection of the figure indicates that the uncertainties indices (CPU, EPU and GPR) show similar trends during the period with heightened uncertainties over the crisis episodes such as COVID-19 and the Russia-Ukraine war periods. The gold prices showed a consistent increase over the crisis episodes indicating its safe-haven property. Both the oil prices and S&P 500 showed a decline during the COVID-19 period. GPR and oil prices showed the highest values during the Russia-Ukraine war period.

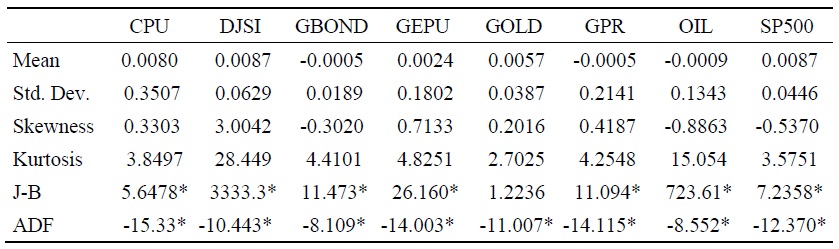

Table 1 presents the summary statistics of all variables included in this study. The visual inspection of Table 1 indicate that CPU exhibits the highest level of risk, followed by GPR, as measured by the standard deviation. This aligns with the significant increase in global climate policy uncertainty, driven by a series of critical climate policy events after late 2015. The elevated standard deviation for GPR may also reflect the escalation of geopolitical tensions, particularly due to the ongoing conflicts between Russia and Ukraine, and Israel and Palestine. Among the financial markets, the DJSI and S&P 500 exhibit the highest average returns, followed by gold and green bonds. Notably, oil, despite having the lowest average return, also demonstrates the second-highest level of risk, highlighting its underperformance relative to other financial assets over the sample period. Furthermore, sustainable assets, represented by the DJSI and green bonds, display lower volatility and reduced skewness, suggesting they may be considered safer investment options for those concerned with climate policy impacts. The skewness and kurtosis statistics indicate that all financial series exhibit significant non-normal characteristics, such as skewed distributions and leptokurtosis. These findings are corroborated by the Jarque-Bera test, which confirms non-normal behaviour for all series except for the gold market. The results of the Augmented Dickey-Fuller (ADF) tests reject the unit root null hypothesis at the 1% significance level in all cases, indicating that all return series are stationary.

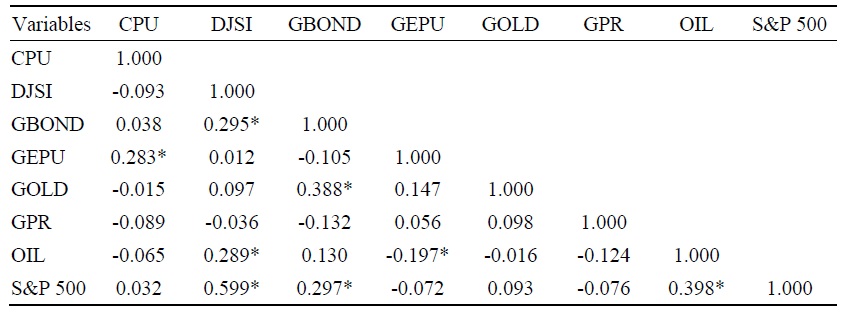

Table 2 presents the correlation matrix between the variables. The table reveals that the CPU is negatively correlated with sustainable stock, oil, gold, and GPR. This negative correlation suggests that higher levels of climate policy uncertainty are associated with lower returns in these markets. In other words, as uncertainty surrounding climate policies rises, these markets tend to underperform, likely due to investor concerns about the potential economic impact of such uncertainties. This can result in reduced investor confidence and lower prices for stocks, crude oil and gold, thereby increasing volatility in these markets. On the other hand, CPU weakly positively correlated with green bonds and S&P 500. The association between CPU and GEPU is positive and significant based on a similar textual analysis methodology of CPU and GEPU. This positive significant association corroborate with Ji et al. (2024). The highest positive correlation is reported between DJSI and S&P 500 indicating that equity market association increased due to uncertainty. These findings are in agreement with most previous studies investigating linkages among the markets in turbulent periods. There is a positive and statistically significant correlation between green bonds and gold. This indicates that green bonds and gold tend to move in the same direction, possibly because both are viewed as safe-haven assets during times of uncertainty, including climate policy changes.

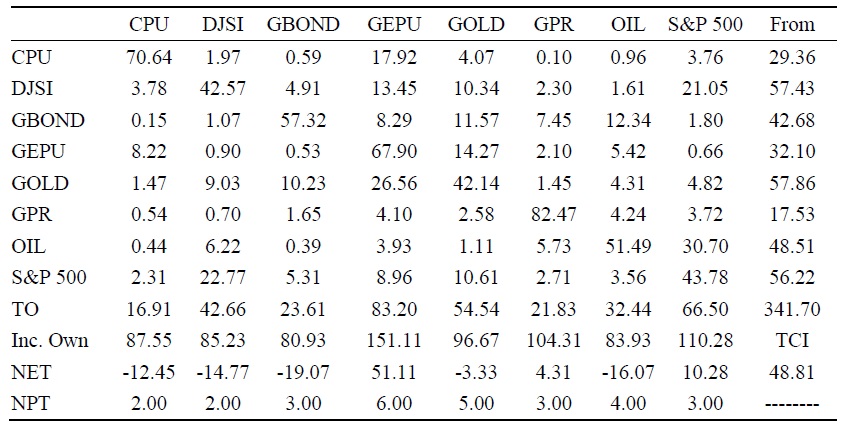

Table 3 shows that the total spillover index is 48.81%. This index captures the contribution of volatility spillovers across all variables in the system to the total forecast error variance (Diebold and Yilmaz, 2012). Therefore, the result suggests that 48.81% of the volatility forecast error variance for all eight variables in the system arises from spillovers, meaning it is due to shocks from other variables. The table also reveals that the gross directional volatility spillovers from other markets to the DJSI and S&P 500 are relatively significant, at 57.43% and 56.22%, indicating notable volatility in these two markets from external sources. Meanwhile, the gross directional volatility spillovers transmitted to other markets are 42.66% and 66.50%, respectively. This implies that 42.66% and 66.50% of the volatility observed in other markets can be attributed to shocks originating from the DJSI and S&P 500 markets. These results highlight the interconnectedness of the DJSI and S&P 500 with other variables, showing that both markets are influential sources of volatility and are also responsive to external market fluctuations.

Similarly, it can be observed that the spillover transmitted by GEPU to other markets is 83.20%, while the spillover it receives accounts for 32.10%, indicating that GEPU is a major transmitter of shocks within the system. The results also show that the spillover of CPU transmitted to (or received from) other markets is 16.91% (29.36%). This suggests that, compared to the CPU index, GEPU is a more influential source of volatility and is more responsive to external market fluctuations.

The findings reveal that the GEPU index exerts a greater influence on financial markets than the CPU and GPR indices, underscoring the critical role of GEPU in shaping financial market dynamics. The GPR index is identified as the primary source of shocks to the green bond and oil markets, contributing 7.45% and 5.73%, respectively. Furthermore, the analysis indicates a strong interconnectedness between the S&P 500 and DJSI in terms of volatility spillovers, accounting for 21.05% and 22.77%, respectively, highlighting a robust relationship between sustainable and conventional markets during periods of uncertainty.

The results conclude that among the uncertainty factors, GEPU and GPR emerge as the principal transmitters of volatility, while commodity markets (oil and gold) and sustainability markets (DJSI and green bonds) are predominantly net receivers of volatility. These findings suggest that during periods of heightened uncertainty, sustainable markets and commodity markets serve as effective hedging tools compared to traditional stock markets. Investors can mitigate risk by incorporating these alternative assets into their portfolios, particularly during extreme market events.

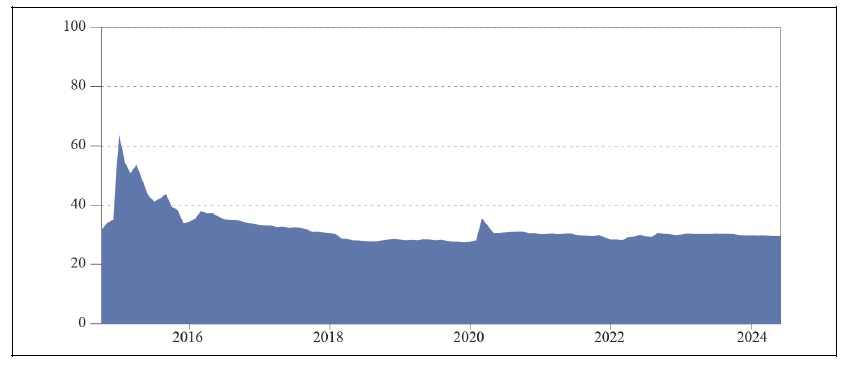

Figure 2 illustrates the overall trend in the connectedness among CPU, GEPU, GPR, and the financial markets represented by gold, oil, DJSI, and green bonds between September 2014 and June 2024. The figure reveals that spillover was notably high during 2014-2015, driven by several significant events, including the oil price crash (2014-2016), the Chinese stock market crash in June 2015, the Greek debt crisis in July 2015, the Federal Reserve interest rate hike in December 2015, and the China-US trade war in 2014. These events collectively contributed to the highest level of volatility observed during the examined period. This was followed by a relatively stable period until 2020, when a sharp spike in volatility occurred due to the unprecedented disruption of the global economy caused by COVID-19. The health crisis led to severe disruptions in global supply chains, labor markets, consumer behavior, and investor sentiment (Cheong et al., 2021). Additionally, the Russia-Ukraine conflict, which began in February 2022, introduced new geopolitical risks with far-reaching implications for global financial markets. The interest rate hikes in 2022 and 2023 further heightened volatility during this period. The Russia-Ukraine crisis, followed by the Israel-Palestine conflict, directly impacted essential commodities, with the effects of these crises reverberating across international markets.

Figure 3 shows the time evolution of the net spillover index for each variable. Positive (negative) values represent volatility transmitters (receivers) to (from) other variables. The figure highlights that GEPU, GPR, and the S&P 500 are the primary contributors of net spillover to the system during the investigated period. This is expected, as both GEPU and GPR were heightened due to various recent events, which are known to have influenced global financial markets. In addition, the crude oil market also acted as net transmitter indicating the oil market strong influence on the other markets. These findings corroborate with Wang et al. (2022) who found oil to act as major net contributor. The impact of GEPU as a strong volatility transmitter in comparison to GPR corroborates with the finding of Das et al. (2019) who found that economic policy uncertainty exerted more influence on the markets as compared to geopolitical risk and financial stress.12 On the other hand, green bonds, gold and CPU were found to be net receivers of volatility.

These results align with Ren et al. (2023a) who found green bonds as safe-haven assets during crisis episodes.13 More specifically, the results from Reboredo et al. (2020) revealed that green bonds were effective device for portfolio hedging and risk diversification over different investment horizons when combined with stocks, high-yield corporate bonds and energy stocks. The finding of CPU as a net receiver of volatility is not surprising as Ren et al. (2023b) argued that CPU functions as a risk recipient, with the causality flowing from market prices to CPU. The ongoing global energy crisis has significantly increased the costs associated with energy-intensive industries, driven by elevated coal and natural gas prices and the frequent volatility of oil prices. These factors have contributed to heightened and persistent uncertainty in CPU levels.

This study also confirms gold’s role as a safe-haven asset during crisis periods, consistent with previous research (Baur and Lucey, 2010; Khan, 2024), which found that gold serves as a hedge and safe-haven in times of crisis. Figure 3 further supports the findings presented in Table 2.

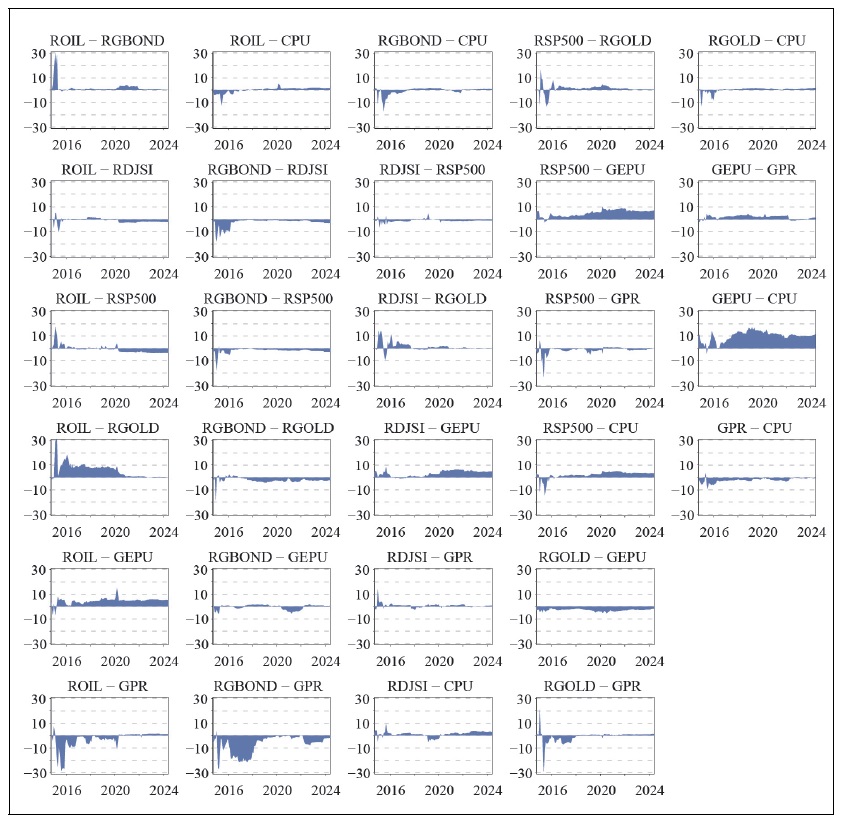

Figure 4 highlights the net pair wise dynamic connectedness plot of the variables. The visual inspection of the plot highlights that GEPU, GPR and S&P 500 are the major transmitters of shocks and volatility to the rest of the markets especially the commodities and sustainable markets. These findings correspond to the results reported in Table 3. In particular, the S&P 500 transmit volatility to the sustainable market including the DJSI and the green bonds markets. This finding supports the results in Table 3 indicating that S&P 500 transmit 22.77% volatility to DJSI and 5.31% to green bonds markets. This may be due to the common risk factors shared by the conventional and sustainable markets and portfolio rebalancing during uncertain periods. GEPU is a major transmitter of volatility to the green bond, gold, and oil markets. As a broader measure of uncertainty compared to CPU, the transmission of shocks from GEPU to CPU is therefore justifiable. These results remain consistent across various alternative methods used as robustness checks to assess GEPU’s impact on financial markets and uncertainty indices. Shocks from the GPR are mainly transmitted to gold, oil and DJSI, whereas the oil market transmitted shocks to the sustainable market. Conversely, gold, green bonds and DJSI are the net receivers of volatility from the other variables including the uncertainty factors and the traditional equity market index. These findings indicate the safe haven nature of gold during the uncertainty periods. Green bonds also received volatility transmission from the CPU corroborating the findings from previous studies indicating the significant role of CPU in the green assets. The most consistent volatility transmitters being the GEPU and GPR. These results further support the results reported in Table 3 where GEPU, GPR and S&P 500 are reported as net transmitters of volatility. The results have important implications for policy makers and investors. Gold and sustainable markets have the characteristics of hedging during the periods of heightened uncertainty due to their ability to absorb shocks from the traditional and uncertainty driven markets. Policy makers should monitor the key transmitters i.e., the GEPU, GPR and traditional markets as they have a significant impact on the global financial markets.

1. Robustness Checks

The study employed several robustness checks to ensure the consistency of the results and the appropriate selection of relevant financial markets and uncertainty factors. The results of the standard VAR model are reported in Table 4, while the orthonormal loadings from PCA are illustrated in Figure 5.

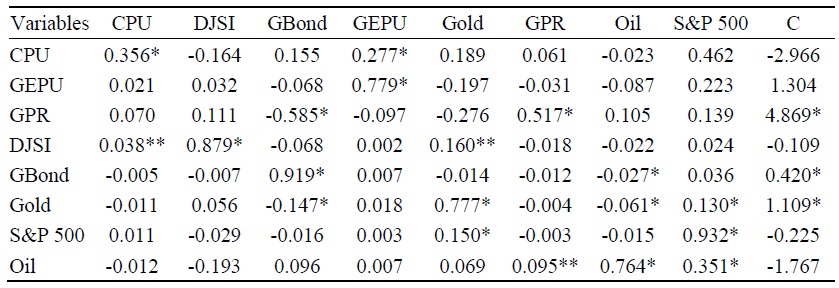

Table 4 presents the results of the standard VAR model, which examines the relationships among the variables under the assumption of constant parameter values. A lag length of one was selected based on the Akaike Information Criterion (AIC) and Schwarz Information Criterion (SIC). The Durbin-Watson statistic yielded values close to two, indicating that the model is free from serial correlation.

Overall, the coefficient estimates suggest strong own-lag effects compared to the shock transmissions from other variables. This implies that each variable’s past values have a significant impact on its current value, highlighting the persistent dynamics of uncertainty indices and financial markets over time.

Table 4 also highlights the cross-spillovers between financial markets and uncertainty indices, as evidenced by the significant off-diagonal coefficients. The significant coefficient for GEPU (0.277) indicates that general economic policy uncertainty contributes to heightened CPU. GEPU also exhibits a high degree of persistence and is not significantly influenced by any other variable, suggesting its independent and dominant nature. Green bonds are negatively affected by commodities (gold and oil) and geopolitical risk, indicating their vulnerability to both commodity market shocks and political instability. Overall, the results demonstrate dynamic interrelationships among political, economic, and climate uncertainties and their spillover effects on financial markets. In addition to their internal persistence, the uncertainty indices exhibit asymmetric cross-asset transmission channels, particularly from climate to sustainable equities, from geopolitical to commodities and from economic to climate uncertainty. However, the standard VAR framework does not account for timevarying behavior in volatility transmission between uncertainty indices and financial markets. Sarma and Rajib (2025) argued that due to the evolving nature of interrelationships under uncertain economic conditions, a dynamic analysis between the most prominent assets is required. This provides strong empirical motivation for adopting TVP-VAR model to better capture the evolving and dynamic nature of the interconnected risks.

Figure 5(a) illustrates the orthonormal loadings of the three uncertainty measures: GEPU, GPR, and CPU, while Figure 5(b) includes Trade Policy Uncertainty (TPU) alongside these three indices. A visual inspection of the figures reveals that GEPU, GPR, and CPU follow distinct trajectories, suggesting that they capture uncertainty transmitted through orthogonal dimensions. The GEPU index reflects broader macroeconomic shocks, whereas TPU is more narrowly focused on trade-related shocks—indicating some degree of overlap between the two. This supports the use of GEPU as a proxy for general economic policy uncertainty and broader economicrelated initiatives. Conversely, TPU may be more suitable in analyses where uncertainty is concentrated in trade-related sectors.

12)The study investigated the volatility spillover in 24 emerging markets using monthly data over a period from January 1997 to May 2018.

13)The study investigated 19 stock markets including 18 from the Group of Twenty (G20) and Switzerland over the period from October 14, 2014 to July 31, 2022.

V. Conclusion

In recent years, rising economic and climate uncertainties, along with growing geopolitical risks, have contributed to significant volatility in global financial markets. This study utilizes the TVP-VAR model to examine the nonlinear, time-varying interconnectedness and spillover effects between September 2014 and June 2024 among commodities (oil and gold), sustainable assets (DJSI and green bonds), and traditional markets (S&P 500), while also considering three key uncertainty indices: CPU, GEPU, and GPR.

The results indicate that GEPU, GPR, and the S&P 500 collectively drive the volatility and interconnectedness of the markets under analysis. The GEPU index stands out as the primary transmitter of volatility, accounting for 83.20% of the total spillover effect. Its influence is particularly significant on gold (26.56%), CPU (17.92%), the S&P 500 (8.96%), and green bonds (8.29%). This prominent role of GEPU aligns with previous studies (e.g., Al-Mamun et al., 2020; Yu et al., 2021), which highlight the substantial impact of economic policy uncertainty on financial market dynamics. Furthermore, GPR has a notable effect on gold, oil, and DJSI, while the S&P 500 and oil markets emerge as major sources of shocks to the sustainable asset markets.

The impact of GPR on commodity markets, especially oil and gold, is understandable due to the direct influence of geopolitical crises on these vital resources. GPR affects oil through both direct and indirect channels (Ayadi and Mbarek, 2025). It can directly disrupt oil supply through conflicts and sanctions and the fear of supply disruption due to political crises. Indirectly, crises can lead to inflationary pressures and higher production costs in oil-importing countries, thereby reducing companies’ profitability (Khan, 2024). Gold, on the other hand, tends to perform well during periods of heightened uncertainty, as investors seek safe-haven assets, increasing demand for gold. Gold offer better diversification opportunity during the crisis episodes and moves against the traditional as well as sustainable markets. These findings are supported by Shaik et al. (2023) who found gold as safe-haven asset during the global financial crisis, COVID-19 and during the Russia-Ukraine war periods. Equity markets are negatively impacted by elevated GPR, as heightened risk aversion among investors often leads to selloffs driven by conflict-related fears. Additionally, during periods of elevated GEPU, the oil market may suffer from demand-side shocks due to trade disruptions and a slowdown in global economic activity. In such times, gold serve as a hedge against policy-related instability. In addition to the more direct transmission channels, heightened uncertainty deteriorates corporate profitability prospects, leading to delayed investments and negatively impacting the equity market. The findings further indicate that risk-averse investors will reduce investments due to heightened uncertainty leading to reduction in the output. The findings corroborate with Bloom (2009) who argued that the real cause of macroeconomic fluctuations is the degree of uncertainty prevailing in the market. These findings support the real options theory, which postulates that investors postpone investment decisions during periods of elevated uncertainty. The findings therefore highlight the necessity of considering GPR and GEPU when managing investment portfolios.

Conversely, gold, CPU, green bonds, and DJSI function predominantly as net receivers of volatility, with gold receiving 57.86% of total spillovers from other markets, making it an effective safe-haven asset during periods of heightened uncertainties. The findings indicate that sustainable assets and commodities, particularly gold, function as effective hedging instruments and safe havens during periods of economic and geopolitical turmoil, offering resilience against heightened uncertainty. Investors should consider reallocating assets toward these safer investment options to minimize the overall portfolio risk by diversifying in to safe assets when confronted with geopolitical risks and economic uncertainty. Furthermore, compared to GEPU and GPR, CPU plays a relatively limited role in volatility transmission.

Despite its valuable contributions, this study is subject to certain limitations. First, the reliance on monthly data may obscure short-term fluctuations that are critical to understanding market dynamics. Second, although the time period used in this study is consistent with several previous studies employing the TVP-VAR model, using a longer time span could yield more robust results. Third, while the TVP-VAR model is robust, incorporating alternative methodologies such as the DCC-GARCH model in future research could enhance the understanding of dynamic connectedness among financial markets. Addressing these limitations would further refine the insights into the volatility spillover mechanisms and improve portfolio risk management strategies.

Tables & Figures

Figure 1.

Time Series Plot of the Variables over the Period from September 2014 to June, 2024

Table 1.

Summary Statistics of the Variables over the Period from September, 2014 to June, 2024

Notes: This table presents the summary statistics for all variables used in the study. CPU, GEPU, GPR, DJSI, Green Bonds, oil, gold, and S&P 500 represent the log-returns of five financial markets (Dow Jones Sustainability Index, Green Bond Index, WTI crude oil futures, gold futures, and the S&P 500), along with the CPU, GEPU, and GPR indices. J-B refers to Jarque-Bera statistics, and ADF indicates the Augmented Dickey-Fuller test for stationarity. Asterisks (*) denote significance at the 1% level.

Table 2.

Correlation Matrix of the Variables

Note: The table reports the correlation among the variables over a period from September 2014 to June 2024. (*) indicates significance at 5% level.

Table 3.

Volatility Spillover among the Markets from September 2014 to June 2024

Notes:

Figure 2.

Total Spillover Index (TCI)

Figure 3.

Net Spillover Index

Figure 4.

Net Pair Wise Dynamic Connectedness Index

Table 4.

Standard VAR Model Results

Notes: Based on the AIC and BIC criteria the lag length of 1 is used. In addition, the Durban Watson statistics was used for model fitness. The variables in the left side were used as dependent variables against the independent variables on the top row. The highlighted values indicate own shock and volatility from the previous month. (*) and (**) indicate significance at 5% and 10% level.

Figure 5.

Orthonormal Loading from Principal Component Analysis

References

-

Adebayo, T. S., Akadiri, S. S. and H. Rjoub. 2022. “On the relationship between Economic Policy Uncertainty, Geopolitical risk and stock market returns in South Korea: A Quantile Causality Analysis.”

Annals of Financial Economics , vol. 17, no. 1.

-

Al-Mamun, Md., Uddin, G. S., Suleman, M. T. and S. H. Kang. 2020. “Geopolitical risk, uncertainty and Bitcoin investment.”

Physica A: Statistical Mechanics and its Applications , vol. 540.

-

Antonakakis, N., Chatziantoniou, I. and D. Gabauer. 2020. “Refined measures of dynamic connectedness based on time-varying parameter vector autoregressions.”

Journal of Risk and Financial Management , vol. 13, no. 4.

-

Asomaning, K. O. and H. Shah. 2023. “Geopolitical risk spillover and Pakistan economic crisis. A TVP-VAR connectedness approach.” Available at SSRN.

https://doi.org/10.2139/ssrn.4610204 -

Asomaning, K. O., Shah, H. and E. Uche. 2024. “A TVP-VAR assessment of the spillover effects of geopolitical risk shocks on macroeconomic variability: A study of the Ghanaian economy.”

Future Business Journal , vol. 10.https://doi.org/10.1186/s43093-024-00341-5 .

-

Ayadi, E. and N. Ben Mbarek. 2025. “The dynamic effects of economic uncertainties and geopolitical risks on Saudi stock market returns: Evidence from local projections.”

Journal of Risk and Financial Management , vol. 18, no. 5.https://doi.org/10.3390/jrfm18050264

-

Baker, S. R., Bloom, N. and S. J. Davis. 2016. “Measuring economic policy uncertainty.”

Quarterly Journal of Economics , vol. 131, no. 4, pp. 1593-1636.https://doi.org/10.1093/qje/qjw024

-

Baur, D. G. and B. M. Lucey. 2010. “Is gold a hedge or a safe haven? An analysis of stocks, bonds and gold.”

Financial Review , vol. 45, no. 2, pp. 217-229.

-

Belke, A., Dubova, I. and T. Osowski. 2018. “Policy uncertainty and international financial markets: The case of Brexit.”

Applied Economics , vol. 50, no. 34-35, pp. 3752-3770.https://doi.org/10.1080/00036846.2018.1436152

-

Bernanke, B. S. 1983. “Irreversibility, uncertainty, and cyclical investment.”

Quarterly Journal of Economics , vol. 98, no. 1, pp. 85-106.

-

Bloom, N. 2009. “The impact of uncertainty shocks.”

Econometrica , vol. 77, no. 3, pp. 623-685.

-

Bossman, A., Gubareva, M. and T. Teplova. 2023. “Economic policy uncertainty, geopolitical risk, market sentiment, and regional stocks: Asymmetric analyses of the EU sectors.”

Eurasian Economic Review , vol. 13, pp. 321-372.https://doi.org/10.1007/s40822-023-00234-y .

-

Bouri, E., Iqbal, N. and T. Klein. 2022. “Climate policy uncertainty and the price dynamics of green and brown energy stocks.”

Finance Research Letters , vol. 47, no. B. - Caldara, D. and M. Iacoviello. 2018. “Measuring geopolitical risk.” International Finance Discussion Paper, no. 1222. Board of Governors of the Federal Reserve System.

-

Caldara, D. and M. Iacoviello. 2022. “Measuring geopolitical risk.”

American Economic Review , vol. 112, no. 4, pp. 1194-1225

-

Cheng, L. T. W., Shen, J. and M. Wojewodzki. 2023. “A cross-country analysis of corporate carbon performance: An international investment perspective.”

Research in International Business and Finance , vol. 64.https://doi.org/10.1016/j.ribaf.2023.101888

-

Cheong, T. S., Wu, Y., Wojewodzki, M. and N. Ma. 2021. “The impacts of globalization on inequality in the post-COVID-19 world: Evidence from China.”

Frontiers in Public Health , vol. 9, pp. 1-11.https://doi.org/10.3389/fpubh.2021.790312

-

Das, D., Kannadhasan, M. and M. Bhattacharyya. 2019. “Do the emerging stock markets react to international economic policy uncertainty, geopolitical risk and financial stress alike?”

North American Journal of Economics and Finance , vol. 48, pp. 1-19.https://doi.org/10.1016/j.najef.2019.01.008

-

Di Tommaso, C., Foglia, M. and V. Pacelli. 2024. “The impact of climate policy uncertainty on the Italian financial market.”

Finance Research Letters , vol. 69, no. A. -

Diebold, F. X. and K. Yilmaz. 2012. “Better to give than to receive: Predictive directional measurement of volatility spillovers.”

International Journal of Forecasting , vol. 28, no. 1, pp. 57-66.https://doi.org/10.1016/j.ijforecast.2011.02.006

-

Diebold, F. X. and K. Yilmaz. 2014. “On the network topology of variance decompositions: Measuring the connectedness of financial firms.”

Journal of Econometrics , vol. 182, no. 1, pp. 119-134.https://doi.org/10.1016/j.jeconom.2014.04.012

-

Elsayed, A. H. and L. Yarovaya. 2019. “Financial stress dynamics in the MENA region: Evidence from the Arab Spring.”

Journal of International Financial Markets Institutions and Money , vol. 62, pp. 20-34.https://doi.org/10.1016/j.intfin.2019.05.004

-

Elsayed, A. H. and M. H. Helmi. 2021. “Volatility transmission and spillover dynamics across financial markets: The role of geopolitical risk.”

Annals of Operations Research , vol. 305, pp. 1-22.https://doi.org/10.1007/s10479-021-04081-5

-

Feng, C., Han, L., Vigne, S. and Y. Xu. 2023. “Geopolitical risk and the dynamics of international capital flows.”

Journal of International Financial Markets Institutions and Money , vol. 82.https://doi.org/10.1016/j.intfin.2022.101693

-

Financial Stability Board (FSB). 2020. “The implications of climate change for financial stability.”

https://www.fsb.org/2020/11/the-implications-of-climate-change-for-financialstability/ (accessed May 21, 2025) -

Gao, L., Guo, K. and X. Wei. 2023. “Dynamic relationship between green bonds and major financial asset markets from the perspective of climate change.”

Frontiers in Environmental Sciences , vol. 10.https://doi.org/10.3389/fenvs.2022.1109796 -

Gavriilidis, K. 2021. “Measuring climate policy uncertainty.” Available at SSRN.

https://doi.org/10.2139/ssrn.3847388 . -

Guidolin, M. and E. La Ferrara. 2010. “The economic effects of violent conflict: evidence from asset market reactions.”

Journal of Peace Research , vol. 47, no. 6, pp. 671-684.https://doi.org/10.1177/0022343310381853

-

Gulen, H. and M. Ion. 2016. “Policy uncertainty and corporate investment.”

Review of Financial Studies , vol. 29, no. 3, pp. 523-564. -

Guo, P., Zhu, H. and W. You. 2018. “Asymmetric dependence between economic policy uncertainty and stock market returns in G7 and BRIC: A quantile regression approach.”

Finance Research Letters , vol. 25, pp. 251-258.

-

He, M. and Y. Zhang. 2022. “Climate policy uncertainty and the stock return predictability of the oil industry.”

Journal of International Financial Markets Institutions and Money , vol. 81. -

Hoque, M. E. and M. A. S. Zaidi. 2020. “Impacts of global-economic-policy uncertainty on emerging stock market: Evidence from linear and non-linear models.”

Prague Economic Papers , vol. 1, pp. 53-66.https://doi.org/10.18267/j.pep.725

-

Hu, Z. and S. Borjigin. 2024. “The amplifying role of geopolitical risks, economic policy uncertainty, and climate risk on energy-stock market volatility spillover across economic cycles.”

North American Journal of Economics and Finance , vol. 71.

-

IMF. 2023. “Ghana: Request for an Arrangement under the Extended Credit Facility.” IMF Country Report, no. 23/168. International Monetary Fund.

https://www.imf.org/-/media/Files/Publications/CR/2023/English/1GHAEA2023001.Ashx -

Ji, Q., Ma, D., Zhai, P., Fan, Y. and D. Zhang. 2024. “Global climate policy uncertainty and financial markets.”

Journal of International Financial Markets, Institutions and Money , vol. 95.

-

Kahneman, D. and A. Tversky. 1979. “Prospect theory: An analysis of decision under risk.”

Econometrica , vol. 47, no. 2, pp. 263-291.

-

Khan, M. N. 2024. “Market volatility and crisis dynamics: A comprehensive analysis of U.S., China, India, and Pakistan stock markets with oil and gold interconnections during COVID-19 and Russia–Ukraine war periods.”

Future Business Journal , vol. 10.https://doi.org/10.1186/s43093-024-00314-8 -

Kollias, C., Kyrtsou, C. and S. Papadamou. 2013. “The effects of terrorism and war on the oil price–stock index relationship.”

Energy Economics , vol. 40, pp. 743-752.

-

Koop, G., Pesaran, M. H. and S. M. Potter. 1996. “Impulse response analysis in nonlinear multivariate models.”

Journal of Econometrics , vol. 74, pp. 119-147.https://doi.org/10.1016/0304-4076(95)01753-4

-

Krueger, P., Sautner, Z. and L. T. Starks. 2020. “The importance of climate risks for institutional investors.”

Review of Financial Studies , vol. 33, no. 3, pp. 1067-1111.https://doi.org/10.1093/rfs/hhz137

-

Lasisi, L., Omoke, P. C. and A. A. Salisu. 2024. “Climate policy uncertainty and stock market volatility.”

Asian Economics Letters , vol. 5, no. 2.https://doi.org/10.46557/001c.37246

-

Liang, C., Umar, M., Ma, F. and T. L. Huynh. 2022. “Climate policy uncertainty and world renewable energy index volatility forecasting.”

Technological Forecasting and Social Change , vol. 182. -

Liu, J., Ma, F., Tang, Y. and Y. Zhang. 2019. “Geopolitical risk and oil volatility: A new insight.”

Energy Economics , vol. 84.

-

Liu, L., Shahrour, M. H., Wojewodzki, M. and A. Rohani. 2025. “Decoding energy market turbulence: A TVP-VAR connectedness analysis of climate policy uncertainty and geopolitical risk shocks.”

Technological Forecasting and Social Change , vol. 210. -

Liu, X., Wojewodzki, M., Cai, Y, and S. Sharma. 2023. “The dynamic relationships between carbon prices and policy uncertainties.”

Technological Forecasting and Social Change , vol. 188.https://doi.org/10.1016/j.techfore.2023.122325

-

Lo, A. W. 2004. “The adaptive markets hypothesis.”

Journal of Portfolio Management , vol. 30, no. 5, pp. 15-29. -

Malkiel, B. G. 2003. “The efficient market hypothesis and its critics.”

Journal of Economic Perspectives , vol. 17, no. 1, pp. 59-82.

-

Mignon, V. and J. Saadaoui. 2024. “How do political tensions and geopolitical risks impact oil prices?”

Energy Economics , vol. 129.https://doi.org/10.1016/j.eneco.2023.107219

-

Nguyen, C. P., Su, D. T., Wongchoti, U. and C. Schinckus. 2020. “The spillover effects of economic policy uncertainty on financial markets: a time-varying analysis.”

Studies in Economics and Finance , vol. 37, no. 3.https://doi.org/10.1108/SEF-07-2019-0262

-

Oliyide, J. A., Adekoya, O. B. and M. A. Khan. 2021. “Economic policy uncertainty and the volatility connectedness between oil shocks and metal market: An extension.”

International Economics , vol. 167, pp. 136-150.https://doi.org/10.1016/j.inteco.2021.06.007

-

Pastor, L. and P. Veronesi. 2012. “Uncertainty about government policy and stock prices.”

Journal of Finance , vol. 67, no. 4, pp. 1129-1264. -

Pastor, L. and P. Veronesi. 2013. “Political uncertainty and risk premia.”

Journal of Financial Economics , vol. 110, no. 3, pp. 520-545.https://doi.org/10.1016/j.jfineco.2013.08.007

-

Pesaran, H. H. and Y. Shin. 1998. “Generalized impulse response analysis in linear multivariate models.”

Economics Letters , vol. 58, no. 1, pp. 17-29.https://doi.org/10.1016/S0165-1765(97)00214-0

-

Reboredo, J. C., Ugolini, A. and F. A. L. Aiubeb. 2020. “Network connectedness of green bonds and asset classes.”

Energy Economics , vol. 86.

-

Ren, B., Lucey, B. and Q. Luo. 2023a. “An Examination of green bonds as a hedge and safe haven for international equity markets.”

Global Finance Journal , vol. 58.

-

Ren, X., Li, J., He, F. and B. Lucey. 2023b. “Impact of climate policy uncertainty on traditional energy and green markets: Evidence from time-varying granger tests.”

Renewable and Sustainable Energy Reviews , vol. 173.

-

Sarma, N. and P. Rajib. 2025. “Do policy uncertainty and volatility index affect dynamic connectedness among house price, financial and commodity market indices? Evidence from TVP-VAR and quantile regression analysis.”

Cogent Economics and Finance , vol. 13, no. 1.https://doi.org/10.1080/23322039.2025.2509613

-

Shahrour, M. H., Arouri, M. and R. Lemand. 2023. “On the foundations of firm climate risk exposure.”

Review of Accounting and Finance , vol. 22, no. 5, pp. 620-635.https://doi.org/10.1108/RAF-05-2023-0163

-

Shahzad, S. J. H., Bouri, E., Roubaud, D. and L. Kristoufek. 2020. “Safe haven, hedge and diversification for G7 stock markets: Gold versus bitcoin.”

Economic Modelling , vol. 87, pp. 212-224.

-

Shaikh, I. 2020. “Does policy uncertainty affect equity, commodity, interest rates, and currency markets? Evidence from CBOE’s volatility index.”

Journal of Business Economics and Management , vol. 21, no. 5, pp. 1350-1374.https://doi.org/10.3846/jbem.2020.13164

-

Shaik, M., Jamil, S. A., Hawaldar, I. T., Sahabuddin, M., Rabbani, M. R. and M. Atif. 2023. “Impact of geo-political risk on stocks, oil, and gold returns during GFC, COVID-19, and Russian–Ukraine war.”

Cogent Economics & Finance , vol. 11, no. 1.https://doi.org/10.1080/23322039.2023.2190213

-

Shang, Y., Han, D., Gozgor, G., Mahalik, M. K. and B. K. Sahoo. 2022. “The impact of climate policy uncertainty on renewable and non-renewable energy demand in the United States.”

Renewable Energy , vol. 197, pp. 654-667.

-

Siddique, M. A., Nobanee, H., Hasan, M. B., Uddin, G. S., Hossain, M. N. and D. Park. 2023. “How do energy markets react to climate policy uncertainty? Fossil versus renewable and low-carbon energy assets.”

Energy Economics , vol. 128.https://doi.org/10.1016/j.eneco.2023.107195

-

Sohag, K., Islam, M. M., Tomas Žiković, I. and H. Mansour. 2023. “Food inflation and geopolitical risks: analyzing European regions amid the Russia-Ukraine war.”

British Food Journal , vol. 125, no. 7, pp. 2368-2391.https://doi.org/10.1108/BFJ-09-2022-0793

-

Tian, H., Long, S. and Z. Li. 2022. “Asymmetric effects of climate policy uncertainty, infectious diseases-related uncertainty, crude oil volatility, and geopolitical risks on green bond prices.”

Finance Research Letters , vol. 48.https://doi.org/10.1016/j.frl.2022.103008

-

Uche, E., Nwaeze, N. C. and R. T. Obiakor. 2022. “Do geopolitical risk factors and economic policy uncertainties stimulate capital outflows: An updated evidence.”

Studies of Applied Economics , vol. 40, no. 3.https://doi.org/10.25115/eea.v40i3.6971 -

Wang, Y., Bouri, E., Fareed, Z. and Y. Dai. 2022. “Geopolitical risk and the systemic risk in the commodity markets under the war in Ukraine.”

Finance Research Letters , vol. 49.https://doi.org/10.1016/j.frl.2022.103066 -

Yu, X., Huang, Y. and K. Xiao. 2021. “Global economic policy uncertainty and stock volatility: evidence from emerging economies.”

Journal of Applied Economics , vol. 24, no. 1, pp. 416-440.https://doi.org/10.1080/15140326.2021.1953913